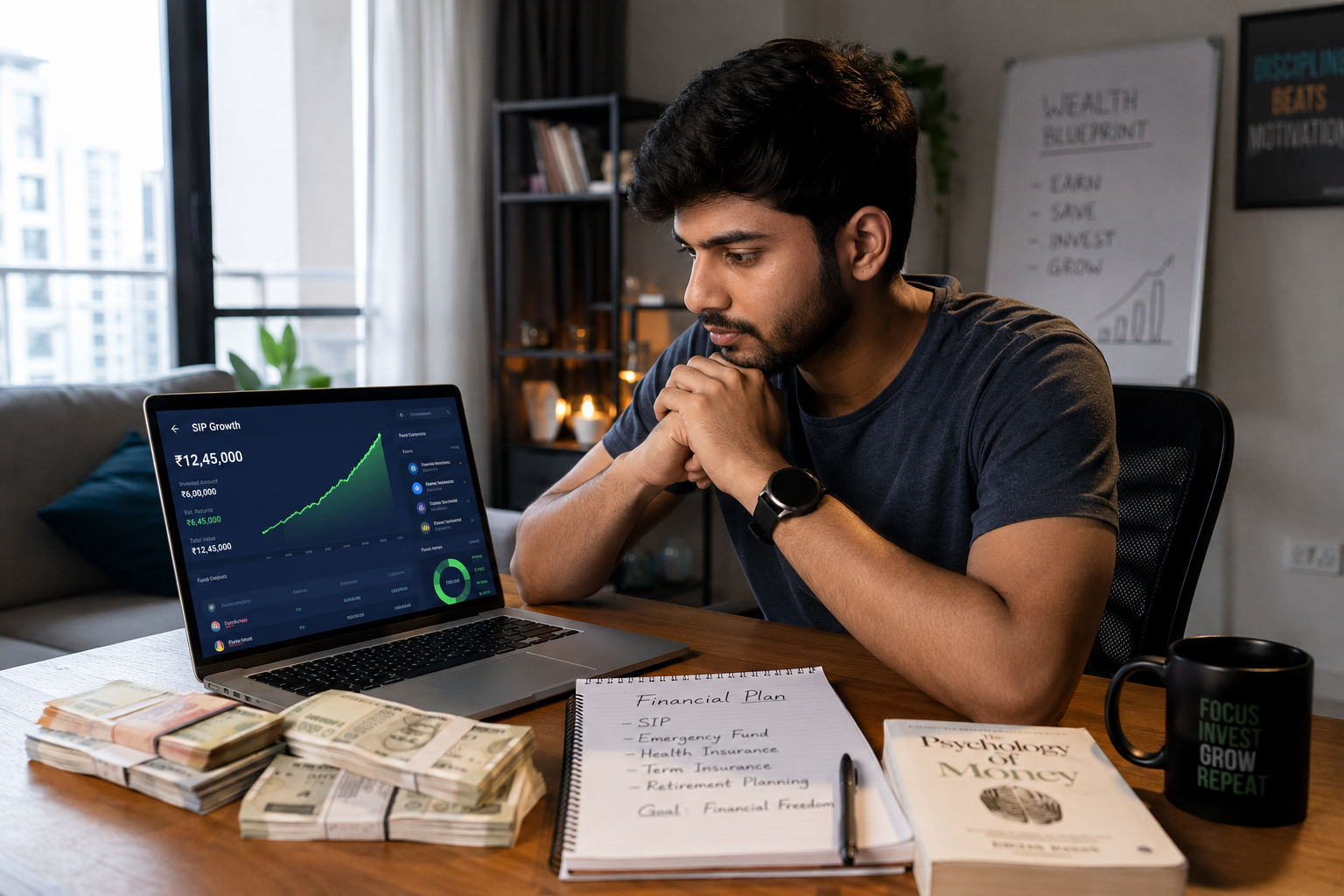

Best Investment Mistakes 2026 Proven Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22 is not just a shocking statement anymore. It has become a painful reality for millions of young Indians who entered their late 30s and 40s without proper savings, investments, or financial discipline. Most people believe investing can wait until salary increases, promotions happen, or responsibilities reduce. Unfortunately, money does not work that way. Time matters more than income when it comes to wealth creation. A person investing ₹5,000 monthly at age 22 often builds more wealth than someone investing ₹15,000 monthly at age 35.

That single difference creates regret, stress, and financial pressure later in life. Many Indians today openly admit they ignored investing because they thought they were too young, too broke, or too busy enjoying life. However, inflation, rising living costs, expensive healthcare, and unstable job markets changed everything. Suddenly, the people who delayed investing realized they lost their most powerful financial weapon: compounding. This is exactly why Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22 has become one of the most discussed personal finance topics in India today.

Table of Contents

Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22 In 2026

The biggest reason behind Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22 is the lack of financial awareness during early adulthood. Most schools and colleges in India still do not teach real-life money management. Students graduate knowing mathematics and science but have no idea how SIPs, mutual funds, stocks, or retirement planning work. As a result, young earners focus entirely on spending instead of investing. They buy expensive phones, bikes, subscriptions, and lifestyle upgrades before understanding the value of building assets. Initially, this lifestyle feels exciting.

Social media also adds pressure because everyone wants to look successful instantly. However, financial reality appears much later. By age 30 or 35, responsibilities increase rapidly. Marriage, children, home loans, healthcare expenses, and family obligations start consuming income. At that stage, people realize they should have started earlier. Unfortunately, compounding works best with time, not panic investing. Therefore, people who begin investing late need to invest much larger amounts to achieve the same financial goals. This painful realization is the core reason Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22 keeps becoming more relevant every year.

The Hidden Power Of Starting Investments At Age 22

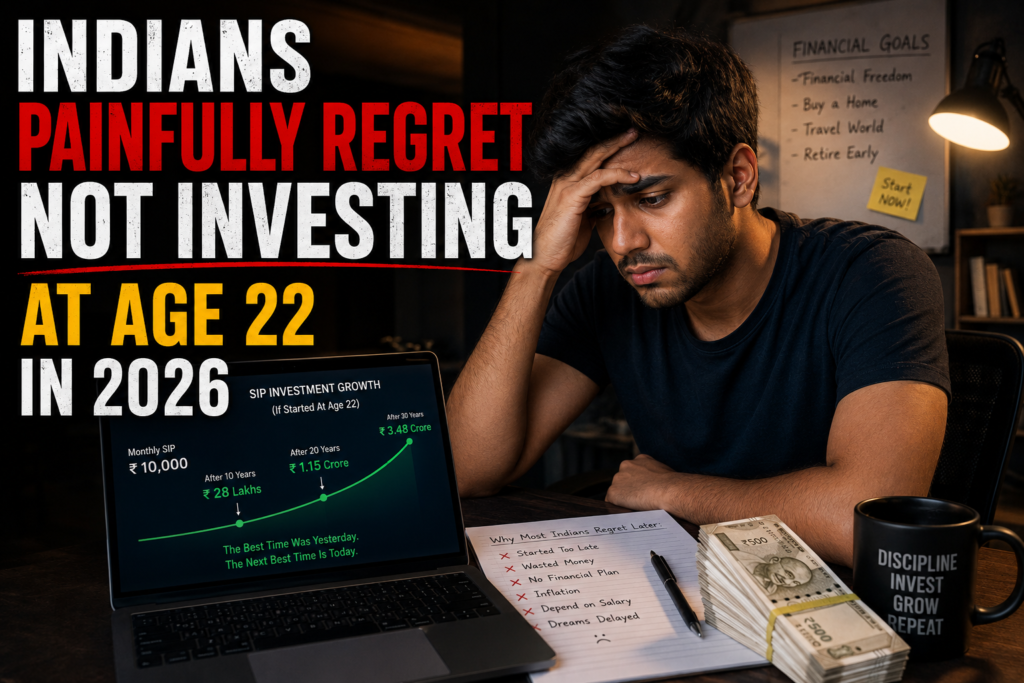

Most Indians underestimate the unbelievable power of early investing. Compounding may sound like a boring finance term, but it is actually the biggest wealth-building machine in the world. When someone starts investing at age 22, even small investments get enough time to grow exponentially. For example, if a person invests ₹5,000 monthly from age 22 with an average 12% annual return, the investment can potentially grow into crores over several decades. However, if the same person starts at age 32, the final wealth amount may reduce dramatically despite investing more money every month.

This is the hidden truth behind Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22. They do not regret only losing money. They regret losing time. Time cannot be recovered later. Additionally, early investing builds financial confidence. Young investors learn patience, risk management, market behavior, and disciplined savings habits. These habits eventually create financial stability. On the other hand, people who delay investing often live paycheck to paycheck even with higher salaries because they never developed healthy financial habits during their early earning years.

Best Investment Mistakes 2026 Proven-How Lifestyle Inflation Destroys Wealth Creation

Best Investment Mistakes 2026 Proven Another major reason Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22 is lifestyle inflation. This happens when income increases but expenses increase even faster. Many young professionals believe they will start investing once their salary becomes higher. However, each salary hike usually comes with new expenses. A better phone becomes necessary. Then a better apartment, expensive vacations, premium memberships, and luxury purchases follow.

Slowly, spending habits expand permanently. As a result, investing keeps getting delayed every year. This cycle becomes dangerous because the person feels financially successful externally while remaining financially weak internally. Best Investment Mistakes 2026 Proven-Social media worsens this problem significantly. Young Indians constantly compare themselves with influencers and friends who display luxury lifestyles online. Consequently, people start spending to impress others instead of investing for their future.

Unfortunately, financial stress eventually catches up. At age 40, many professionals earn good salaries but have minimal savings, heavy EMIs, and no retirement security. This financial insecurity becomes emotionally painful. Therefore, Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22 is directly connected to uncontrolled lifestyle inflation and poor financial priorities.

Best Investment Mistakes 2026 Proven-Why Compounding Rewards Young Investors More

Best Investment Mistakes 2026 Proven-Albert Einstein reportedly called compounding the eighth wonder of the world for a reason. Compounding allows money to generate returns, and then those returns generate even more returns over time. This creates a snowball effect. The earlier the investment starts, the bigger the snowball becomes. Understanding compounding explains perfectly Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22. Imagine two friends. One starts investing ₹3,000 monthly at age 22 and stops at age 32.

The second friend starts investing ₹3,000 monthly at age 32 and continues until age 60. Surprisingly, the first friend may still end up with similar or even greater wealth because the investments got more time to compound. That is how powerful time becomes in investing. Sadly, most people only realize this after crossing their 30s. By then, financial pressure increases, making consistent investing emotionally difficult. Early investing also reduces stress because investors can take calculated risks while they are young. Younger investors have more recovery time during market corrections. Older investors often panic because they are closer to retirement goals.

Best Investment Mistakes 2026 Proven-Common Excuses Indians Use To Avoid Investing

Best Investment Mistakes 2026 Proven-One of the most interesting aspects of Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22 is how similar the excuses are across different income groups. Some people say they earn too little. Others believe investing is risky. Many think they need expert knowledge before starting. Some wait for the “perfect time” in the market. However, these excuses usually hide deeper financial fears and lack of confidence. The truth is simple. Investing does not require huge income initially.

Even ₹500 SIPs can build excellent habits and meaningful long-term wealth. Waiting for perfect conditions usually means never starting at all. Markets will always fluctuate. Economic uncertainty will always exist. Therefore, successful investors focus on consistency instead of timing. Another common excuse involves family pressure. Many Indian families still prioritize fixed deposits and savings accounts because they fear stock market volatility. While safety matters, avoiding growth assets completely can destroy purchasing power over time because inflation keeps increasing. This creates another reason Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22 later in life when savings fail to match rising expenses.

Best Investment Mistakes 2026 Proven-How Inflation Quietly Eats Your Future Wealth

Best Investment Mistakes 2026 Proven-Inflation is one of the most dangerous financial realities that young Indians ignore. Prices of education, healthcare, real estate, and daily necessities keep rising continuously. Money sitting idle in savings accounts loses purchasing power every year. This is another major factor behind Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22. People think saving cash alone is enough, but inflation silently reduces its value. For example, ₹100 today may only buy goods worth ₹40 or ₹50 after many years due to inflation. Therefore, investing becomes essential, not optional. Investments help money grow faster than inflation.

Equity mutual funds, stocks, and long-term investment assets historically outperform inflation over long periods. Young investors especially benefit because they have time to ride market cycles. However, people who delay investing often struggle to beat inflation later because they become too conservative with money. Fear increases with age. Consequently, delayed investors miss both growth opportunities and compounding benefits simultaneously. This double loss creates deep financial regret during middle age.

Best Investment Mistakes 2026 Proven-The Emotional Side Of Financial Regret

Best Investment Mistakes 2026 Proven=Financial regret is not only about money. It also affects mental peace, confidence, relationships, and future choices. Many Indians in their late 30s openly admit they feel trapped because they started investing too late. This emotional reality strongly supports Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22. Delayed investing creates constant pressure. People start worrying about retirement, children’s education, emergencies, and healthcare costs. Additionally, they feel guilty watching younger investors become financially independent earlier.

Social comparison becomes emotionally exhausting. Some people even stay stuck in stressful jobs because they lack financial security. On the other hand, early investors often enjoy greater freedom. They can switch careers, start businesses, travel more confidently, or retire early because their investments support them. Money itself does not guarantee happiness, but financial stability definitely reduces stress. That is why investing early creates psychological benefits alongside wealth creation. The emotional pain of realizing “I should have started at 22” becomes one of the biggest financial regrets many Indians experience.

Best Investment Mistakes 2026 Proven-How SIP Investments Changed Financial Planning In India

Best Investment Mistakes 2026 Proven-Systematic Investment Plans transformed investing culture in India dramatically. Earlier, investing seemed complicated and accessible only to wealthy people. Today, SIPs allow ordinary salaried individuals to invest small amounts consistently every month. This accessibility directly addresses Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22 because now there are fewer excuses for delaying investments. Young professionals can start with minimal amounts and gradually increase contributions as income grows. SIPs also reduce emotional investing mistakes because investments continue automatically regardless of market conditions. This disciplined approach helps build long-term wealth efficiently.

Additionally, SIPs encourage habit formation. Once investing becomes a monthly routine, financial discipline improves naturally. However, despite these advantages, many young Indians still postpone starting. Some believe small investments are meaningless. Others prioritize short-term enjoyment over long-term security. Unfortunately, even a few years of delay can create massive differences in final wealth outcomes due to compounding. Therefore, financial experts continuously emphasize starting early instead of waiting for higher salaries or perfect market conditions.

Best Investment Mistakes 2026 Proven-Real Example Of Early Investing Vs Late Investing

Consider a realistic example that explains Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22 clearly. Rahul started investing ₹4,000 monthly at age 22 in equity mutual funds. His friend Aman started investing ₹10,000 monthly at age 32 because he wanted to “enjoy life first.” Assuming average long-term market returns, Rahul eventually accumulated more wealth despite investing significantly less money overall. Why? Because Rahul gave compounding an extra decade to work. Those early years became financially priceless.

Aman later realized he needed to invest aggressively just to catch up. This situation happens across India daily. Young earners underestimate how quickly time passes. They assume future income will solve all financial problems. However, financial goals also become larger with time. Marriage expenses, children’s education, home purchases, and medical costs increase continuously. Consequently, delayed investors feel permanently behind. This is exactly why Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22 resonates emotionally with millions of working professionals today.

Best Investment Mistakes 2026 Proven-Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22 And The Cost Of Waiting Too Long

The financial cost of delaying investments is much bigger than most people imagine. Many Indians think missing a few years of investing will not matter much. However, those missing years can reduce long-term wealth dramatically. This is another painful reason Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22 later in life. A person who delays investing by even five years may need to invest double the amount later just to achieve the same retirement goal. Unfortunately, by the time most people understand this reality,

they already have financial responsibilities. They cannot invest aggressively because monthly expenses consume most of their salaries. Therefore, the regret becomes emotional as well as financial. Many professionals say they wish someone had explained investing properly when they got their first salary. Instead of learning about assets and compounding, they focused entirely on consumption. They upgraded lifestyles faster than their financial intelligence. This pattern is visible across urban India today. Expensive gadgets, luxury experiences, and social media validation replaced long-term wealth planning. Consequently, Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22 continues becoming more relatable every year.

Best Investment Mistakes 2026 Proven-Why Young Indians Ignore Financial Planning

One major reason behind Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22 is psychological distance from the future. At age 22, retirement feels extremely far away. Medical emergencies seem unlikely. Financial pressure appears manageable. Young adults naturally focus more on present enjoyment than future security. This behavior is completely understandable, but it becomes financially dangerous when investing gets ignored for too long. Additionally, many first-job earners experience freedom for the first time. They suddenly have salaries, independence, and spending power.

Therefore, investing rarely becomes the first priority. Friends influence spending habits heavily during this stage. Weekend outings, gadgets, vacations, fashion, and online shopping dominate financial decisions. Unfortunately, nobody notices the hidden opportunity cost immediately. Years later, however, reality changes completely. People realize the money they spent casually could have grown into substantial wealth through compounding. That realization creates regret. Moreover, financial anxiety increases because delayed investors feel they are running out of time. This emotional pressure explains deeply Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22 after entering their mid-30s and 40s.

Best Investment Mistakes 2026 Proven-How Social Media Creates Financial Confusion

Social media plays a surprisingly powerful role in Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22. Young Indians constantly consume content promoting luxury lifestyles, instant success, and expensive consumption habits. Influencers rarely show the importance of disciplined investing, emergency funds, or retirement planning. Instead, flashy purchases receive more attention online. Consequently, many young professionals confuse spending with success. They feel pressure to appear rich before actually becoming financially stable.

This mindset damages long-term wealth creation. People start spending future wealth on present validation. Credit cards, EMIs, and buy-now-pay-later schemes make overspending even easier. Unfortunately, financial reality cannot be hidden forever. Eventually, responsibilities increase and people realize they built a lifestyle without building assets. This imbalance creates enormous stress later. Therefore, Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22 is also connected to the modern culture of comparison and instant gratification. Financial maturity often arrives much later than financial independence, and that gap creates regret.

Best Investment Mistakes 2026 Proven-Why Investing Early Builds Confidence And Discipline

Early investing does not only create wealth. It also develops confidence, patience, and discipline. This is another overlooked reason Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22. Young investors learn how markets behave during ups and downs. They understand risk gradually instead of fearing it completely. They also develop better money habits because investing forces people to think long term. A person who invests regularly becomes more conscious about unnecessary spending. Financial awareness improves naturally over time. Additionally, early investors often feel more secure during emergencies because they already have savings and assets growing steadily.

On the other hand, people who delay investing frequently experience financial instability despite earning decent salaries. They struggle to save consistently because investing habits were never developed. Consequently, even small market fluctuations create fear and confusion. Starting early also reduces pressure later. A young investor can build wealth slowly and steadily without taking extreme financial risks. Delayed investors often attempt aggressive investing later because they want faster results. Unfortunately, emotional investing usually creates more losses than profits.

Best Investment Mistakes 2026 Proven-The Dangerous Myth Of “I Will Start Next Year”

The sentence “I will start investing next year” has destroyed wealth for millions of people. This mindset directly explains Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22. Delaying financial action becomes a habit very quickly. One year becomes three years, then five years, and eventually a decade disappears. People always find reasons to postpone investing. Sometimes the market looks risky. Sometimes income feels insufficient. Sometimes expenses seem more important.

However, waiting rarely improves financial discipline. In fact, delaying investing often makes starting emotionally harder because the person feels guilty about lost time. Therefore, they continue postponing action even further. Successful investors understand that starting imperfectly is better than waiting endlessly. Even small investments create momentum and financial awareness. The hardest part is usually beginning, not continuing. Once investing becomes routine, consistency improves naturally. This simple truth explains why financial experts repeatedly encourage young earners to start immediately rather than waiting for ideal conditions.

Best Investment Mistakes 2026 Proven-Why Emergency Funds And Investments Must Work Together

Many Indians believe they must choose between saving money and investing money. However, both are essential for financial stability. Understanding this balance also helps explain Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22. An emergency fund provides short-term security, while investments create long-term wealth. Without emergency savings, people may panic during financial crises and withdraw investments early. Without investments, savings alone may fail to beat inflation.

Therefore, young adults should ideally build both gradually. A practical strategy involves creating a small emergency fund first and then starting SIP investments simultaneously. This balanced approach reduces financial anxiety while allowing wealth creation to begin early. Unfortunately, many people spend years accumulating cash savings without learning about investment growth. As inflation increases, they realize their money did not grow meaningfully. This realization becomes another source of regret later in life.

Best Investment Mistakes 2026 Proven-The Relationship Between Financial Freedom And Early Investing

Financial freedom means having enough investments and assets to support your lifestyle without constant financial stress. Most people dream about financial freedom but underestimate the role of early investing in achieving it. This connection explains Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22. Financial freedom is not built suddenly. It develops gradually through years of disciplined investing, smart financial choices, and patience. People who begin early gain flexibility later.

They can take career breaks, explore entrepreneurship, relocate, or retire earlier because investments support their decisions. In contrast, delayed investors often feel trapped in stressful jobs because they depend entirely on salaries. They may earn more money, but financial pressure remains high due to insufficient assets. Therefore, investing early creates freedom of choice, not just financial returns. This emotional and practical advantage becomes extremely clear during middle age, when responsibilities increase significantly.

Best Investment Mistakes 2026 Proven-Why Mutual Funds Became Popular Among Young Indians

Mutual funds became popular because they simplified investing for ordinary people. This trend strongly connects with Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22. Earlier generations often avoided equity investing because they lacked access, knowledge, or confidence. Today, technology and mobile apps made investing much easier. Young Indians can start SIPs within minutes. Educational content about investing is also more available now than ever before.

Despite these advantages, hesitation still exists because many people fear losses or misunderstand market volatility. However, long-term investing historically rewards patience. Equity mutual funds especially work well for young investors because they provide diversification and professional management. Additionally, SIP investing removes the pressure of timing the market perfectly. Regular investing during both rising and falling markets helps average investment costs over time. Consequently, disciplined investors benefit from long-term market growth without needing advanced expertise.

Best Investment Mistakes 2026 Proven-Mistakes Young Investors Must Avoid

Understanding common investing mistakes is important because avoiding them can save years of regret. Many of these mistakes directly contribute to Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22. The first mistake is delaying investments unnecessarily. The second mistake is chasing quick profits instead of focusing on long-term growth. Many beginners enter markets hoping for instant returns, then panic during corrections. Emotional investing usually creates poor decisions.

Another mistake involves investing without financial goals. Goals provide direction and motivation. Young investors should define why they are investing, whether for retirement, financial freedom, travel, education, or family security. Additionally, many people ignore diversification and invest randomly based on social media trends. Proper financial planning requires patience and balance. Overspending is another dangerous mistake because it reduces investment capacity significantly. Building wealth requires controlling unnecessary expenses consistently over time.

Best Investment Mistakes 2026 Proven-How Parents Can Teach Financial Literacy Earlier

Financial education should ideally begin before adulthood. Parents play a critical role in shaping money habits. This topic also connects deeply with Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22. Many Indian families avoid discussing money openly with children. As a result, young adults enter working life without understanding investments, taxes, budgeting, or inflation. Teaching financial literacy earlier can change future outcomes dramatically. Parents can encourage savings habits, explain compounding, and introduce basic investing concepts during teenage years.

Even simple conversations about budgeting and goal setting create awareness. Financial literacy empowers young people to make smarter decisions when they start earning. Moreover, it reduces fear around investing because familiarity builds confidence. Countries with stronger financial education systems often produce better long-term saving habits among young adults. India is gradually improving in this area, but awareness still needs significant growth.

Best Investment Mistakes 2026 Proven-The Reality Of Retirement Planning In India

Retirement planning is becoming increasingly important because traditional family support systems are changing rapidly. Earlier generations often depended on children during old age. Today, rising living costs and modern lifestyles make independent retirement planning essential. This reality strongly supports Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22. Young earners who ignore retirement planning usually assume they have plenty of time. Unfortunately, retirement wealth requires decades of preparation.

Waiting until age 40 to think seriously about retirement creates massive pressure because investment amounts need to become much larger. Healthcare inflation further complicates the situation. Medical expenses during old age can become financially devastating without proper planning. Therefore, early investing becomes one of the most practical forms of self-protection for the future. Retirement planning is not only about old age comfort. It is about maintaining dignity, independence, and peace of mind throughout life.

Best Investment Mistakes 2026 Proven-Case Study Of Two Different Financial Journeys

Consider another realistic example that explains Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22. Priya started investing ₹2,500 monthly immediately after getting her first job at age 22. Initially, the amount looked small, but she stayed consistent. Over time, she increased investments whenever her salary increased. By age 35, she already had significant investments, emergency savings, and financial confidence. Meanwhile, her colleague Neha delayed investing because she wanted to enjoy life first.

She traveled frequently, upgraded gadgets regularly, and postponed financial planning repeatedly. At age 35, Neha earned more salary than Priya but had very limited savings. She felt stressed about future security and regretted not starting earlier. This example reflects real financial journeys across India today. The difference rarely comes from intelligence or income alone. Usually, it comes from starting early and remaining disciplined consistently.

Best Investment Mistakes 2026 Proven-Pro Tips That Most Financial Experts Do Not Explain Clearly

One important lesson behind Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22 is that consistency matters more than perfection. Many beginners waste years trying to learn every investment detail before starting. However, investing is often learned best through practical experience. Another important tip involves increasing investments gradually with salary growth. Instead of increasing lifestyle expenses after every promotion, increasing SIP amounts can transform long-term wealth dramatically.

Additionally, automating investments reduces emotional decision-making. Automatic SIP deductions create discipline effortlessly. Another underrated strategy involves avoiding unnecessary debt during young adulthood. High-interest debt destroys investment growth because money goes toward interest payments instead of asset creation. Finally, patience remains one of the most powerful investing skills. Wealth creation usually looks slow initially, but compounding accelerates growth significantly over time.

The most powerful lesson behind Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22 is that financial success usually depends on behavior more than intelligence. Many highly educated professionals still struggle financially because they never built investing habits early in life. On the other hand, ordinary salaried individuals who started small SIPs at age 22 often achieve strong financial stability by their late 30s. This difference surprises many people because society usually associates wealth only with high salaries. However, investing discipline creates a much bigger long-term impact than income alone.

A person earning ₹40,000 monthly and investing consistently may eventually build greater wealth than someone earning ₹1 lakh monthly but spending everything. Unfortunately, this truth becomes obvious only after many years. That delayed realization explains perfectly Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22. They discover too late that income without investing rarely creates lasting financial freedom. Instead, disciplined investing combined with controlled expenses builds real wealth over time.

How Small Monthly Investments Become Life-Changing Wealth

Many young Indians underestimate small investments because immediate growth looks slow. However, long-term investing works differently from quick-profit thinking. This understanding is essential to fully grasp Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22. Small investments may appear insignificant initially, but consistency changes everything. For example, investing ₹100 daily may not feel impressive today. Yet over decades, those investments can grow into a substantial corpus through compounding and market growth. The problem is that humans naturally focus on short-term results.

People want immediate rewards, quick transformations, and visible success. Investing rewards patience instead. This psychological challenge causes many young earners to delay financial planning. They think investing will become meaningful only after higher salaries arrive. Unfortunately, by delaying action, they sacrifice the most important factor in investing: time. Even modest investments started early often outperform large investments started late. This reality becomes emotionally painful for delayed investors once they finally calculate how much wealth they could have created earlier.

Best Investment Mistakes 2026 Proven-How To Avoid Becoming One Of Them ans Financial Discipline Matters More Than Motivation

Motivation feels powerful temporarily, but discipline creates permanent results. This principle strongly connects with Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22. Many people become excited about investing after watching videos or reading success stories. However, excitement alone does not build wealth. Consistent monthly investing builds wealth. Financial discipline means continuing investments even during market corrections, economic uncertainty, or temporary personal struggles.

Unfortunately, many beginners invest emotionally. They invest aggressively during market rallies and panic during declines. As a result, they buy high and sell low repeatedly. Early investors who remain disciplined usually perform much better over time because they allow compounding to work uninterrupted. Discipline also helps control unnecessary spending. Every unnecessary expense carries an opportunity cost because that money could have become a future investment. Understanding opportunity cost changes financial behavior dramatically. Young adults who recognize this concept earlier often make smarter financial decisions throughout life.

Best Investment Mistakes 2026 Proven-The Role Of Financial Awareness In Wealth Creation

Financial awareness is one of the biggest advantages a young person can develop today. Understanding inflation, investing, taxes, budgeting, and compounding creates a massive long-term edge. Lack of this awareness directly contributes to Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22. Many people work hard for money but never learn how money itself works. Consequently, they remain financially dependent on active income for decades. Financial awareness changes this mindset completely.

Instead of spending every salary increase, financially aware individuals focus on building assets that generate future value. They understand the importance of emergency funds, investment diversification, and long-term planning. Additionally, financially educated people usually avoid common traps like excessive debt, emotional investing, and lifestyle inflation. This knowledge creates confidence because decisions become intentional rather than reactive. Young adults who prioritize financial learning early often experience less stress later because they understand how to manage uncertainty better.

Best Investment Mistakes 2026 Proven-Why Delayed Investing Creates Retirement Fear

Retirement fear is becoming increasingly common among working professionals in India. Rising healthcare costs, unstable job markets, and inflation make future security a serious concern. This reality strongly supports Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22. Many people reach their late 30s or 40s and suddenly realize retirement is no longer a distant concept. Unfortunately, building retirement wealth requires decades of investing. Starting late creates enormous pressure because monthly investment requirements become much larger. Some people attempt risky shortcuts hoping to recover lost time quickly.

However, aggressive investing without proper planning often increases financial stress instead of reducing it. Early investors usually avoid this panic because they gave their investments enough time to grow gradually. Retirement planning becomes easier when started early because compounding handles much of the heavy work over decades. Therefore, investing early is not only about becoming rich. It is about reducing future fear and increasing long-term peace of mind.

Best Investment Mistakes 2026 Proven-Why Budgeting And Investing Must Work Together

Budgeting and investing are often treated as separate financial topics, but they are deeply connected. Understanding this relationship also helps explain Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22. Without budgeting, investing becomes inconsistent because spending controls financial decisions completely. A proper budget creates clarity about where money goes every month. This awareness helps identify unnecessary expenses that can be redirected toward investments. Young earners especially benefit from simple budgeting systems because habits formed early usually continue for years.

Budgeting does not mean avoiding enjoyment completely. Instead, it means spending intentionally while still prioritizing future goals. Many financially successful people live balanced lives because they control spending instead of allowing spending habits to control them. Investing works best when it becomes a planned monthly priority rather than an occasional leftover activity. Automatic SIP deductions combined with realistic budgeting create excellent long-term financial discipline.

Best Investment Mistakes 2026 Proven-The Difference Between Saving And Investing

Many Indians still confuse saving with investing. Although both are important, they serve different financial purposes. This misunderstanding contributes significantly to Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22. Saving protects money for short-term needs and emergencies. Investing grows money for long-term goals and wealth creation. Keeping all money in low-return savings accounts may feel safe initially, but inflation gradually reduces purchasing power.

Therefore, investments become essential for long-term financial growth. Young adults especially need investments because they have enough time to handle market fluctuations. Long investment horizons reduce the impact of short-term volatility substantially. However, many people avoid investing completely because they fear temporary losses. Unfortunately, avoiding growth assets entirely often creates bigger long-term financial risks. A balanced financial strategy includes both emergency savings and long-term investments working together.

Best Investment Mistakes 2026 Proven-Why Consistency Beats Perfection In Investing

One of the biggest myths about investing is that people need perfect timing or expert knowledge to succeed. In reality, consistency usually matters far more than perfection. This lesson sits at the center of Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22. Many young earners delay investing because they feel unprepared. They believe they must understand every market detail before starting.

However, waiting for complete certainty often results in years of inaction. Successful long-term investors usually focus on regular investing instead of predicting market movements constantly. They understand that markets naturally fluctuate, but disciplined investing across decades historically creates strong results. This mindset reduces emotional stress significantly. Instead of worrying about daily market movements, consistent investors focus on long-term financial goals. Starting imperfectly today often produces better results than waiting years for ideal conditions.

Best Investment Mistakes 2026 Proven-How Early Investing Creates Career Freedom

An underrated advantage of early investing is career flexibility. Financial security gives people more freedom to make professional decisions confidently. This benefit directly connects with Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22. Individuals with investments and savings often feel less trapped in toxic work environments because they have financial cushioning. They can take calculated career risks, pursue entrepreneurship, learn new skills, or switch industries more comfortably.

On the other hand, people living paycheck to paycheck frequently remain stuck in stressful situations because they cannot afford uncertainty. Investments create options. Even moderate financial security can improve mental peace significantly. Therefore, investing early is not only about retirement planning. It also improves present-day confidence and flexibility. This emotional advantage becomes increasingly valuable during unpredictable economic conditions and changing job markets.

Best Investment Mistakes 2026 Proven-How Inflation Changes Financial Reality Every Year

Inflation quietly changes financial reality every single year. Many young people fail to notice it because price increases happen gradually. However, over decades, inflation dramatically increases living costs. This economic reality explains another major reason Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22. Expenses that seem manageable today may become overwhelming later without investment growth. Education, healthcare, housing, and daily essentials continue becoming more expensive over time.

Salaries may increase, but inflation also keeps rising. Therefore, simply earning more money does not guarantee financial security. Investments help protect future purchasing power by growing wealth faster than inflation over long periods. Delayed investors often realize too late that traditional savings alone cannot support future financial needs effectively. Consequently, they experience increasing pressure to catch up financially during middle age.

Best Investment Mistakes 2026 Proven-Why Financial Independence Starts With One Decision

Financial independence usually begins with one simple decision: starting. This idea perfectly summarizes Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22. Most people do not fail financially because they lacked opportunities. They fail because they delayed action repeatedly. Starting small may feel insignificant initially, but momentum builds over time. Every investment creates progress.

Every SIP builds discipline. Every financial habit shapes future outcomes. Young adults often underestimate how quickly years pass. The future they imagine eventually becomes the present reality they must live with. Therefore, taking financial action early matters enormously. Investments started at age 22 may eventually support dreams, emergencies, family security, and retirement freedom decades later. That is the hidden power of beginning early.

Final Thoughts

Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22 is ultimately about missed opportunities, lost compounding years, and delayed financial awareness. The regret does not come from failing to predict markets perfectly. It comes from not starting at all. Financial success rarely happens overnight. It develops slowly through consistent investing,

disciplined habits, controlled spending, and long-term thinking. Young Indians today have more access to investing tools and financial education than ever before. Therefore, there has never been a better time to start building wealth intelligently. Even small investments made consistently can transform future financial security dramatically. The most important step is not finding the perfect investment strategy. The most important step is beginning before more time disappears.

FAQ

What does Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22 actually mean?

It highlights the financial regret many Indians feel later in life after realizing they delayed investing during their early earning years and lost valuable compounding time.

Why is age 22 considered important for investing?

Age 22 is important because investments started early get more years to compound and grow, creating much larger long-term wealth.

Can small SIP investments really create wealth?

Yes. Even small SIP investments can grow significantly over decades due to compounding and disciplined investing habits.

Is investing risky for beginners?

Every investment has some risk, but long-term diversified investing through mutual funds generally reduces risk substantially compared to short-term speculation.

What is the biggest investing mistake young Indians make?

The biggest mistake is delaying investing while focusing entirely on spending and lifestyle upgrades.

Conclusion

Why 6 Out Of 10 Indians Painfully Regret Not Investing At Age 22 is ultimately a warning about time, discipline, and financial awareness. Most people do not regret spending less money on luxury purchases. They regret losing years that could have transformed their future through investing and compounding. Financial freedom rarely depends only on salary size. It depends more on habits, consistency, and starting early.

The earlier someone begins investing, the less pressure they usually face later in life. Young Indians today have more investing opportunities, educational resources, and digital tools than any previous generation. Therefore, delaying action has become even more costly. Starting with small investments today is far better than waiting for perfect conditions tomorrow. Every year matters in wealth creation. Every SIP matters. Every financial habit matters. The future version of you will either thank you for starting early or regret waiting too long.

2 thoughts on “Best Investment Mistakes 2026 Proven”