What is section 80c of income tax act is one of the most important questions every salaried person and taxpayer in India should understand because it directly impacts how much tax you pay and how much money you can legally save every year. If you have ever felt that your salary disappears quickly due to taxes, then you are not alone. Most people earn well but fail to optimize their taxes simply because they don’t understand how to use deductions like section 80C effectively. The good news is that once you understand this concept clearly, you can save a significant amount of money without doing anything complicated. This guide will explain everything in a simple, practical, and real-life way so that you can actually use it and not just read it.

What is section 80c of income tax act and why it matters

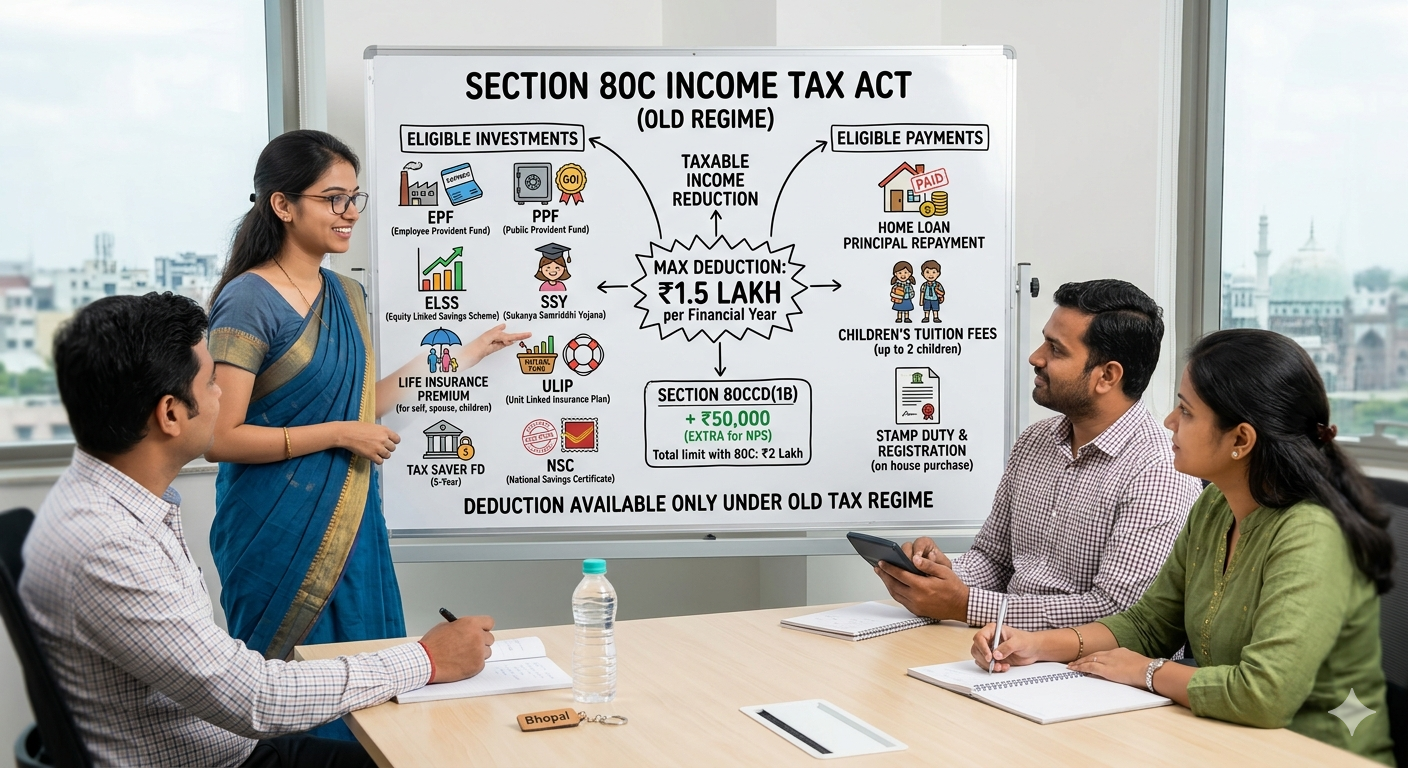

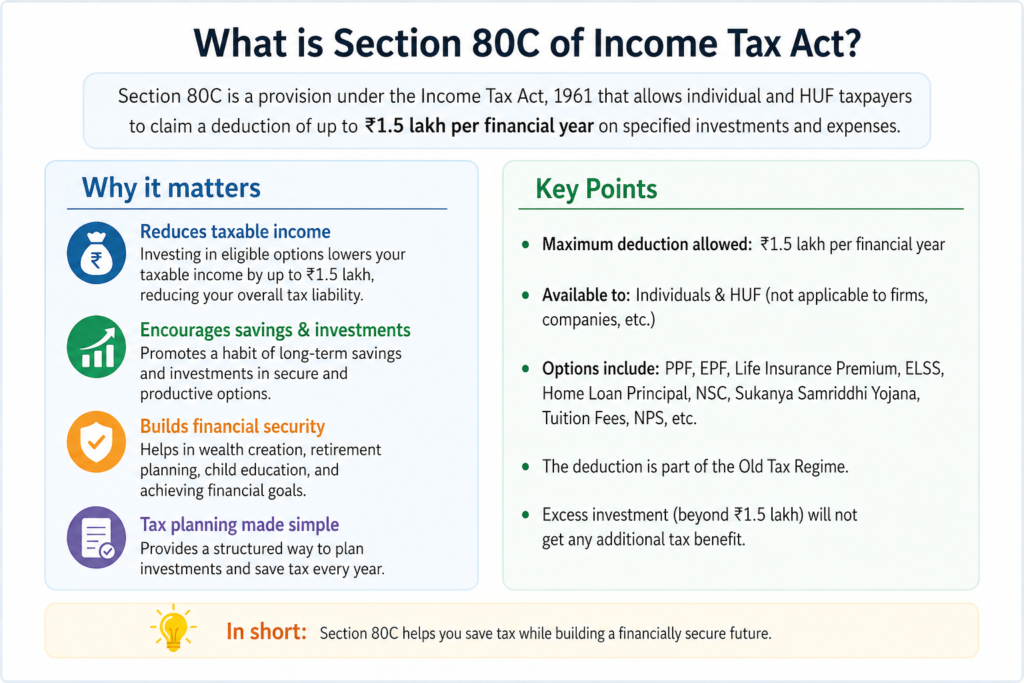

Section 80C of the Income Tax Act allows individuals to reduce their taxable income by investing or spending money in specific financial instruments and expenses approved by the government. In simple terms, it is a legal way to reduce your tax burden. The maximum deduction allowed under this section is ₹1.5 lakh per financial year. This means if you invest or spend ₹1.5 lakh in eligible options, your taxable income reduces by the same amount. Therefore, the tax you pay becomes lower. This is why understanding what is section 80c of income tax act is not just theory but a practical tool for saving money.

How section 80C actually works in real life

Let’s understand this with a simple example. Suppose your annual income is ₹8 lakh. If you invest ₹1.5 lakh under section 80C, your taxable income becomes ₹6.5 lakh. Now you will pay tax on ₹6.5 lakh instead of ₹8 lakh. This difference directly reduces your tax liability. However, many people make the mistake of investing randomly at the last minute just to save tax. Instead, a smarter approach is to plan your investments at the beginning of the financial year so your money works for you throughout the year.

Eligible investments under section 80C

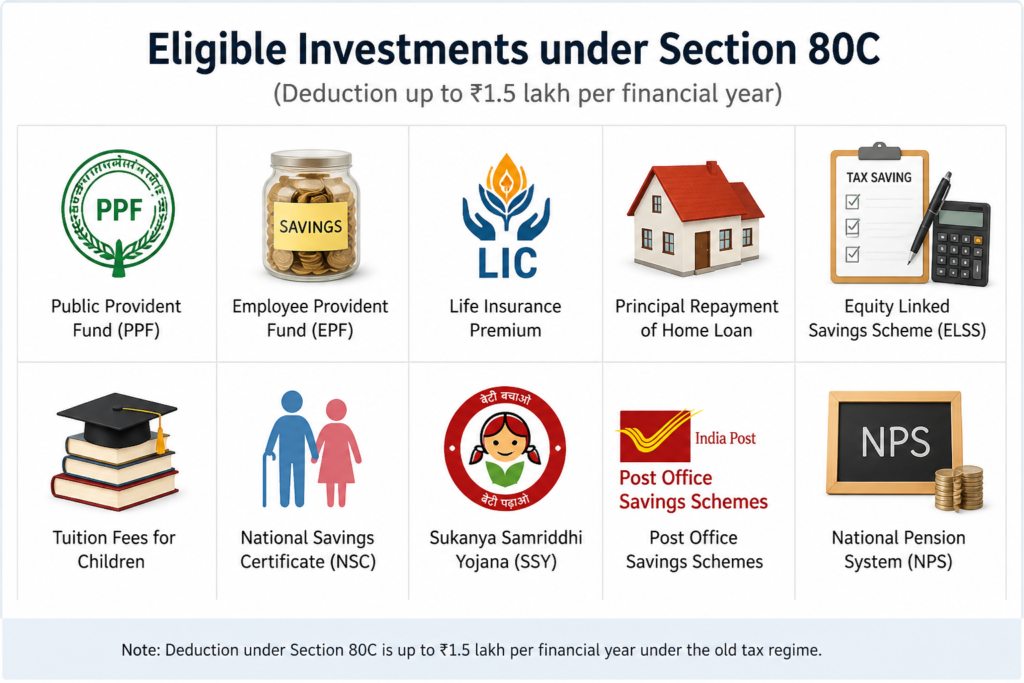

There are multiple options available under section 80C, and each serves a different purpose. Some of the most popular ones include Public Provident Fund, Employee Provident Fund, Equity Linked Savings Scheme, National Savings Certificate, life insurance premium, tax-saving fixed deposits, Sukanya Samriddhi Yojana, and tuition fees for children. Each option has its own risk level, return potential, and lock-in period. Therefore, understanding what is section 80c of income tax act also means understanding where to invest based on your goals.

Public Provident Fund as a safe option

Public Provident Fund is one of the safest investment options backed by the government. It offers guaranteed returns and has a long-term lock-in period of 15 years. This makes it ideal for people who want stability and long-term wealth creation. However, liquidity is low because you cannot withdraw money easily.

Equity Linked Savings Scheme for higher returns

If you want higher returns, Equity Linked Savings Scheme is a better option. It invests in the stock market and has a lock-in period of just 3 years, which is the lowest among all section 80C investments. Over the long term, ELSS has the potential to generate higher returns compared to traditional options.

Life insurance and tax saving

Life insurance premiums also qualify under section 80C. While insurance should not be treated purely as an investment, it plays an important role in financial security. A good term insurance plan protects your family while also helping you save tax.

Common mistakes people make with section 80C

One of the biggest mistakes people make is waiting until March to invest. This leads to poor decisions and low returns. Another mistake is choosing low-return products just because they are safe. While safety is important, you should also consider inflation and long-term growth. Many people also ignore diversification and put all their money into one instrument, which is not ideal.

Smart strategy to use section 80C effectively

A balanced approach works best. You can divide your ₹1.5 lakh limit into different categories such as safe investments, growth investments, and protection. For example, you can allocate some amount to PPF for safety, some to ELSS for growth, and some to insurance for protection. This way, you not only save tax but also build a strong financial foundation.

Real life example of smart tax planning

Imagine two individuals earning the same salary. One invests randomly at the end of the year, while the other plans systematically from April. The second person not only saves tax but also earns better returns because the money stays invested longer. Over 10 to 15 years, this difference becomes huge. This is why understanding what is section 80c of income tax act is important for long-term wealth creation.

Advanced tips most people don’t know

One powerful strategy is to combine section 80C with other deductions like 80D for health insurance and 80CCD for NPS. This can significantly reduce your taxable income. Another smart move is to increase your investments gradually every year instead of keeping them fixed. This helps you build wealth faster without feeling financial pressure.

Frequently Asked Questions

What is section 80c of income tax act in simple words

It is a provision that allows you to reduce taxable income by investing in specific options up to ₹1.5 lakh.

What is the maximum limit under section 80C

The maximum deduction allowed is ₹1.5 lakh per financial year.

Which investment is best under section 80C

It depends on your goal. ELSS is good for growth, while PPF is good for safety.

Can I claim both PPF and ELSS

Yes, you can invest in multiple options as long as the total does not exceed ₹1.5 lakh.

Is section 80C available for everyone

Yes, it is available for individuals and Hindu Undivided Families under the old tax regime.

How to choose the right section 80C investments for your goals

Understanding what is section 80c of income tax act is only the first step. The real benefit comes when you choose the right combination of investments based on your financial goals. Every person has different priorities. Some want safety, some want growth, and some want liquidity. Therefore, instead of copying others, you should align your choices with your own life situation. For example, if you are in your early career stage, you can take slightly higher risk and invest more in equity-based options like ELSS. On the other hand, if you are closer to retirement, stability becomes more important, so safer options like PPF or fixed deposits may be better. This is why personalizing your 80C strategy matters more than just using it.

Understanding risk vs return in section 80C

Many people focus only on saving tax and ignore returns. This is a mistake. Inflation reduces the value of money over time, so your investments should ideally grow faster than inflation. Equity-based options like ELSS have higher risk in the short term, but over the long term, they usually deliver better returns. On the other hand, options like PPF and NSC offer stable but lower returns. Therefore, a mix of both can create balance. Understanding what is section 80c of income tax act also means understanding that tax saving and wealth creation should go together.

Importance of starting early in the financial year

One simple habit can make a huge difference in your financial life. Instead of investing at the last minute, start your 80C investments from April itself. When you invest early, your money stays invested for a longer time and earns better returns. This is especially important for market-linked investments. Even if the amount is small, consistency matters more than timing. Over the years, this habit builds discipline and significantly improves your financial position.

Role of discipline in tax saving

Tax saving is not just a financial activity. It is also a behavioral habit. Many people know what is section 80c of income tax act but still fail to use it effectively because they lack consistency. They delay decisions, spend unnecessarily, and then rush at the end of the year. To avoid this, you need a system. For example, setting up a monthly SIP in ELSS or a regular contribution to PPF can automate your tax saving. This reduces stress and ensures that you stay on track without extra effort.

Combining section 80C with overall financial planning

Section 80C should not be treated as a separate task. It should be part of your overall financial plan. Your investments should match your life goals such as buying a house, funding education, or building retirement wealth. When you connect tax saving with goals, it becomes more meaningful. Instead of just saving tax, you start building a future. This mindset shift is what separates smart investors from average ones.

How salaried individuals can maximize benefits

If you are a salaried employee, you have a great advantage. Your employer often provides options like EPF and sometimes NPS contributions. EPF automatically contributes to your 80C limit, which reduces your effort. However, many people don’t even check how much is already being invested through EPF. Once you know this, you can plan the remaining amount accordingly. This helps you use the full ₹1.5 lakh limit efficiently without overinvesting or underutilizing the benefit.

How self-employed individuals can use section 80C

For self-employed individuals, there is no automatic deduction like EPF. This means you need to plan everything yourself. The advantage is flexibility. You can choose where to invest and how much to invest based on your income flow. However, this also requires discipline. Setting aside a fixed percentage of income every month can help you stay consistent. Understanding what is section 80c of income tax act becomes even more important in this case because it directly affects your tax liability.

Tax planning vs tax saving

Many people confuse tax planning with tax saving. Tax saving is just one part of the process. Tax planning is a broader concept where you organize your income, expenses, and investments in a way that minimizes tax legally while maximizing returns. Section 80C is a major tool in this process, but it should be used strategically. For example, blindly investing in low-return products just to save tax may not be the best decision in the long run.

Case study: smart vs average investor

Let’s look at a simple scenario. Two people earn ₹10 lakh annually. Both use section 80C, but their approach is different. The first person invests ₹1.5 lakh in low-return instruments every year without thinking about growth. The second person splits the same amount into PPF and ELSS and invests consistently from the start of the year. After 15 years, the second person has significantly higher wealth due to better returns and compounding. This shows that how you use section 80C matters more than just using it.

Pro tips for maximizing section 80C benefits

One effective strategy is to increase your investment every year as your income grows. This helps you maintain the same savings ratio. Another tip is to review your investments annually. Financial situations change, and your strategy should adapt accordingly. Also, avoid locking all your money in long-term instruments if you may need liquidity. Balance is the key. Understanding what is section 80c of income tax act gives you the foundation, but smart execution gives you results.

Emotional aspect of money management

Money is not just numbers. It is connected to emotions, habits, and mindset. Many people overspend due to social pressure or lifestyle inflation. This reduces their ability to invest and save tax. By creating a structured plan using section 80C, you bring control and clarity into your financial life. This reduces stress and increases confidence. Over time, this leads to better decisions and a more secure future.

Future of tax saving in India

The tax system in India is evolving. The new tax regime offers lower rates but removes many deductions including section 80C. Therefore, taxpayers need to evaluate which regime suits them better. If you actively invest and use deductions, the old regime with section 80C may be beneficial. However, if you prefer simplicity, the new regime may be suitable. Understanding what is section 80c of income tax act helps you make this decision more effectively.

How to choose the right section 80C investments for your goals

Understanding what is section 80c of income tax act is only the first step. The real benefit comes when you choose the right combination of investments based on your financial goals. Every person has different priorities. Some want safety, some want growth, and some want liquidity. Therefore, instead of copying others, you should align your choices with your own life situation. For example, if you are in your early career stage, you can take slightly higher risk and invest more in equity-based options like ELSS. On the other hand, if you are closer to retirement, stability becomes more important, so safer options like PPF or fixed deposits may be better. This is why personalizing your 80C strategy matters more than just using it.

Understanding risk vs return in section 80C

Many people focus only on saving tax and ignore returns. This is a mistake. Inflation reduces the value of money over time, so your investments should ideally grow faster than inflation. Equity-based options like ELSS have higher risk in the short term, but over the long term, they usually deliver better returns. On the other hand, options like PPF and NSC offer stable but lower returns. Therefore, a mix of both can create balance. Understanding what is section 80c of income tax act also means understanding that tax saving and wealth creation should go together.

Importance of starting early in the financial year

One simple habit can make a huge difference in your financial life. Instead of investing at the last minute, start your 80C investments from April itself. When you invest early, your money stays invested for a longer time and earns better returns. This is especially important for market-linked investments. Even if the amount is small, consistency matters more than timing. Over the years, this habit builds discipline and significantly improves your financial position.

Role of discipline in tax saving

Tax saving is not just a financial activity. It is also a behavioral habit. Many people know what is section 80c of income tax act but still fail to use it effectively because they lack consistency. They delay decisions, spend unnecessarily, and then rush at the end of the year. To avoid this, you need a system. For example, setting up a monthly SIP in ELSS or a regular contribution to PPF can automate your tax saving. This reduces stress and ensures that you stay on track without extra effort.

Combining section 80C with overall financial planning

Section 80C should not be treated as a separate task. It should be part of your overall financial plan. Your investments should match your life goals such as buying a house, funding education, or building retirement wealth. When you connect tax saving with goals, it becomes more meaningful. Instead of just saving tax, you start building a future. This mindset shift is what separates smart investors from average ones.

How salaried individuals can maximize benefits

If you are a salaried employee, you have a great advantage. Your employer often provides options like EPF and sometimes NPS contributions. EPF automatically contributes to your 80C limit, which reduces your effort. However, many people don’t even check how much is already being invested through EPF. Once you know this, you can plan the remaining amount accordingly. This helps you use the full ₹1.5 lakh limit efficiently without overinvesting or underutilizing the benefit.

How self-employed individuals can use section 80C

For self-employed individuals, there is no automatic deduction like EPF. This means you need to plan everything yourself. The advantage is flexibility. You can choose where to invest and how much to invest based on your income flow. However, this also requires discipline. Setting aside a fixed percentage of income every month can help you stay consistent. Understanding what is section 80c of income tax act becomes even more important in this case because it directly affects your tax liability.

Tax planning vs tax saving

Many people confuse tax planning with tax saving. Tax saving is just one part of the process. Tax planning is a broader concept where you organize your income, expenses, and investments in a way that minimizes tax legally while maximizing returns. Section 80C is a major tool in this process, but it should be used strategically. For example, blindly investing in low-return products just to save tax may not be the best decision in the long run.

Case study: smart vs average investor

Let’s look at a simple scenario. Two people earn ₹10 lakh annually. Both use section 80C, but their approach is different. The first person invests ₹1.5 lakh in low-return instruments every year without thinking about growth. The second person splits the same amount into PPF and ELSS and invests consistently from the start of the year. After 15 years, the second person has significantly higher wealth due to better returns and compounding. This shows that how you use section 80C matters more than just using it.

Pro tips for maximizing section 80C benefits

One effective strategy is to increase your investment every year as your income grows. This helps you maintain the same savings ratio. Another tip is to review your investments annually. Financial situations change, and your strategy should adapt accordingly. Also, avoid locking all your money in long-term instruments if you may need liquidity. Balance is the key. Understanding what is section 80c of income tax act gives you the foundation, but smart execution gives you results.

Emotional aspect of money management

Money is not just numbers. It is connected to emotions, habits, and mindset. Many people overspend due to social pressure or lifestyle inflation. This reduces their ability to invest and save tax. By creating a structured plan using section 80C, you bring control and clarity into your financial life. This reduces stress and increases confidence. Over time, this leads to better decisions and a more secure future.

Conclusion

Future of tax saving in India

The tax system in India is evolving. The new tax regime offers lower rates but removes many deductions including section 80C. Therefore, taxpayers need to evaluate which regime suits them better. If you actively invest and use deductions, the old regime with section 80C may be beneficial. However, if you prefer simplicity, the new regime may be suitable. Understanding what is section 80c of income tax act helps you make this decision more effectively.