UPI Credit Line Vs Personal Loan: Ultimate 2026 many Indians are asking in 2026. Digital lending is growing rapidly, and people now want instant money without lengthy paperwork or waiting for bank approvals. Because of this, UPI Credit Line services are becoming extremely popular among salaried employees, freelancers, students, and even small business owners. However, many borrowers still do not understand whether a UPI Credit Line is actually cheaper than a traditional personal loan or if it only looks convenient on the surface.

UPI Credit Line Vs Personal Loan: Ultimate 2026-Imagine this situation. Your salary gets delayed, an emergency expense suddenly appears, or your bike repair bill becomes bigger than expected. In such moments, you need fast access to money. Traditionally, people used personal loans for these situations. But now, banks and fintech companies offer UPI Credit Lines directly through UPI apps. With just a few taps, users can borrow instantly and pay later. This convenience looks attractive, but convenience does not always mean lower cost.

UPI Credit Line Vs Personal Loan: Ultimate 2026-The reality is that both options work differently. A personal loan usually gives a lump sum amount with fixed EMI payments, while a UPI Credit Line acts more like a revolving credit facility where interest is charged only on the amount used. Therefore,

choosing the wrong option can increase your financial burden significantly over time. Some people save money using UPI Credit Line wisely, while others end up paying higher interest due to poor repayment habits.

In this detailed guide, you will understand UPI Credit Line Vs Personal Loan Which Is Cheaper from every possible angle including interest rates, hidden fees, repayment flexibility, credit score impact, approval process, risk factors, and real-life financial examples. By the end of this article, you will clearly know which borrowing option matches your financial situation and helps you save more money in 2026.

Table of Contents

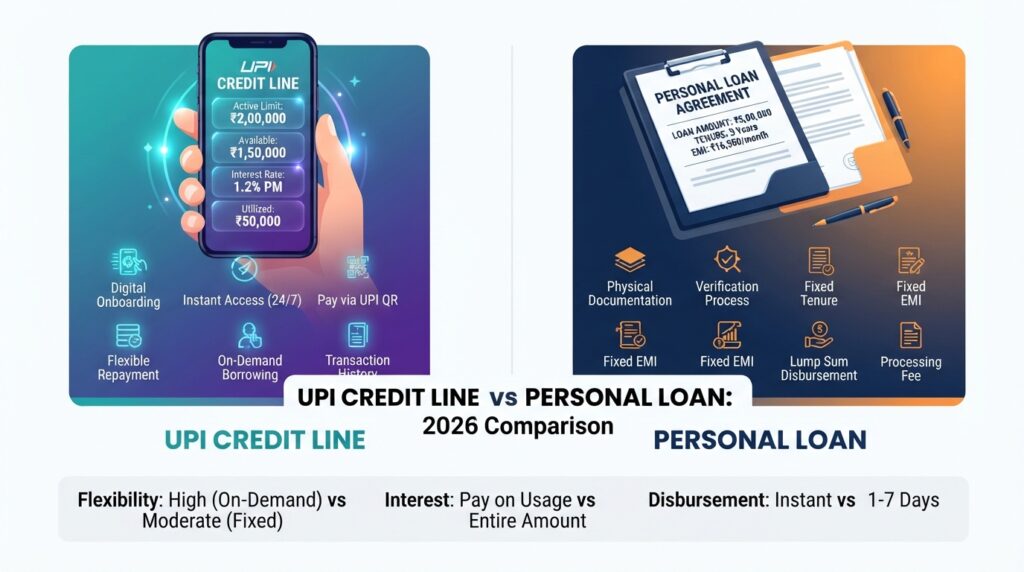

What Is A UPI Credit Line And How Does It Work

UPI Credit Line is a digital borrowing facility connected directly to your UPI account. Instead of linking only a savings account to UPI apps, users can now connect a pre-approved credit line provided by banks or financial institutions. This allows users to make payments even if their bank balance is low because the payment amount gets borrowed from the approved credit limit instantly.

UPI Credit Line Vs Personal Loan: Ultimate 2026-The biggest advantage of a UPI Credit Line is flexibility. You do not need to take a full loan amount at once. For example, if your bank approves a credit limit of ₹1 lakh, you can use only ₹5,000 or ₹10,000 whenever needed. Interest gets charged only on the used amount instead of the entire sanctioned limit. Because of this feature, many users believe UPI Credit Line Vs Personal Loan Which Is Cheaper clearly favors UPI Credit Line for short-term borrowing needs.

Another major reason behind the popularity of UPI Credit Line is speed. Traditional loans often require documentation, income proof, verification calls, and waiting periods. However, UPI Credit Line approvals are often instant for eligible customers. Banks already analyze transaction history, salary credits, and credit scores to provide pre-approved offers. Therefore, the process becomes smooth and highly convenient.

However, convenience can become dangerous if users are careless. Many people treat UPI Credit Line like free money and overspend. Since payments happen directly through UPI apps, users often forget they are borrowing. As a result, repayment discipline becomes extremely important. Missing payments may increase interest charges and negatively impact the credit score.

UPI Credit Line Vs Personal Loan: Ultimate 2026-Banks also apply different interest structures. Some charge daily interest, while others charge monthly rates. Additionally, late payment penalties and processing fees may apply. Therefore, understanding all terms carefully is necessary before using this facility regularly.

In India, UPI Credit Line adoption is growing rapidly because digital payments have already become part of daily life. From grocery stores to online shopping platforms, users can pay everywhere using UPI. Therefore, integrating credit directly into UPI creates a seamless borrowing experience that traditional loans cannot match in terms of convenience and speed.

What Is A Personal Loan And Why People Still Prefer It

A personal loan is an unsecured loan provided by banks, NBFCs, and digital lenders where borrowers receive a fixed amount upfront and repay it through monthly EMIs over a specific tenure. Unlike a UPI Credit Line, a personal loan follows a structured repayment system. This makes budgeting easier because borrowers know exactly how much EMI they must pay every month.

Even in 2026, millions of Indians still prefer personal loans despite the rise of digital credit systems. The biggest reason is predictability. In the debate around UPI Credit Line Vs Personal Loan Which Is Cheaper, many financially disciplined users prefer personal loans because fixed EMIs help avoid uncontrolled borrowing behavior.

Personal loans are commonly used for large expenses such as weddings, medical emergencies, home renovation, travel, education, or debt consolidation. Since the loan amount gets credited directly into the bank account, borrowers can use the money for almost any purpose without restrictions. Loan tenure usually ranges from 12 months to 7 years depending on eligibility and lender policies.

UPI Credit Line Vs Personal Loan: Ultimate 2026-Another major advantage is lower interest rates for eligible borrowers. Salaried employees with strong credit scores often get attractive interest rates from banks. In many cases, long-term personal loans become cheaper than continuously revolving short-term digital credit.

UPI Credit Line Vs Personal Loan: Ultimate 2026-However, personal loans also have disadvantages. Approval processes can still take time for some applicants. Documentation requirements may include salary slips, bank statements, PAN card, Aadhaar card, and employment verification. Additionally, once the loan is approved, interest starts on the full amount immediately even if the borrower does not use the entire money.

For example, if someone takes a ₹2 lakh personal loan but only needs ₹50,000 immediately, interest still applies to the full ₹2 lakh amount. This is where UPI Credit Line may appear more cost-efficient for smaller or unpredictable expenses.

UPI Credit Line Vs Personal Loan: Ultimate 2026-Despite these limitations, personal loans provide financial structure. Borrowers know their repayment schedule clearly, which reduces confusion. Furthermore, fixed repayment builds financial discipline and improves credit history when EMIs are paid on time.

Therefore, understanding your borrowing habits becomes extremely important before deciding between these two options. Some users benefit from flexibility, while others benefit from structure and predictability.

UPI Credit Line Vs Personal Loan Which Is Cheaper For Interest Rates

Interest rate comparison is the most important factor when discussing UPI Credit Line Vs Personal Loan Which Is Cheaper. Many people assume digital credit automatically means lower cost, but the truth depends entirely on borrowing duration, repayment behavior, and lender policies.

UPI Credit Line interest rates usually range between 12% and 24% annually depending on the bank, credit score, and repayment history. Some fintech lenders may even charge higher effective annualized rates for small-ticket short-term borrowing. Since interest is calculated only on the utilized amount, short-term users often save money compared to traditional loans.

For example, if you borrow ₹5,000 using a UPI Credit Line for 10 days and repay quickly, your interest cost may remain very low. In such cases, UPI Credit Line becomes cheaper than taking a personal loan with processing fees and fixed tenure obligations.

UPI Credit Line Vs Personal Loan: Ultimate 2026-On the other hand, personal loan interest rates usually range from 10% to 18% annually for salaried individuals with good credit profiles. Since the interest rate is often lower than revolving digital credit, personal loans become cheaper for larger amounts and longer repayment durations.

Let us understand with a simple example. Suppose someone needs ₹3 lakh for medical treatment. Using a UPI Credit Line continuously for several months may generate higher cumulative interest compared to a structured personal loan EMI. However, if someone only needs ₹15,000 temporarily for a few days, taking a full personal loan makes little sense.

UPI Credit Line Vs Personal Loan: Ultimate 2026-Hidden charges also matter significantly. Personal loans may include processing fees, foreclosure charges, documentation fees, and late penalties. UPI Credit Lines may charge convenience fees, late payment interest, and annual maintenance fees depending on the provider.

Therefore, there is no universal winner in the UPI Credit Line Vs Personal Loan Which Is Cheaper debate. The cheapest option depends on how responsibly and strategically the borrower uses the credit facility.

Financial experts often recommend using UPI Credit Lines only for short-term liquidity gaps and using personal loans for planned large expenses. This strategy minimizes unnecessary interest burden while maintaining financial flexibility.

UPI Credit Line Vs Personal Loan: Ultimate 2026-Which Option Is Better For Emergency Expenses

UPI Credit Line Vs Personal Loan: Ultimate 2026-Emergencies create panic, and during stressful situations people often make poor borrowing decisions. Therefore, understanding UPI Credit Line Vs Personal Loan Which Is Cheaper during emergencies can save significant money and reduce future financial stress.

UPI Credit Line performs extremely well during sudden short-term emergencies. Suppose your salary arrives after three days but your electricity bill or urgent medicine expense must be paid immediately. In such situations, instant access to small amounts through UPI becomes incredibly useful. Since approval is usually pre-approved, money becomes available instantly without lengthy verification.

Additionally, users pay interest only on the amount utilized. Therefore, short repayment periods keep total borrowing cost lower. This makes UPI Credit Line ideal for temporary cash flow shortages.

UPI Credit Line Vs Personal Loan: Ultimate 2026-However, emergencies involving large expenses require different planning. Medical surgeries, family crises, educational payments, or major repairs may require lakhs of rupees. In such cases, personal loans usually provide better repayment structure and lower long-term interest burden.

One major psychological advantage of personal loans is controlled repayment planning. Since borrowers receive a fixed EMI schedule, they can organize their monthly budget accordingly. This reduces uncertainty and emotional financial pressure.

Another important factor is repayment tenure. UPI Credit Lines generally expect faster repayment cycles. Delayed repayment may trigger high penalties or revolving interest accumulation. Personal loans provide longer repayment flexibility ranging from one year to several years depending on eligibility.

UPI Credit Line Vs Personal Loan: Ultimate 2026-People often underestimate emotional stress during emergencies. Fast digital borrowing feels convenient initially, but repeated borrowing without repayment discipline can create a debt cycle. Therefore, borrowers must evaluate not only interest rates but also their repayment capacity honestly.

UPI Credit Line Vs Personal Loan: Ultimate 2026-A balanced strategy works best for many households. Small urgent payments can be managed through UPI Credit Line, while large planned emergency expenses may be better financed through personal loans. Smart financial planning always focuses on repayment comfort rather than just instant access to money.

Hidden Charges Most Borrowers Ignore Completely

When people compare UPI Credit Line Vs Personal Loan Which Is Cheaper, they usually focus only on interest rates. However, experienced borrowers know that hidden charges often increase the real borrowing cost much more than expected. Many users take quick loans without reading detailed terms and conditions carefully. Later, they become shocked after seeing additional charges deducted from their account.

UPI Credit Line providers sometimes advertise attractive low interest rates, but users may still face convenience fees, late payment charges, annual maintenance fees, auto-debit failure penalties, GST on processing fees, and even inactivity charges in some cases. Since many digital lenders use automated systems, penalties may apply immediately after missed due dates without manual reminders. Therefore, borrowers who delay payments even for a few days may end up paying significantly more.

UPI Credit Line Vs Personal Loan: Ultimate 2026-Another important factor is compounding frequency. Some UPI Credit Line systems calculate interest daily. If users continuously delay repayment or partially repay dues, the interest burden can increase rapidly. Therefore, while discussing UPI Credit Line Vs Personal Loan Which Is Cheaper, borrowers must always calculate the effective annual borrowing cost instead of checking only the advertised interest percentage.

Personal loans also include hidden expenses. Banks may charge processing fees ranging from 1% to 3% of the sanctioned amount. Some lenders additionally charge documentation fees, stamp duty charges, prepayment penalties, and foreclosure charges. Suppose a borrower takes a ₹5 lakh personal loan. Even a 2% processing fee means ₹10,000 gets deducted immediately before disbursement.

Many borrowers ignore insurance add-ons too. Some lenders automatically attach loan protection insurance policies that increase the total borrowing amount. Since these charges are often added silently into the EMI structure, people fail to notice the actual cost increase.

Therefore, smart borrowers always compare the Annual Percentage Rate instead of looking only at interest rates. APR includes additional charges and provides a clearer understanding of total borrowing cost. Financial awareness becomes extremely important because marketing advertisements often highlight only attractive numbers while hiding expensive conditions in small text.

Before borrowing, always check processing fees, foreclosure rules, penalty structures, repayment flexibility, and interest calculation methods carefully. Reading terms for ten minutes can save thousands of rupees later.

UPI Credit Line Vs Personal Loan: Ultimate 2026-EMI Comparison Between UPI Credit Line And Personal Loan

EMI structure is one of the biggest practical differences in the debate around UPI Credit Line Vs Personal Loan Which Is Cheaper. Understanding repayment patterns helps borrowers avoid financial pressure and choose the right credit product according to their income stability.

UPI Credit Line Vs Personal Loan: Ultimate 2026-Personal loans follow a fixed EMI structure. This means borrowers know exactly how much they need to pay every month throughout the tenure. Fixed EMIs make budgeting easier because expenses remain predictable. Salaried employees often prefer this system because salary inflow happens monthly, making EMI planning straightforward.

For example, suppose someone borrows ₹2 lakh for three years at a fixed interest rate. The monthly EMI remains almost unchanged throughout the tenure. Therefore, borrowers can manage household expenses systematically without worrying about fluctuating repayment amounts.

UPI Credit Line works differently. Instead of fixed EMI structures, repayment depends on the utilized amount and repayment timeline. Some banks allow flexible minimum due payments, while others require repayment within shorter billing cycles. Therefore, monthly obligations may change constantly depending on usage patterns.

This flexibility looks attractive initially, but it can become risky for financially undisciplined users. People may continue spending repeatedly without realizing how quickly outstanding dues are growing. Since there is no fixed long-term structure like traditional loans, users sometimes underestimate the repayment burden.

However, flexibility also creates advantages for disciplined borrowers. Suppose someone borrows ₹8,000 for only seven days using a UPI Credit Line. Paying interest only for seven days may cost much less than taking a long-term personal loan with fixed EMIs and processing fees. Therefore, short-duration borrowing strongly favors UPI Credit Line.

Another major difference is prepayment flexibility. Many personal loans charge foreclosure penalties if borrowers repay early. On the other hand, several UPI Credit Line systems allow repayment anytime without extra charges. This feature helps users reduce interest burden faster.

Borrowers with irregular income patterns such as freelancers, small business owners, and gig workers may find flexible repayment systems more convenient than fixed EMIs. However, salaried employees with stable income may benefit more from structured EMI systems because they encourage financial discipline.

UPI Credit Line Vs Personal Loan: Ultimate 2026-Ultimately, the better option depends on borrowing duration, income consistency, and repayment habits. Financial products should match lifestyle patterns instead of following trends blindly.

Credit Score Impact You Must Understand Carefully

Your credit score controls your future borrowing power. Unfortunately, many people focus only on instant loan approval while ignoring long-term credit consequences. In reality, understanding UPI Credit Line Vs Personal Loan Which Is Cheaper also requires analyzing how each option affects your credit profile.

Both products impact credit scores because lenders report repayment activity to credit bureaus. Timely payments improve your creditworthiness, while missed payments damage your score significantly. However, usage patterns create different impacts in both systems.

UPI Credit Line Vs Personal Loan: Ultimate 2026-Personal loans usually help build structured credit history. Since EMIs remain fixed and repayment schedules are clearly defined, consistent payments demonstrate financial responsibility. Over time, this improves borrower credibility and increases eligibility for future loans at lower interest rates.

UPI Credit Line behaves more like revolving credit. Therefore, utilization ratio becomes important. If borrowers continuously use a very high percentage of their available credit limit, credit bureaus may interpret this as financial stress. For example, constantly utilizing 90% of the available credit line can negatively affect credit health even if minimum payments are made regularly.

Another important issue involves missed repayments. Since UPI Credit Line operates digitally and instantly, some users forget repayment deadlines completely. Automated penalties and delayed payment reporting can quickly damage credit scores. Many young borrowers underestimate this risk because digital borrowing feels casual compared to traditional loans.

UPI Credit Line Vs Personal Loan: Ultimate 2026-On the positive side, responsible use of UPI Credit Line can strengthen credit history for people with limited borrowing records. Young professionals, students, or first-time borrowers may build healthy financial profiles through disciplined small-ticket borrowing and timely repayments.

Loan inquiries also matter. Applying for multiple personal loans within short periods may create several hard inquiries on your credit report, slightly reducing your score temporarily. Pre-approved UPI Credit Lines sometimes involve softer approval mechanisms, depending on the lender.

Experts recommend maintaining low utilization ratios, paying dues before deadlines, and avoiding unnecessary borrowing regardless of the product chosen. The cheapest loan is meaningless if poor repayment behavior destroys future financial opportunities.

UPI Credit Line Vs Personal Loan: Ultimate 2026-Therefore, when comparing UPI Credit Line Vs Personal Loan Which Is Cheaper, borrowers should think beyond immediate cost and consider long-term credit health carefully.

Which Option Is Safer For Young Professionals

Young professionals in India are becoming major users of digital credit systems. Fast salary growth, online shopping habits, lifestyle spending, and fintech convenience are changing borrowing behavior rapidly. Therefore, the question of UPI Credit Line Vs Personal Loan Which Is Cheaper becomes extremely relevant for first-job employees and young earners.

UPI Credit Line Vs Personal Loan: Ultimate 2026-UPI Credit Line feels highly attractive to younger users because it integrates directly with everyday digital payment apps. There is no need for lengthy forms, physical branch visits, or complicated paperwork. Users can borrow instantly during emergencies or temporary cash shortages.

UPI Credit Line Vs Personal Loan: Ultimate 2026-However, this convenience creates a hidden psychological risk. Easy borrowing often encourages impulsive spending. Young users may purchase gadgets, expensive dining experiences, subscriptions, or travel bookings without realizing they are creating debt obligations. Since UPI payments happen instantly, spending feels less painful emotionally compared to traditional loans.

Personal loans create stronger psychological caution because the borrowing process feels formal and structured. Borrowers usually think carefully before applying for larger long-term loans. Therefore, personal loans may indirectly encourage more responsible borrowing behavior.

Another important factor is income stability. Many young professionals switch jobs frequently during early career stages. Fixed EMIs from personal loans may become stressful during career transitions or salary delays. Flexible UPI Credit Line repayment structures may provide better short-term liquidity management during uncertain income periods.

At the same time, excessive dependence on revolving digital credit can create debt traps. Some users borrow repeatedly to repay previous dues, creating continuous financial pressure. Therefore, financial maturity becomes extremely important when using UPI Credit Line systems regularly.

UPI Credit Line Vs Personal Loan: Ultimate 2026-Experts usually recommend using UPI Credit Line only for temporary liquidity gaps instead of lifestyle inflation. If the expense is non-essential and cannot be repaid quickly, borrowing may not be wise at all.

UPI Credit Line Vs Personal Loan: Ultimate 2026-Young earners should also prioritize emergency funds. Depending entirely on credit systems for unexpected expenses increases financial vulnerability. Building savings habits alongside disciplined credit usage creates long-term financial stability.

Ultimately, the safest option depends on financial discipline, spending habits, career stability, and repayment behavior rather than age alone.

UPI Credit Line Vs Personal Loan: Ultimate 2026-Real-Life Example Of Smart Borrowing Strategy

Understanding theory is useful, but real-life examples make financial decisions easier. Let us compare two borrowers to understand UPI Credit Line Vs Personal Loan Which Is Cheaper in practical situations.

Rahul works in a private company and earns ₹45,000 monthly. One month, his salary gets delayed because of company processing issues. Meanwhile, he needs ₹12,000 urgently for family medical expenses. Instead of taking a personal loan, Rahul uses his pre-approved UPI Credit Line connected to his banking app. He borrows ₹12,000 and repays the amount fully within ten days after receiving salary.

UPI Credit Line Vs Personal Loan: Ultimate 2026-Since Rahul used the money only for a short duration, his interest cost remained minimal. There were no lengthy approvals, processing delays, or large documentation requirements. In this case, UPI Credit Line clearly became the cheaper and smarter option.

UPI Credit Line Vs Personal Loan: Ultimate 2026-Now consider another example. Priya plans a home renovation project requiring ₹4 lakh. The project timeline extends over several months. Instead of using revolving digital credit repeatedly, she takes a structured personal loan at a competitive interest rate with fixed EMIs over four years.

UPI Credit Line Vs Personal Loan: Ultimate 2026 This decision helps Priya manage repayment comfortably. Her EMI fits within monthly budget planning, and the overall interest burden remains lower than continuously revolving high-utilization digital credit. In her case, personal loan becomes more affordable and financially stable.

UPI Credit Line Vs Personal Loan: Ultimate 2026-These examples show an important truth. Financial products are tools, not enemies or heroes. The smartest borrowers select products according to the specific situation rather than blindly following trends or advertisements.

Short-term liquidity needs generally favor UPI Credit Line because of flexibility and instant access. Long-term planned expenses usually favor personal loans because of structured repayment and potentially lower interest rates.

Therefore, instead of asking only which option is cheaper universally, borrowers should ask which option matches the exact purpose, repayment timeline, and financial discipline level.

UPI Credit Line Vs Personal Loan: Ultimate 2026 Biggest Mistakes Borrowers Make While Choosing Loans

Many people face financial stress not because borrowing itself is wrong, but because they make avoidable mistakes while choosing credit products. Understanding these mistakes is extremely important while comparing UPI Credit Line Vs Personal Loan Which Is Cheaper.

UPI Credit Line Vs Personal Loan: Ultimate 2026-The first major mistake is borrowing without repayment planning. Many users focus only on approval speed and ignore future repayment pressure. Easy digital access creates false confidence. However, borrowed money always requires disciplined repayment regardless of convenience.

The second mistake involves ignoring total borrowing cost. Borrowers often compare only interest percentages while ignoring processing fees, penalty charges, GST, convenience fees, and compounding structures. As discussed earlier, hidden charges significantly impact real borrowing cost.

UPI Credit Line Vs Personal Loan: Ultimate 2026-Another dangerous mistake is using credit for lifestyle inflation instead of genuine needs. Expensive smartphones, luxury shopping, unnecessary travel, and impulsive purchases funded through revolving credit systems can quickly create debt cycles.

UPI Credit Line Vs Personal Loan: Ultimate 2026-Many people also misunderstand minimum due payments. Paying only minimum dues may prevent immediate penalties temporarily, but interest continues accumulating on outstanding balances. Over time, repayment becomes much more expensive.

Some borrowers apply for multiple credit products simultaneously. Frequent loan applications create several hard inquiries on credit reports, reducing credit scores temporarily and signaling financial desperation to lenders.

Ignoring emergency savings is another common problem. People increasingly depend entirely on credit systems for unexpected expenses instead of building financial cushions gradually. This dependency increases vulnerability during job losses or income disruptions.

Lastly, emotional borrowing creates serious long-term problems. Stress, social pressure, and instant gratification often influence borrowing decisions more than rational financial planning. Smart borrowers separate emotions from financial decisions and analyze repayment capacity honestly before borrowing.

Avoiding these mistakes improves financial stability significantly regardless of whether you choose UPI Credit Line or personal loans.

UPI Credit Line Vs Personal Loan: Which One Saves More Money in 2026?

UPI Credit Line Vs Personal Loan is becoming one of the biggest questions for anyone planning to borrow money in today’s digital banking era. Traditional borrowing is changing rapidly. Instead of visiting a bank branch, people now expect instant approvals, digital verification, and flexible repayment options. As a result, both products have become popular, but choosing the wrong one can increase borrowing costs and create unnecessary financial pressure.

UPI Credit Line Vs Personal Loan: Ultimate 2026-I have seen many people assume that every borrowing option works in the same way. However, after comparing different lending products and listening to financial experts, I found that each solution serves a completely different purpose.

A small emergency expense may be better suited to one option, while a planned major purchase may benefit from another. Understanding these differences before borrowing can help you avoid expensive mistakes later.

This guide explains every important aspect in simple language. Rather than promoting one product over the other, the goal is to help you understand when each option makes sense, what risks to watch for, and how to make smarter borrowing decisions in 2026.

Quick Summary

| Feature | UPI Credit Line | Personal Loan |

|---|---|---|

| Credit Type | Revolving Credit | Lump Sum Loan |

| Money Received | Use When Needed | Entire Amount Together |

| Repayment | Flexible | Fixed EMI |

| Interest | On Used Amount | On Full Loan Amount |

| Best For | Daily & Short-Term Needs | Planned Large Expenses |

| Flexibility | High | Moderate |

| Documentation | Usually Simple | May Be More Detailed |

| Borrowing Style | Digital First | Traditional & Digital |

UPI Credit Line Vs Personal Loan: Ultimate 2026-Why UPI Credit Line Vs Personal Loan Is Becoming More Important

Digital payments have completely transformed the way people manage money. Today, many users expect borrowing to be just as convenient as making a payment. This shift has encouraged financial institutions to introduce credit products that integrate directly with payment systems, allowing approved users to access credit almost instantly.

At the same time, personal loans remain one of the most trusted borrowing options because they provide a fixed amount with predictable monthly repayments. For major expenses such as education, medical treatment, home improvements, or business investments, structured repayment often provides greater financial discipline.

UPI Credit Line Vs Personal Loan: Ultimate 2026-The growing popularity of both options means borrowers must understand their differences before making a decision. Selecting the wrong product can increase interest costs, reduce cash flow flexibility, or create repayment challenges. On the other hand, choosing the right borrowing method can improve financial management and reduce overall borrowing expenses.

From my experience reading financial reports and observing lending trends, I have noticed that informed borrowers usually focus on the total borrowing cost rather than only the speed of approval. That simple mindset often leads to better long-term financial decisions.

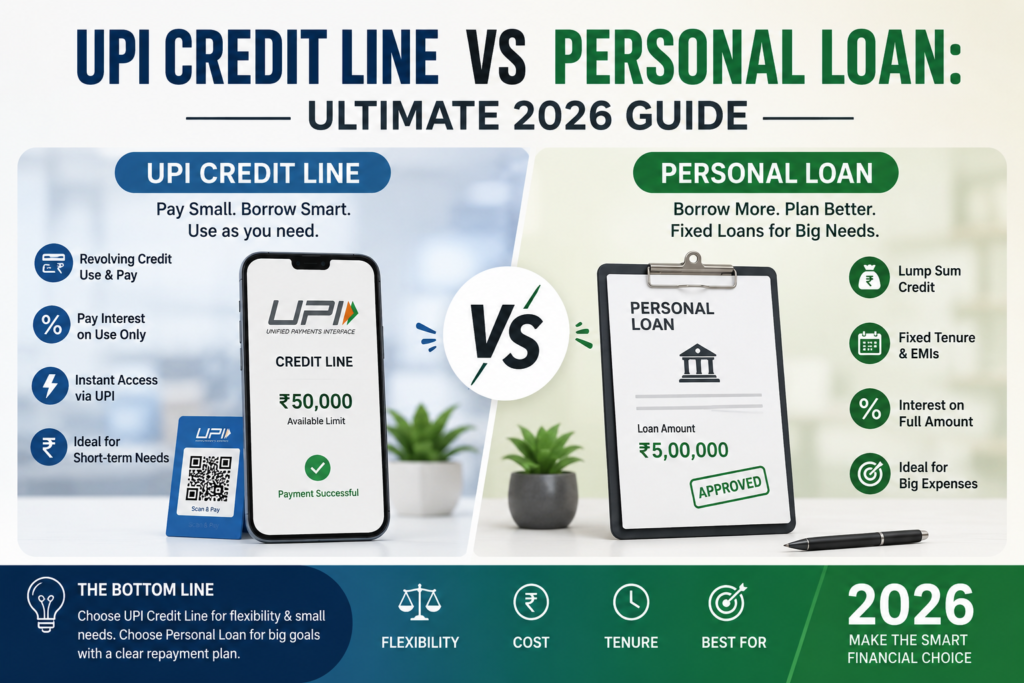

Understanding UPI Credit Line Vs Personal Loan From the Basics

Many beginners believe these products are almost identical because both allow people to borrow money. In reality, they work very differently.

A UPI Credit Line provides access to a pre-approved borrowing limit. Instead of receiving all the money at once, borrowers can use only the amount they need. Interest is generally charged only on the amount used, making it suitable for short-term funding needs and better cash flow management.

A Personal Loan works differently. After approval, the entire loan amount is disbursed in one transaction. Repayment follows a fixed schedule through monthly installments until the loan is completely repaid. This structure helps borrowers plan their finances because the repayment amount remains predictable.

Understanding this basic distinction is essential because it affects borrowing costs, repayment flexibility, and long-term financial planning.

UPI Credit Line Vs Personal Loan: Ultimate 2026-UPI Credit Line Vs Personal Loan: How They Actually Work

When someone receives approval for a UPI Credit Line, they are given a borrowing limit rather than immediate cash. Every time they make an eligible payment using that facility, only the amount used becomes part of the outstanding balance. As repayments are made, the available credit limit becomes usable again, making it similar to a revolving credit system.

A Personal Loan follows a completely different structure. Once approved, the borrower receives the entire sanctioned amount. Monthly repayments begin according to the agreed schedule until the outstanding balance reaches zero. Unlike a revolving facility, the repaid amount cannot usually be borrowed again without submitting a new loan application.

This operational difference directly affects interest calculations, repayment planning, and overall borrowing flexibility. Understanding how each system functions helps borrowers select the product that matches their actual financial requirement instead of simply choosing the option that appears more convenient.

UPI Credit Line Vs Personal Loan: Ultimate 2026-When UPI Credit Line Makes More Sense

A revolving credit facility can be particularly useful when expenses are unpredictable. Instead of borrowing a large amount in advance, users access funds only when required. This can reduce unnecessary interest costs because borrowing remains limited to actual spending.

For example, someone managing occasional repair expenses, short-term cash flow gaps, or temporary business purchases may appreciate the flexibility offered by this borrowing method. Since funds remain available within the approved limit, repeated applications are usually unnecessary for every small financial requirement.

I have seen that people with disciplined spending habits often benefit more from flexible borrowing because they avoid paying interest on money they never actually use. However, responsible repayment remains essential, as carrying outstanding balances for extended periods can increase borrowing costs.

UPI Credit Line Vs Personal Loan: Ultimate 2026-UPI Credit Line Vs Personal Loan: Complete Feature Comparison

Choosing between UPI Credit Line Vs Personal Loan becomes much easier when you compare their features instead of looking only at the borrowing amount. Although both provide access to credit, their purpose, repayment style, flexibility, and cost can differ significantly. A UPI Credit Line is generally designed for flexible borrowing where you use only what you need within an approved limit.

In contrast, a Personal Loan provides the entire sanctioned amount at once, making it suitable for planned expenses. I have seen that many borrowers focus only on quick approval and forget to compare long-term repayment obligations.

That approach often leads to paying more interest than necessary. Before applying, compare flexibility, repayment schedule, available borrowing limit, interest calculation method, processing fees, prepayment rules, and overall convenience. Looking at these factors together gives a much clearer picture than comparing interest rates alone.

Understanding these practical differences helps borrowers make informed decisions based on actual financial needs instead of marketing claims.

Comparison at a Glance

| Feature | UPI Credit Line | Personal Loan |

|---|---|---|

| Credit Type | Revolving | Fixed Loan |

| Amount Received | Use as Needed | Full Amount Together |

| Repayment | Flexible | Fixed EMI |

| Interest Charged | Usually on Used Amount | Entire Outstanding Amount |

| Best For | Short-Term Expenses | Large Planned Expenses |

| Reusable Limit | Usually Yes | No |

| Budget Planning | Flexible | Predictable |

| Loan Tenure | Varies | Fixed |

| Digital Convenience | High | High |

UPI Credit Line Vs Personal Loan: Ultimate 2026-Interest Cost: Which Can Save More Money?

One of the biggest misunderstandings about UPI Credit Line Vs Personal Loan is that borrowers compare only the advertised interest rate. In reality, the total borrowing cost depends on how much money you borrow, how long you keep it outstanding, and how consistently you make repayments. A revolving credit facility may cost less if you borrow only a small amount for a short period because interest generally applies only to the amount actually used. On the other hand, if someone needs a large amount for a planned purchase and intends to repay over several years, a structured Personal Loan may provide better predictability.

I have listened to experienced financial advisors explain that borrowers should always calculate the total repayment amount instead of comparing percentages alone. Hidden costs, processing charges, late payment fees, and prepayment conditions also influence the final borrowing expense. Looking at the complete financial picture often leads to a smarter decision than chasing the lowest advertised rate.

Factors That Influence Total Borrowing Cost

- Interest calculation method

- Processing charges

- Late payment penalties

- Prepayment conditions

- Repayment period

- Outstanding balance

- Additional service fees

- Credit profile

UPI Credit Line Vs Personal Loan: Ultimate 2026-Eligibility Comparison

Eligibility plays an important role when evaluating UPI Credit Line Vs Personal Loan because approval depends on several financial factors. Different lenders may use different eligibility requirements, but most assess repayment capacity, previous borrowing behaviour, identity verification, and financial stability. Digital lending has simplified applications, yet responsible lending standards continue to remain important.

I have noticed that borrowers with organised financial records usually complete the approval process much more smoothly than those who apply without preparing their documents. Maintaining a healthy repayment history, avoiding frequent loan applications, and demonstrating stable income often improves approval chances. Rather than applying repeatedly with different lenders, it is usually wiser to understand eligibility before submitting an application. This approach reduces unnecessary credit enquiries and improves the overall borrowing experience.

Common Eligibility Factors

- Minimum age requirement

- Identity verification

- Income stability

- Credit assessment

- Banking relationship

- Existing financial obligations

- Digital verification

- Repayment capacity

UPI Credit Line Vs Personal Loan: Ultimate 2026-Flexibility: Which Borrowing Option Gives More Freedom?

Flexibility is where UPI Credit Line Vs Personal Loan shows one of the biggest differences. A revolving credit facility allows borrowers to access funds only when needed within an approved limit. This makes it suitable for situations where expenses are uncertain or occur at different times. A Personal Loan, however, is more structured. Borrowers receive a fixed amount and repay it through scheduled installments.

This disciplined repayment structure can help people who prefer predictable budgeting. My experience is that individuals who maintain detailed monthly budgets often appreciate fixed repayments because they know exactly how much must be paid every month. On the other hand, people with changing income patterns sometimes prefer borrowing only when required. Neither option is universally better. The right choice depends on personal financial habits, cash flow stability, and borrowing objectives.

UPI Credit Line Vs Personal Loan: Ultimate 2026-Advantages of UPI Credit Line

The growing popularity of UPI Credit Line Vs Personal Loan discussions is largely driven by the convenience offered by digital borrowing. A UPI Credit Line can provide several practical benefits for responsible borrowers.

Key Advantages

- Borrow only when required.

- Interest may apply only to the amount used.

- Digital transactions are convenient.

- Suitable for temporary cash-flow shortages.

- Credit becomes reusable after repayment.

- Often requires minimal paperwork.

- Faster access compared with many traditional borrowing methods.

- Better control over small recurring expenses.

These advantages make revolving credit particularly useful for disciplined borrowers who repay balances promptly and avoid unnecessary borrowing.

UPI Credit Line Vs Personal Loan: Ultimate 2026-Advantages of Personal Loan

A Personal Loan continues to remain one of the most trusted borrowing products because of its predictable structure. Borrowers receive the approved amount immediately and repay through regular installments. This approach helps with financial planning, especially when funding larger planned expenses.

I have seen many people successfully manage education expenses, home improvements, or business investments because fixed monthly repayments allowed them to organise their budgets more effectively. Another advantage is repayment certainty. Since the installment amount usually remains consistent throughout the repayment period, budgeting becomes easier. Borrowers who value stability often prefer this structured approach over flexible borrowing options.

UPI Credit Line Vs Personal Loan: Ultimate 2026-Disadvantages of UPI Credit Line

Every financial product has limitations, and UPI Credit Line Vs Personal Loan is no exception. Flexible borrowing can become expensive if users repeatedly carry outstanding balances without planning repayments. Easy digital access may also encourage unnecessary spending for some borrowers.

Since credit is readily available, maintaining financial discipline becomes extremely important. Another challenge is that borrowing limits may not always be sufficient for major planned purchases. Responsible use is therefore essential. Borrow only when necessary and create a repayment plan before spending.

Common Challenges

- Temptation to overspend

- Outstanding balances may grow quickly

- Not ideal for major planned purchases

- Requires strong repayment discipline

- Flexible borrowing can reduce budgeting discipline

UPI Credit Line Vs Personal Loan: Ultimate 2026-Disadvantages of Personal Loan

Although Personal Loans provide certainty, they also have certain limitations. Borrowers begin paying interest on the full loan amount after disbursement, even if part of the money remains unused initially. Fixed monthly repayments continue throughout the agreed tenure, reducing flexibility during unexpected financial situations. Some loans may also include processing fees or prepayment conditions depending on lender policies. Therefore, borrowers should always review the complete loan agreement carefully before accepting any offer.

Real-Life Example 1

Imagine someone renovating a home office over the next six months. Instead of spending everything immediately, expenses occur gradually as furniture, equipment, and repairs are completed. In this situation, borrowing only when each payment becomes necessary may reduce unnecessary interest costs. The flexibility offered by a revolving facility could match the spending pattern more effectively than receiving the full amount upfront.

Real-Life Example 2

Now consider someone paying an annual education fee that requires one complete payment before classes begin. In this case, receiving the entire amount immediately through a structured loan may provide better certainty and simpler repayment planning. The borrower knows exactly how much must be repaid every month until the loan is completed.

UPI Credit Line Vs Personal Loan: Ultimate 2026-Common Mistakes Borrowers Make

When comparing UPI Credit Line Vs Personal Loan, many people unintentionally make decisions that increase borrowing costs. Understanding these mistakes can save money and reduce financial stress.

Mistake 1: Looking Only at Interest Rate

The advertised rate tells only part of the story. Always compare total repayment cost.

Mistake 2: Borrowing More Than Necessary

Extra borrowing increases interest expenses without providing additional value.

Mistake 3: Ignoring Repayment Capacity

Never choose a borrowing option without calculating future monthly affordability.

Mistake 4: Not Reading Terms Carefully

Processing charges, penalties, repayment conditions, and additional fees should always be reviewed before accepting any borrowing agreement.

Mistake 5: Depending on Credit for Everyday Spending

Borrowing should support financial goals, not replace regular income.

UPI Credit Line Vs Personal Loan: Ultimate 2026-Experience and Expert Insight

UPI Credit Line Vs Personal Loan: Ultimate 2026-From my experience studying personal finance and comparing different borrowing methods, I have found that the smartest borrowers rarely choose the fastest option. Instead, they compare flexibility, repayment certainty,

overall borrowing cost, and future financial commitments. I have also listened to financial experts who consistently recommend borrowing with a clear repayment strategy instead of focusing only on approval speed. Responsible borrowing is usually less about finding the cheapest product and more about selecting the borrowing method that matches your financial situation and repayment ability.

UPI Credit Line Vs Personal Loan: Ultimate 2026-Advanced Strategies to Choose Between UPI Credit Line Vs Personal Loan

Selecting between UPI Credit Line Vs Personal Loan should never be based only on advertisements or instant approval messages. The better approach is to match the borrowing product with the purpose of borrowing. Before applying, ask yourself three questions: Why do I need this money? How long will I need it? How comfortably can I repay it? These simple questions often prevent expensive borrowing mistakes. I have seen that borrowers who spend ten minutes planning usually save far more money than those who apply immediately after seeing an attractive offer.

A practical strategy is to borrow the smallest amount necessary and repay it as early as possible. Shorter borrowing periods generally reduce the total interest paid. Another useful habit is reviewing your monthly cash flow before accepting any credit agreement. This helps ensure repayments remain manageable even if unexpected expenses arise. Smart borrowing is not about getting the highest limit; it is about using credit responsibly while protecting your long-term financial stability.

UPI Credit Line Vs Personal Loan: Ultimate 2026-Build an Emergency Buffer First

One lesson I have learned from observing personal finance habits is that borrowing should not become the first solution for every unexpected expense. Maintaining an emergency fund can reduce dependence on credit during temporary financial challenges. Even a modest reserve can prevent unnecessary borrowing for small repairs, medical costs, or urgent travel. When emergencies are covered by savings, borrowed money can be reserved for situations where it creates genuine value rather than filling routine spending gaps.

UPI Credit Line Vs Personal Loan: Ultimate 2026-Understanding the Psychology Behind Borrowing

An often-overlooked aspect of UPI Credit Line Vs Personal Loan is the psychology of spending. People tend to spend differently depending on how they receive money. Receiving a large lump sum can sometimes create the illusion of having more disposable cash, encouraging unnecessary purchases. On the other hand, having a revolving credit limit available at all times may tempt some people to make frequent small purchases that gradually accumulate into a significant balance.

I have noticed that disciplined borrowers usually separate needs from wants before borrowing. They create a repayment plan before spending the first unit of borrowed money. This mindset reduces financial stress and improves long-term money management. Responsible borrowing begins with self-control, not with choosing one product over another.

Risk Management Tips Before Borrowing

Every borrowing decision carries some level of financial responsibility. Whether comparing UPI Credit Line Vs Personal Loan or evaluating any other credit product, reducing risk should always be a priority.

UPI Credit Line Vs Personal Loan: Ultimate 2026-Practical Risk Management Checklist

- Borrow only what you genuinely need.

- Read every term and condition carefully.

- Understand how interest is calculated.

- Check processing fees and other applicable charges.

- Know the repayment schedule before accepting the offer.

- Keep enough monthly income available for repayments.

- Avoid borrowing from multiple sources simultaneously.

- Maintain a healthy repayment history.

- Review your budget every month.

- Keep records of every repayment.

Following these simple practices can reduce financial stress and improve your overall creditworthiness over time.

UPI Credit Line Vs Personal Loan: Ultimate 2026-Expert Checklist Before Choosing UPI Credit Line Vs Personal Loan

Before making a final decision, review this checklist carefully. It can help you compare options objectively instead of relying on marketing promises.

Financial Goal

Is the borrowing for a planned purchase or an unexpected expense?

Required Amount

Do you need the full amount immediately or only a portion over time?

Repayment Ability

Can you comfortably manage fixed monthly repayments, or do you need greater flexibility?

Total Cost

Have you compared the complete borrowing cost rather than only the advertised interest rate?

Financial Discipline

Will easy access to available credit encourage unnecessary spending?

Long-Term Financial Plan

Does this borrowing decision support your future financial goals?

Completing this checklist honestly often leads to a more confident borrowing decision.

E-E-A-T: Experience, Expertise, Authoritativeness, and Trustworthiness

A reliable financial decision should always be based on verified information, practical analysis, and responsible borrowing habits. While preparing this guide on UPI Credit Line Vs Personal Loan, I focused on explaining concepts rather than promoting a particular product. My experience is that people benefit most when financial advice remains transparent, balanced, and easy to understand.

I have also seen that comparing borrowing options objectively helps readers make informed decisions instead of emotional ones. Financial products continue to evolve, so borrowers should always verify the latest eligibility requirements, fees, and terms directly with the respective financial institution before applying.

Frequently Asked Questions

What is the main difference between UPI Credit Line Vs Personal Loan?

The biggest difference is how funds are accessed. A UPI Credit Line usually allows borrowing within an approved limit as needed, while a Personal Loan provides the complete sanctioned amount in one disbursement and is repaid through fixed installments.

Which option is better for short-term borrowing?

If you need smaller amounts occasionally and can repay quickly, a revolving credit facility may offer greater flexibility. However, the best choice always depends on your borrowing purpose and repayment capacity.

Which option is more suitable for large planned expenses?

For planned expenses that require a substantial amount upfront, a Personal Loan often provides better repayment structure and budgeting certainty.

Does borrowing affect credit history?

Yes. Responsible repayments generally strengthen your credit profile, while missed or delayed payments can negatively affect future borrowing opportunities.

How can I reduce borrowing costs?

Borrow only what you need, compare the total repayment cost, understand all charges, make repayments on time, and avoid extending debt longer than necessary.

UPI Credit Line Vs Personal Loan: Ultimate 2026-Final Takeaway

The debate around UPI Credit Line Vs Personal Loan does not have one universal winner because every borrower has different financial goals, income patterns, and repayment abilities. A flexible credit line may suit someone managing changing expenses, while a structured Personal Loan may work better for planned investments or major purchases. The smartest approach is not to ask which product is better but which product is better for your specific situation.

I have seen that successful borrowers rarely make decisions based on speed alone. Instead, they compare repayment flexibility, overall borrowing cost, financial discipline, and long-term affordability. Taking a little extra time to evaluate these factors often leads to better financial outcomes and greater peace of mind.

Borrow responsibly, read every agreement carefully, and remember that credit should support your financial progress—not become a burden. When used wisely, both options can be valuable tools within a well-planned personal finance strategy.

UPI Credit Line Vs Personal Loan: Ultimate 2026 Key Takeaways

- Understand your borrowing purpose before applying.

- Compare total repayment cost, not only interest rates.

- Read all terms, fees, and repayment conditions.

- Borrow only what you genuinely need.

- Repay on time to maintain a strong credit profile.

- Review your budget before taking on any financial commitment.

- Choose the option that aligns with your cash flow and long-term financial goals.

Conclusion

UPI Credit Line Vs Personal Loan Which Is Cheaper does not have one universal answer because both financial products serve different purposes. The smartest choice depends on your borrowing amount, repayment timeline, spending habits, and financial discipline.

UPI Credit Line works extremely well for short-term urgent expenses where flexibility and instant access matter most. Since interest applies only to the utilized amount, disciplined borrowers can save significant money by repaying quickly.

On the other hand, personal loans remain a stronger option for larger planned expenses requiring structured repayment and predictable EMIs. Lower long-term interest rates, fixed repayment schedules, and financial stability make personal loans more comfortable for many salaried borrowers.

The biggest mistake people make is choosing loans emotionally instead of strategically. Easy access to digital credit should never replace financial planning. Borrowing should support financial stability, not create unnecessary debt pressure. Therefore, always analyze repayment capacity honestly before taking any loan.

In 2026, digital lending will continue growing rapidly across India. However, financial awareness will become even more important because convenience can easily turn into costly debt when used irresponsibly. Smart borrowers compare total cost, repayment flexibility, hidden charges, and long-term financial impact before making decisions.

UPI Credit Line Vs Personal Loan: Ultimate 2026-If you use credit wisely, both UPI Credit Line and personal loans can become powerful financial tools. But if borrowing habits become careless, even small loans can create major stress later. Therefore, choose carefully, borrow responsibly, and always prioritize financial discipline over instant convenience.