Escape Debt Trap: 7 Proven ₹15000 Hacks sounds impossible to many people. Every month salary comes, bills get paid, EMI cuts happen, and within a few days the bank balance becomes zero again. Then people start using credit cards, borrowing from friends, or taking personal loans just to survive till the next salary. Slowly this becomes a dangerous cycle where stress increases every single month. The worst part is that many hardworking people believe they can never escape this situation because their income is too low.

But the truth is different. Even with a ₹15000 monthly income, you can slowly escape debt if you follow the right strategy. Thousands of Indians have already done it by changing a few financial habits, controlling emotional spending, and creating smart money systems. You do not need to become rich overnight. You only need discipline, patience, and a practical roadmap that works in real life.

Most people fail because they try random financial advice from social media. However, low income financial planning works differently. You need a survival-first strategy. This guide will help you understand exactly how to manage rent, food, EMI, savings, and future planning even on a limited income. If you follow these methods consistently, your financial stress can reduce dramatically within a few months.

Table of Contents

Escape Debt Trap: 7 Proven ₹15000 Hacks-Why People Fall Into A Dangerous Debt Trap

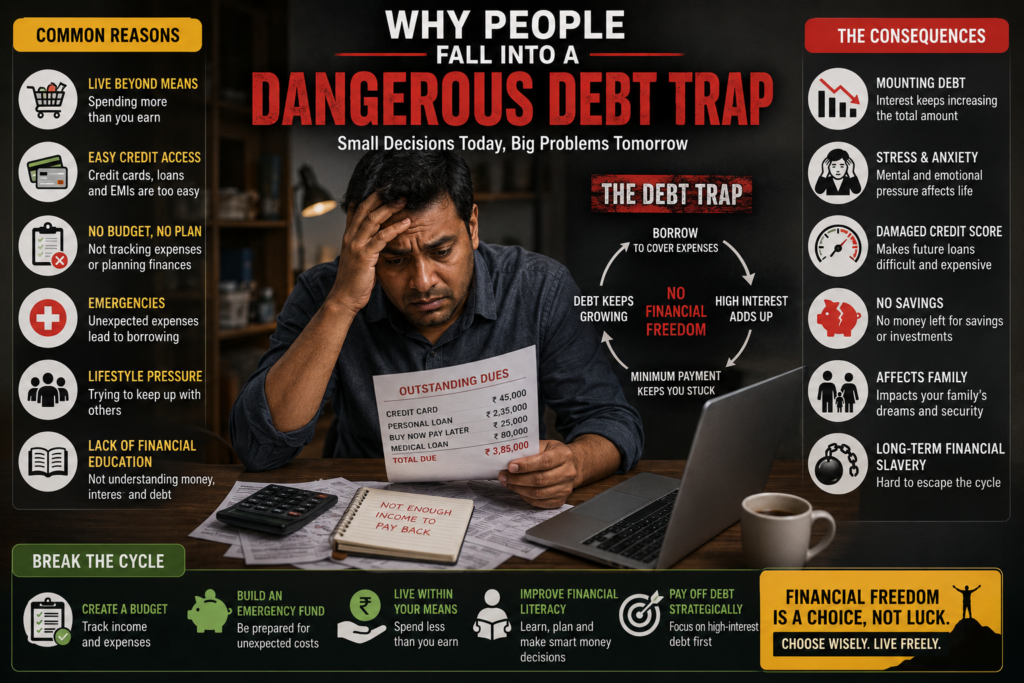

A dangerous debt trap usually starts with small mistakes. Many people think debt happens only because of low income. However, the real reason is poor money management combined with financial emergencies. For example, a person earning ₹15000 may suddenly face hospital expenses, job loss, or family pressure. Since there are no savings, borrowing becomes the only option.

Another major reason is lifestyle inflation. The moment salary comes, people spend on online shopping, expensive mobile phones, food delivery apps, or unnecessary subscriptions. Small expenses may look harmless individually, but together they destroy monthly budgets. Therefore, even basic needs become difficult later.

Credit cards make the situation even worse. Initially, they feel convenient. However, once minimum payments begin, interest grows rapidly. Soon the person starts borrowing money just to pay old debt. This creates a dangerous cycle that becomes emotionally exhausting.

In addition, social pressure plays a big role in India. Many people spend money on weddings, festivals, gifts, and status symbols just to impress relatives or friends. Unfortunately, these temporary impressions create long-term financial pain.

Escape Debt Trap: 7 Proven ₹15000 Hacks The biggest problem is that people ignore debt during the early stage. They think things will improve automatically next month. But without action, debt keeps growing silently. Interest accumulates, stress increases, and confidence decreases.

Therefore, the first step to Escape Dangerous Debt Trap With ₹15000 Monthly Income is accepting the reality honestly. You cannot solve financial problems emotionally. You must face them strategically. Once you understand where your money is going, half the battle is already won.

Escape Dangerous Debt Trap With ₹15000 Monthly Income Using Smart Budgeting

Smart budgeting is the foundation of financial recovery. Without a proper budget, even ₹1 lakh salary can disappear quickly. However, with discipline, even ₹15000 income can become manageable.

The first thing you should do is divide your salary into clear categories. A simple budgeting method works best for low-income earners.

Needs: 60%

Debt Repayment: 20%

Savings: 10%

Emergency Expenses: 10%

For example, if your monthly income is ₹15000, your budget may look like this:

House Rent And Utilities: ₹5000

Food And Groceries: ₹3000

Travel Expenses: ₹1000

Debt EMI: ₹3000

Savings: ₹1500

Emergency Fund: ₹1500

Escape Debt Trap: 7 Proven ₹15000 Hacks-Initially, this may feel difficult. However, budgeting becomes easier after two months because you start understanding spending patterns.

Escape Debt Trap: 7 Proven ₹15000 Hacks-One important trick is using cash instead of digital payments for daily expenses. People usually spend more carelessly through UPI and cards because money does not physically leave their hands. Cash creates spending awareness naturally.

Another useful strategy is tracking every rupee for 30 days. Write down every expense in a notebook or mobile app. Even tea, snacks, or auto fare should be recorded. This habit reveals hidden money leaks immediately.

In addition, stop comparing your lifestyle with others. Social media creates unrealistic financial pressure. Many people showing luxury online are actually struggling with debt offline. Focus only on your own progress.

Most importantly, avoid taking new loans while repaying old debt. Otherwise, you will never break the cycle. Financial freedom starts when borrowing stops completely.

Escape Debt Trap: 7 Proven ₹15000 Hacks-Best Money Saving Habits For Low Income Families

Saving money on a low salary requires creativity more than sacrifice. Many families think saving is impossible after expenses. However, small habits can create surprisingly big results over time.

Start with food expenses because they consume a large portion of income. Cooking at home instead of ordering food can save thousands every month. Simple homemade meals are healthier and cheaper.

Electricity savings also matter. Switch off unnecessary lights, fans, and appliances. Small reductions in electricity bills create long-term financial benefits.

Transportation costs can also be reduced. If possible, use public transport instead of private vehicles. Fuel expenses destroy low-income budgets very quickly.

In addition, avoid emotional shopping. Many people buy things because of stress, sadness, or boredom. Before purchasing anything, ask yourself one question: “Do I truly need this right now?” This simple habit prevents unnecessary expenses.

Subscription services should also be reviewed carefully. Multiple OTT apps, gaming subscriptions, or premium memberships silently drain money every month. Cancel everything non-essential immediately.

Another powerful habit is using the “24-hour rule.” Whenever you want to buy something unnecessary, wait for 24 hours before purchasing. Most impulsive desires disappear automatically after some time.

Families can also save money through bulk grocery shopping. Buying monthly essentials together usually reduces overall cost significantly.

Escape Debt Trap: 7 Proven ₹15000 Hacks-Most importantly, create a separate savings account that is difficult to access quickly. This prevents unnecessary withdrawals and builds financial discipline gradually.

Escape Debt Trap: 7 Proven ₹15000 Hacks-How To Repay Debt Faster On ₹15000 Salary

Repaying debt on a low salary feels stressful, but it becomes manageable when approached strategically. The biggest mistake people make is paying random amounts without a clear repayment plan.

First, list all your debts clearly. Write loan amount, interest rate, minimum EMI, and remaining balance. This creates clarity.

Then choose one of these methods:

Escape Debt Trap: 7 Proven ₹15000 Hacks-Snowball Method:

Pay off the smallest loan first while continuing minimum payments on others. This creates psychological motivation because small wins build confidence.

Avalanche Method:

Focus on the highest-interest loan first. This saves more money long-term because expensive debt reduces faster.

For low-income earners, the snowball method often works better emotionally because motivation is extremely important during financial struggles.

Another useful strategy is negotiating with lenders. Many people feel scared to talk to banks or lenders. However, banks sometimes offer lower EMI options, settlement plans, or temporary relief if you communicate honestly.

Side income should also be used primarily for debt repayment instead of lifestyle upgrades. Many people waste extra income on entertainment instead of financial recovery.

In addition, stop lending money to others during your debt repayment journey. Helping everyone while drowning financially yourself creates more problems.

Most importantly, never miss EMI dates intentionally. Late payment charges and penalties increase debt faster than expected. Set automatic reminders to avoid this situation.

The journey may feel slow initially. However, consistency creates momentum. Even paying ₹500 extra every month can reduce long-term interest dramatically.

Escape Dangerous Debt Trap With ₹15000 Monthly Income Through Side Income Ideas

Increasing income is equally important for financial recovery. Although budgeting helps, side income accelerates debt freedom significantly.

Today, there are many realistic side income opportunities available in India. You do not need huge investments to start.

Freelancing is one of the best options. Skills like content writing, graphic design, video editing, data entry, or social media management can generate additional monthly income.

Tuition classes are also powerful. If you are good at any subject, teaching school students can provide stable extra earnings.

Delivery jobs during weekends can also help temporarily. Many people use part-time delivery work to clear debt faster.

Selling unused items online is another smart strategy. Old mobile phones, clothes, furniture, or electronics can generate emergency cash immediately.

Women can explore home-based businesses like tiffin services, tailoring, handmade products, or beauty services. Small businesses often grow surprisingly fast with consistency.

Affiliate marketing and blogging are long-term opportunities as well. Although results take time, they can eventually create passive income streams.

However, avoid fake online earning schemes promising instant riches. Many desperate people lose money because of scams during financial stress.

The goal is not becoming rich quickly. The goal is creating breathing space financially. Even an extra ₹3000 monthly income can completely transform your financial situation over time.

Escape Debt Trap: 7 Proven ₹15000 Hacks-Real Life Example Of Escaping Debt On Low Salary

Ramesh from Indore earned only ₹16000 monthly working in a private company. Due to family medical emergencies and credit card bills, his total debt reached ₹1.8 lakh. Every month, most of his salary went toward EMI payments.

Initially, he felt hopeless. However, he decided to change his financial habits completely.

He shifted to shared accommodation and reduced rent costs. He stopped online shopping entirely. Food delivery apps were deleted from his phone. He started tracking every expense daily.

At the same time, he began giving evening tuition to school students. This generated an additional ₹4000 monthly income.

Instead of increasing lifestyle expenses, he used the extra income only for debt repayment. Within two years, he cleared almost all debt completely.

Today, he maintains an emergency fund and avoids unnecessary borrowing completely.

His story proves one important truth. Financial recovery depends more on discipline than salary size.

Escape Debt Trap: 7 Proven ₹15000 Hacks-Common Mistakes That Keep People Trapped In Debt

Many people work hard but still remain financially stuck because they repeat the same mistakes continuously.

The first mistake is ignoring small expenses. Daily snacks, online offers, and impulsive purchases slowly damage budgets badly.

The second mistake is depending too much on credit cards. Easy money creates dangerous habits.

Another major mistake is borrowing for non-essential lifestyle upgrades. Expensive phones, bikes, or celebrations should never be financed through debt on low income.

People also fail because they avoid financial planning completely. Hope is not a financial strategy. Without budgeting, debt automatically grows.

In addition, many people try to escape stress through entertainment spending. Shopping or eating outside may provide temporary happiness, but financial anxiety returns stronger later.

The final mistake is giving up too early. Debt freedom takes time. Progress may feel slow initially, but consistency changes everything eventually.

Escape Dangerous Debt Trap With ₹15000 Monthly Income By Building Emergency Fund

An emergency fund acts like financial protection. Without it, every unexpected expense pushes people back into debt again.

Start very small. Even saving ₹20 daily matters initially. Over time, small savings create meaningful financial security.

Keep emergency savings separate from daily spending accounts. This prevents unnecessary usage.

Your first goal should be saving at least one month of expenses. After that, aim for three months gradually.

Emergency funds should only be used for genuine crises like medical emergencies, job loss, or urgent repairs. They are not for shopping or vacations.

Many people underestimate the emotional power of savings. Even small emergency funds reduce stress and improve decision-making confidence significantly.

Escape Debt Trap: 7 Proven ₹15000 Hacks-How To Stay Motivated During Financial Struggles

Financial recovery is not only about money. It is also a mental challenge.

There will be months when progress feels invisible. Sometimes unexpected expenses may slow down your journey. However, do not quit.

Celebrate small wins. Paying off one EMI, reducing one loan, or saving your first ₹5000 matters more than people realize.

Avoid negative comparisons. Everyone has different financial circumstances.

Surround yourself with practical financial content instead of luxury lifestyle content online. Your environment influences financial habits strongly.

Most importantly, remember that temporary struggle does not define your future permanently. Many financially successful people once faced severe debt problems too.

Escape Debt Trap: 7 Proven ₹15000 Hacks-Practical Monthly Budget Plan To Escape Debt Faster

Most people who try to Escape Dangerous Debt Trap With ₹15000 Monthly Income fail because they create unrealistic budgets. They try to stop all spending suddenly, and within a few weeks they return to old habits again. Therefore, your budget should feel practical and sustainable instead of painful.

Escape Debt Trap: 7 Proven ₹15000 Hacks-A realistic low-income monthly budget should focus on survival first, comfort second, and luxury last. This mindset shift changes everything financially. Many people unknowingly treat wants like needs. However, once you learn the difference, financial pressure starts reducing immediately.

For example, basic groceries are needs, but expensive restaurant dinners are wants. A simple smartphone is a need, but upgrading to a premium device on EMI becomes a financial burden. Therefore, before spending money, classify every expense honestly.

Escape Debt Trap: 7 Proven ₹15000 Hacks-A strong monthly budget on ₹15000 income may look like this:

Rent Or Shared Accommodation: ₹4500

Food And Groceries: ₹3000

Electricity And Mobile Recharge: ₹1000

Travel Expenses: ₹1200

Debt EMI Repayment: ₹3000

Emergency Savings: ₹1000

Miscellaneous Expenses: ₹1300

Initially, following this budget may feel restrictive. However, after two or three months, your mind adjusts automatically. In fact, many people later realize they were wasting money on things that never truly improved their lives.

Escape Debt Trap: 7 Proven ₹15000 Hacks-Another powerful strategy is “budgeting before salary arrives.” Do not wait until money enters your account. Plan every rupee in advance. When salary comes, immediately divide the amount according to categories. This prevents emotional spending.

In addition, keep separate UPI accounts if possible. One account for expenses and another for savings. This small trick improves money discipline dramatically.

Most importantly, remember that budgeting is not punishment. Budgeting is financial control. The moment you control your money, your stress starts reducing automatically.

Escape Debt Trap: 7 Proven ₹15000 Hacks-Escape Dangerous Debt Trap With ₹15000 Monthly Income Using Minimalist Lifestyle

Minimalism does not mean living a boring life. It simply means removing unnecessary financial pressure from your lifestyle. Many people remain trapped in debt because they constantly chase social validation through spending.

In India, social pressure influences money decisions heavily. People spend beyond their capacity on weddings, festivals, clothes, gadgets, and celebrations just to avoid judgment from others. Unfortunately, these temporary moments create long-term financial problems.

Escape Debt Trap: 7 Proven ₹15000 Hacks-A minimalist lifestyle helps you focus only on things that genuinely improve your life. Instead of buying many cheap products repeatedly, you start choosing fewer meaningful purchases. Therefore, overall spending reduces naturally.

For example, many people purchase clothes during every online sale because discounts create excitement. However, most items remain unused later. If you avoid impulsive shopping for just six months, you can save thousands of rupees without reducing happiness.

Minimalism also improves mental peace. When financial pressure decreases, relationships improve, sleep becomes better, and future planning feels easier.

Escape Debt Trap: 7 Proven ₹15000 Hacks-Another hidden advantage is reduced maintenance costs. Fewer gadgets, subscriptions, and unnecessary items mean fewer repair expenses and fewer replacement costs.

In addition, minimalism teaches gratitude. Instead of feeling poor constantly, you begin appreciating stability and security. This emotional shift reduces stress-related spending habits significantly.

People often think happiness comes from spending more. However, true financial freedom comes from needing less.

Escape Debt Trap: 7 Proven ₹15000 Hacks-How Low Salary Earners Can Build Financial Discipline

Financial discipline matters more than financial intelligence. Many educated people remain trapped in debt because they cannot control spending habits. Meanwhile, some low-income workers slowly build wealth through consistent discipline.

The easiest way to build discipline is automation. Human emotions are unreliable. Therefore, systems work better than motivation.

For example, automatically transfer a fixed amount into savings immediately after salary arrives. Even ₹500 matters initially. Over time, this creates a strong financial habit.

Escape Debt Trap: 7 Proven ₹15000 Hacks-Another useful habit is delaying gratification. Whenever you want to buy something expensive, wait seven days before making the purchase. Most desires disappear naturally during this period.

Tracking progress visually also improves discipline. Create a debt repayment chart and mark completed payments every month. This creates motivation because visible progress feels rewarding psychologically.

In addition, avoid spending time with people who constantly pressure you into unnecessary expenses. Your financial environment influences your habits more than you realize.

Escape Debt Trap: 7 Proven ₹15000 Hacks-One powerful rule followed by financially successful people is this:

“Never spend future income today.”

This means avoiding unnecessary EMI purchases whenever possible. Debt steals future financial freedom.

Escape Debt Trap: 7 Proven ₹15000 Hacks-Another important discipline habit is learning basic financial education regularly. Read finance blogs, watch educational videos, and understand money management slowly. Financial knowledge improves confidence and reduces costly mistakes.

Most importantly, stop expecting instant transformation. Financial discipline develops gradually through repeated small actions.

Escape Debt Trap: 7 Proven ₹15000 Hacks-Best Cheap Foods To Reduce Monthly Expenses

Food expenses consume a large portion of low-income salaries. However, smart food planning can reduce costs without harming health.

The biggest mistake many people make is depending too much on food delivery apps. Convenience feels attractive, but daily ordering destroys budgets quickly.

Simple homemade Indian meals remain one of the cheapest and healthiest options. Rice, dal, vegetables, eggs, poha, oats, and seasonal fruits provide affordable nutrition.

Buying groceries monthly instead of daily also reduces expenses significantly. Wholesale markets usually offer better prices compared to local convenience stores.

Escape Debt Trap: 7 Proven ₹15000 Hacks-Another powerful strategy is meal preparation. Cooking larger quantities saves both money and time. For example, preparing lunch at home instead of buying outside food daily can save several thousand rupees yearly.

Tea and snack expenses should also be monitored carefully. Many people spend ₹50 to ₹100 daily without realizing the long-term impact. Small daily expenses become massive yearly losses.

In addition, avoid wasting food. Food wastage equals direct money wastage. Plan grocery purchases carefully according to actual needs.

Healthy eating does not require expensive products. Marketing often creates the illusion that good health requires costly packaged foods. In reality, simple traditional Indian meals are both economical and nutritious.

Escape Dangerous Debt Trap With ₹15000 Monthly Income By Avoiding Financial Scams

Financially stressed people often become easy targets for scams. When someone desperately wants quick money, fake schemes start looking attractive.

Many scams promise unrealistic returns like doubling money quickly, guaranteed trading profits, instant online income, or easy passive income. These schemes usually target financially vulnerable people.

If something sounds too good to be true, it is probably fake.

Avoid borrowing money through unknown apps or illegal lending platforms. Many apps charge extremely high interest rates and use harassment tactics later.

Similarly, avoid gambling, betting apps, and lottery addiction. Many people lose even more money while trying to solve financial problems quickly.

Escape Debt Trap: 7 Proven ₹15000 Hacks-Crypto scams and fake investment courses also trap desperate earners frequently. Always research carefully before investing any money.

Trusted financial information should come from reliable sources like:

SEBI India

National Stock Exchange India

Remember one important truth:

Slow financial growth is still better than fast financial destruction.

Escape Dangerous Debt Trap With ₹15000 Monthly Income Through Smart Goal Setting

Financial goals provide direction during difficult times. Without goals, budgeting feels frustrating and meaningless.

Your first financial goal should be survival stability. This means paying rent, food, utilities, and essential expenses comfortably every month.

The second goal should be emergency savings.

The third goal becomes complete debt freedom.

Finally, long-term wealth building can begin.

Break large goals into smaller monthly targets. For example:

Save ₹1000 this month

Repay one small debt in three months

Build ₹10000 emergency fund in one year

Escape Debt Trap: 7 Proven ₹15000 Hacks-Small targets create momentum and confidence.

Another effective method is writing goals physically on paper. Visible goals improve commitment psychologically.

In addition, review progress every month honestly. If mistakes happen, adjust strategy without guilt. Financial growth is a learning process.

People often quit because they expect perfection immediately. However, consistency matters more than perfection.

Escape Debt Trap: 7 Proven ₹15000 Hacks-How Families Can Support Financial Recovery

Debt recovery becomes easier when families cooperate together. Unfortunately, many households avoid discussing money problems openly. This creates confusion and stress.

Transparent conversations improve financial teamwork. Family members should understand income limitations clearly. Once everyone supports budgeting goals, unnecessary expenses reduce naturally.

Children can also learn valuable money habits early. Teaching basic savings and budgeting creates lifelong financial discipline.

Couples should avoid blame during financial struggles. Instead of fighting emotionally, focus on solving problems practically together.

Simple family activities like eating at home, reducing unnecessary shopping, and planning expenses collectively strengthen financial recovery.

Emotional support matters greatly during debt repayment journeys. Encouragement from family reduces stress and increases motivation significantly.

Best Free Tools For Budget Planning

You do not need expensive financial software to manage money effectively. Many free tools work perfectly for low-income budgeting.

Escape Debt Trap: 7 Proven ₹15000 Hacks-Google Sheets helps track expenses manually.

Mobile apps like Walnut, Money Manager, and Goodbudget simplify daily tracking.

Simple notebooks also work surprisingly well. The method matters less than consistency.

Set weekly reminders to review spending habits. Small weekly corrections prevent larger financial problems later.

The key is awareness. The moment you know exactly where money goes, financial control becomes easier.

Escape Debt Trap: 7 Proven ₹15000 Hacks-Why Emergency Loans Make Debt Worse

Many people try to solve old debt using new loans. Initially, this feels helpful because immediate pressure reduces temporarily. However, long-term financial stress usually becomes worse.

Emergency loans often carry high interest rates. Therefore, repayment burdens increase rapidly.

In addition, taking multiple loans creates mental exhaustion. Managing different EMI dates, lenders, and payment amounts increases anxiety significantly.

Instead of taking new loans, focus on:

Expense reduction

Income increase

Negotiating repayment plans

Selling unused assets temporarily

Borrowing should always remain the last option, not the first solution.

Mindset Shift Needed For Financial Freedom

The biggest transformation required to Escape Dangerous Debt Trap With ₹15000 Monthly Income is mental, not financial.

Escape Debt Trap: 7 Proven ₹15000 Hacks-You must stop seeing yourself as helpless.

Low income may create limitations, but smart decisions still create progress. Every financially stable person started somewhere. Wealth grows slowly through discipline, patience, and consistency.

Stop believing that financial freedom is only for rich people. Financial stability begins with habits, not salary size.

Most importantly, stop feeling ashamed about your financial struggles. Millions of hardworking people face similar challenges today. What matters is your willingness to improve the situation gradually.

Focus on progress instead of perfection.

Even reducing one unnecessary expense matters.

Even saving ₹50 matters.

Even repaying one small EMI matters.

Escape Debt Trap: 7 Proven ₹15000 Hacks-Small financial improvements repeated consistently create life-changing results over time.

Frequently Asked Questions

What is the fastest way to Escape Dangerous Debt Trap With ₹15000 Monthly Income?

The fastest method is combining strict budgeting, side income, and aggressive debt repayment while avoiding new loans completely.

Can I save money with ₹15000 monthly income?

Yes, small savings are possible with proper budgeting and controlled spending habits.

Should I use credit cards during debt repayment?

No, avoid using credit cards during financial recovery because they increase spending temptation and interest burden.

How much emergency fund should I build first?

Start with one month of expenses first. Then slowly expand toward three to six months of savings.

Is side income necessary for debt freedom?

Although not compulsory, side income accelerates debt repayment and reduces financial stress significantly.

Conclusion

Escape Dangerous Debt Trap With ₹15000 Monthly Income may seem difficult today, but it is absolutely possible with discipline and patience. Financial freedom does not happen through luck. It happens through consistent smart decisions repeated every month.

Start by understanding your expenses honestly. Build a realistic budget. Reduce unnecessary spending. Avoid new debt completely. Increase income slowly through side work. Most importantly, stay consistent even when progress feels slow.

Your current salary does not decide your future permanently. Your financial habits decide it. Many people earning high salaries remain trapped in debt because they lack discipline. Meanwhile, some low-income earners build stable financial lives through smart planning.

Take action today instead of waiting for the perfect moment. Even one small financial improvement this month can change your future direction completely.

2 thoughts on “Escape Debt Trap: 7 Proven ₹15000 Hacks”