Bad Financial Decision At 25- is not just a catchy headline. It is a financial reality that many people discover only after years have passed. At the age of 25, most people are focused on enjoying their first salary, upgrading their lifestyle, buying gadgets, traveling, or simply living independently. Very few think about how one financial choice today can affect their future wealth by lakhs of rupees.

I have seen this happen many times. A person earning a decent salary feels that investing can wait. Another person delays saving because they believe they will earn more later. Some take unnecessary loans because monthly EMIs seem affordable. These decisions may appear small today, but over the next 10 or 20 years they can create a huge financial gap.

The truth is simple. Time is the most valuable asset in wealth creation. Money lost today is not just money lost. It is also the future growth that money could have generated. That is why understanding Why 1 Bad Financial Decision At 25 Can Cost You 40 Lakh Later is essential for anyone who wants long-term financial security.

Table of Contents

The Hidden Cost of Delaying Financial Decisions

Most people think financial mistakes are dramatic events such as losing money in a scam or making a bad stock investment. However, the biggest financial mistakes are often invisible.

One of the most common examples is delaying investments.

Imagine two friends. One starts investing ₹5,000 every month at age 25. The other waits until age 35 to begin. Assuming similar returns, the first person may accumulate tens of lakhs more by retirement.

The difference is not because the first person invested significantly more money. The difference comes from time and compounding.

I remember reading several studies showing that investors who start earlier often contribute less money overall but end up with larger portfolios. This is the power of compounding working quietly in the background.

Therefore, when discussing Why 1 Bad Financial Decision At 25 Can Cost You 40 Lakh Later, delaying investments deserves a place at the top of list.

Why Lifestyle Inflation Destroys Wealth

Lifestyle inflation happens when spending increases every time income increases.

A salary hike arrives and immediately a bigger car becomes necessary. A promotion leads to expensive vacations. A bonus disappears on luxury purchases.

There is nothing wrong with enjoying your income. The problem begins when every increase in earnings results in higher expenses and zero growth in savings.

Many people earning ₹1 lakh per month still struggle financially because expenses rise as quickly as income.

Financial experts often warn about lifestyle inflation because it quietly reduces wealth-building potential. Instead of investing additional income, people consume it.

Over twenty years, the opportunity cost can be enormous. The money spent on unnecessary upgrades could have become a significant investment portfolio.

This is another reason why Why 1 Bad Financial Decision At 25 Can Cost You 40 Lakh Later is more than a theoretical discussion. It reflects real-world behavior that affects millions of people.

The Dangerous Trap of Bad Debt

Not all debt is harmful. Some forms of debt can help achieve important goals.

However, high-interest consumer debt is different.

Why 1 Bad Financial Decision at 25 Costs ₹40 Credit card debt, personal loans for luxury purchases, and financing lifestyle expenses often create long-term financial problems.

Many young professionals underestimate how quickly interest accumulates.

A purchase that feels affordable today can become expensive when interest charges continue month after month.

I have personally heard financial advisors explain that high-interest debt acts like negative compounding. Instead of helping wealth grow, it steadily reduces net worth.

This is why avoiding unnecessary debt remains one of the smartest financial decisions anyone can make during their twenties.

Ignoring Emergency Funds

An emergency fund may not seem exciting.

There are no dramatic gains and no impressive returns.

However, it provides something equally valuable: financial stability.

Without an emergency fund, unexpected events such as medical expenses, job loss, or urgent repairs can force people to borrow money or sell investments at the wrong time.

A well-funded emergency reserve protects long-term financial plans.

Many individuals focus entirely on investing while ignoring liquidity. Later, a financial emergency disrupts years of progress.

That is why every strong financial plan begins with a solid emergency fund.

Bad Financial Decision At 25-Why Financial Education Matters More Than Income

One of the biggest misconceptions is that high income automatically leads to wealth.

Reality tells a different story.

Many high earners struggle financially while some moderate earners build impressive wealth.

The difference often comes down to financial knowledge.

Understanding budgeting, investing, taxation, risk management, and long-term planning creates better financial outcomes.

I have noticed that financially successful people consistently spend time learning about money. They read books, follow credible financial sources, and continue improving their knowledge.

Financial education helps prevent costly mistakes and improves decision-making.

Bad Financial Decision At 25-Small Decisions Create Massive Results

The biggest lesson from personal finance is that wealth is rarely created through one spectacular decision.

Instead, wealth grows through consistent small actions.

Saving regularly.

Investing consistently.

Avoiding unnecessary debt.

Controlling lifestyle inflation.

Building emergency reserves.

Improving financial knowledge.

Each action may seem insignificant in isolation. Together, they create powerful long-term results.

This is exactly why Why 1 Bad Financial Decision At 25 Can Cost You 40 Lakh Later deserves attention. Financial consequences often appear years after the original decision.

Bad Financial Decision At 25-Common Financial Mistakes Young Adults Make

Ignoring Investments

Many people postpone investing because retirement feels distant.

Spending Every Salary Increase

Higher income should increase investments, not just expenses.

Taking Unnecessary Loans

Luxury purchases financed through debt often create long-term burdens.

Not Tracking Expenses

Money leaks usually happen through small recurring expenses.

Following Social Pressure

Trying to match other people’s lifestyles can damage financial progress.

Pro Tips Most People Never Hear

Focus on Savings Rate

Increasing savings percentage often matters more than increasing returns.

Automate Investments

Automation removes emotional decision-making.

Review Finances Quarterly

Regular reviews help identify problems early.

Build Skills

Increasing earning potential remains one of the best long-term investments.

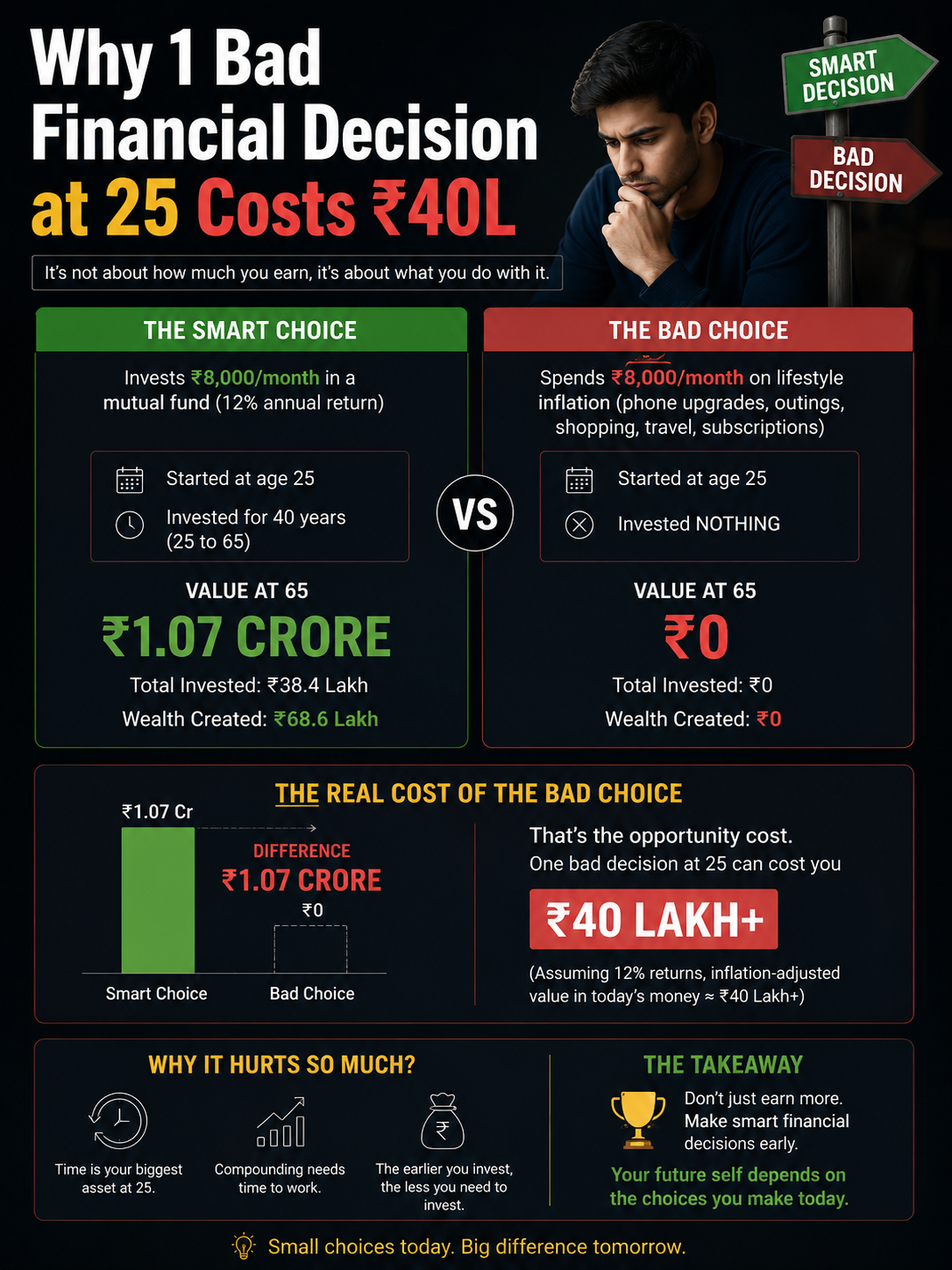

Bad Financial Decision At 25-How a ₹5,000 Monthly SIP Delay Can Become a ₹40 Lakh Mistake

Many people think missing one year of investing is not a big deal. After all, they can always start later when their salary increases. Unfortunately, wealth creation does not work that way.

Consider a simple example. A person starts a ₹5,000 monthly SIP at age 25 and continues investing consistently. Another person decides to wait until age 35 because they want to enjoy life first and invest later.

Both individuals may eventually invest similar amounts every month. However, the first investor gets something the second investor can never recover—an extra decade of compounding.

I have seen many financial planners highlight this exact issue. They often explain that the biggest advantage young investors have is not higher income. It is time.

Those ten years can create a wealth difference worth several lakhs or even crores depending on investment returns and consistency. This is one of the strongest examples of why one bad financial decision at 25 can cost you 40 lakh later.

The lesson is simple. Never underestimate the value of starting early. Even a small amount invested consistently can outperform large investments started much later.

Why Your First Salary Shapes Your Financial Future

Most people remember their first salary because it represents freedom. Suddenly, you can buy things without asking anyone. You can travel, shop, and enjoy experiences.

There is absolutely nothing wrong with enjoying your earnings. The problem starts when spending becomes the default habit and saving becomes an afterthought.

Financial habits formed during the first few years of employment often stay with people for decades.

Someone who learns to save 20% of income from the beginning usually continues doing so even when income increases. On the other hand, someone who spends everything they earn often struggles financially despite salary growth.

I have noticed that successful investors rarely begin with huge amounts. They begin with discipline.

They create a system where investing happens automatically every month. They treat investing like a mandatory expense rather than an optional activity.

This mindset shift may appear small today, but it creates a massive difference over the long term.

Bad Financial Decision At 25-The Opportunity Cost Nobody Talks About

One of the most overlooked financial concepts is opportunity cost.

Opportunity cost means what you give up when choosing one option over another.

For example, buying an expensive smartphone is not just about spending ₹80,000. The real cost includes the investment growth that ₹80,000 could have generated over the next twenty years.

This perspective changes everything.

Instead of asking whether you can afford something, you start asking whether the purchase is worth sacrificing future wealth.

Financially successful people often think in terms of opportunity cost. They understand that every spending decision has a hidden long-term consequence.

This does not mean never spending money. It simply means spending consciously.

Understanding opportunity cost is one of the fastest ways to improve financial decision-making.

Bad Financial Decision At 25-The Psychological Side of Money Mistakes

Money decisions are rarely logical.

Most financial mistakes happen because of emotions.

Fear causes people to avoid investing.

Greed encourages risky investments.

Social pressure pushes people into unnecessary spending.

Overconfidence leads to poor financial choices.

Many young professionals buy things they do not truly need simply because everyone around them is doing the same thing.

A new car, luxury gadgets, expensive vacations, and premium lifestyles often become status symbols.

However, financial success is not about looking wealthy. It is about becoming wealthy.

The difference between those two ideas is enormous.

I have heard many experts repeat the same principle: real wealth is often invisible.

Investment portfolios are invisible.

Emergency funds are invisible.

Retirement accounts are invisible.

But these invisible assets are what create genuine financial security.

Bad Financial Decision At 25-Why Financial Freedom Starts Before Age 30

Many people assume financial freedom is a goal for their forties or fifties.

In reality, the foundation is built much earlier.

The decisions made between ages 20 and 30 often determine financial outcomes decades later.

This period is important because:

- Income starts growing.

- Financial habits become permanent.

- Investment time horizon is longest.

- Risk-taking capacity is highest.

People who use these years wisely gain a tremendous advantage.

Even if income is modest, consistent investing combined with time creates powerful results.

That is why delaying good financial habits can be surprisingly expensive.

Bad Financial Decision At 25-A Realistic Example of a Costly Financial Mistake

Imagine two individuals earning the same salary.

Person A starts investing ₹8,000 monthly at age 25.

Person B decides to enjoy life and starts at age 35.

Both are intelligent. Both work hard. Both earn similar incomes.

The only difference is timing.

Twenty years later, Person A may have accumulated substantially more wealth because compounding had more time to work.

The gap often surprises people.

Most assume the difference will be small. Instead, it can easily reach several lakhs or more.

That is the hidden cost of waiting.

Warning Signs You Are Making a Bad Financial Decision

Sometimes financial mistakes are obvious. Other times they are hidden.

Watch for these warning signs:

- You regularly spend more than you save.

- Credit card balances keep increasing.

- You have no emergency fund.

- Investing is always postponed until next month.

- Lifestyle expenses rise after every salary increase.

- Financial goals are unclear.

- You depend entirely on one source of income.

If several of these signs sound familiar, it may be time to reassess your financial strategy.

How to Avoid the ₹40 Lakh Mistake

The solution is not complicated.

Start investing early.

Build an emergency fund.

Avoid unnecessary debt.

Increase investments whenever income rises.

Continue learning about personal finance.

Focus on long-term goals instead of short-term gratification.

Most importantly, remember that wealth creation is usually boring.

It comes from consistency rather than excitement.

Small monthly investments. Regular saving. Controlled spending. Continuous learning.

These habits may not look impressive on social media, but they create extraordinary results over time.

The Final Financial Reality

Most people spend years searching for the perfect investment, the next market opportunity, or a secret wealth-building strategy.

However, the biggest factor behind financial success is often much simpler.

It is avoiding major mistakes early in life.

One poor financial decision at 25 may not seem important today. But because money compounds over time, the consequences can grow much larger than expected.

That is why financial decisions deserve careful thought.

Every rupee has potential.

Every year matters.

Every financial habit counts.

And sometimes, avoiding one bad decision is worth more than making ten good ones.

Bad Financial Decision At 25-The Difference Between Rich Income and Rich Wealth

One of the biggest financial misconceptions is believing that a high salary automatically creates wealth.

I have personally seen people earning ₹40,000 per month build strong investment portfolios, while others earning ₹2 lakh per month struggle financially. The difference is rarely income. The difference is behavior.

Income helps create opportunities, but wealth comes from what you keep, invest, and grow.

Think about it this way. If someone earns ₹1 lakh every month but spends ₹95,000, their financial progress will remain slow. On the other hand, a person earning ₹60,000 and investing ₹15,000 every month may build greater long-term wealth.

This is why many financial experts focus more on savings rate than income level.

The people who become financially secure are usually not the biggest spenders. They are the people who consistently direct money toward assets instead of liabilities.

That is why one bad financial decision at 25 can cost you 40 lakh later. The wrong decision often prevents money from reaching investments where it could have grown for years.

Why Most Financial Regrets Begin with “I Will Start Later”

Almost every major financial regret starts with the same sentence.

“I will start later.”

I will start investing later.

I will buy insurance later.

I will create an emergency fund later.

I will learn about personal finance later.

The problem is that later often becomes years.

Before you realize it, five or ten years have passed.

I have read interviews from successful investors who repeatedly mention one common regret. Most wish they had started earlier.

Interestingly, very few regret starting too soon.

This teaches an important lesson. Imperfect action today is usually better than perfect action someday in the future.

Financial progress rewards consistency, not perfection.

Even if your first investment is small, the habit itself becomes valuable.

The habit eventually becomes a system.

And systems create wealth.

Bad Financial Decision At 25-The Power of Compounding Nobody Appreciates at 25

At age 25, retirement feels extremely far away.

Forty years sounds like a lifetime.

That is why many young adults underestimate compounding.

However, compounding becomes powerful precisely because it has time.

A small investment today can produce surprisingly large results decades later.

The challenge is that compounding feels slow at first.

During the first few years, growth appears minimal.

Many people become impatient and quit.

Then something interesting happens.

As years pass, growth starts accelerating.

The portfolio begins generating returns on previous returns.

This is when wealth starts growing rapidly.

Unfortunately, people who delayed investing miss this early foundation period.

That lost time can never be recovered completely.

Why Social Media Creates Expensive Financial Mistakes

Today’s generation faces a challenge that previous generations did not.

Constant exposure to other people’s lifestyles.

Every day people see luxury cars, expensive vacations, designer clothes, and seemingly perfect lives.

What social media rarely shows is debt, financial stress, or lack of savings.

This creates pressure.

People start comparing their financial reality with someone else’s highlight reel.

As a result, they spend money to impress others.

The irony is that many wealthy individuals focus more on building assets than displaying wealth.

I have often noticed that financially successful people prioritize investments, businesses, skills, and long-term growth over appearances.

Meanwhile, people chasing appearances often sacrifice financial security.

One bad financial decision at 25 can cost you 40 lakh later because short-term status frequently destroys long-term wealth creation.

Bad Financial Decision At 25-Building Wealth Is More About Habits Than Intelligence

Many people believe financial success requires exceptional intelligence.

The truth is much simpler.

Personal finance is largely behavioral.

The basic principles are not complicated:

Spend less than you earn.

Invest consistently.

Avoid unnecessary debt.

Think long term.

Bad Financial Decision At 25 Keep learning.

The challenge is not understanding these ideas.

The challenge is applying them consistently.

I have seen highly educated people make poor money decisions.

I have also seen ordinary individuals build impressive wealth through discipline.

Success usually comes from habits repeated for years.

Not from occasional bursts of motivation.

Bad Financial Decision At 25-Financial Decisions That Create Wealth Instead of Destroying It

If bad decisions can cost lakhs, good decisions can create lakhs.

Some examples include:

Starting an SIP with your first salary.

Building a six-month emergency fund.

Learning about investing every month.

Increasing investments after every salary increment.

Avoiding unnecessary consumer debt.

Investing in skills that increase earning potential.

These decisions may appear small today.

However, over twenty or thirty years, they can completely transform your financial future.

That is the beauty of compounding.

Small advantages accumulate.

Small disadvantages accumulate too.

The direction matters more than the speed.

Bad Financial Decision At 25-My Biggest Observation About Financial Success

After studying personal finance content, listening to experts, and observing real-life examples, one pattern becomes obvious.

Financially successful people rarely make dramatic moves.

Instead, they make steady decisions repeatedly.

They save consistently.

They invest consistently.

They learn consistently.

They avoid emotional decisions.

They focus on long-term outcomes.

Most importantly, they understand that money is a tool.

It is not something to show off.

It is something to use strategically.

That mindset creates a huge difference over time.

The Real Meaning of the ₹40 Lakh Lesson

The number ₹40 lakh is not the most important part of this discussion.

The real lesson is understanding consequences.

Every financial decision has a future impact.

Some decisions create opportunities.

Others create obstacles.

At age 25, those consequences may be invisible.

At age 45, they become obvious.

The person who invested early enjoys financial flexibility.

The person who delayed often faces pressure.

The difference comes from years of accumulated choices.

That is why personal finance is not about getting rich quickly.

Frequently Asked Questions

What is the biggest financial mistake people make at 25?

Delaying investing and saving is often the most expensive mistake because it reduces the benefits of compounding.

Can one financial mistake really cost 40 lakh?

Yes. Lost investment growth, unnecessary debt, and missed opportunities can easily add up over decades.

Is starting late always bad?

Starting late is better than never starting, but earlier action generally produces stronger results.

How much should a 25-year-old save?

The exact amount depends on income, but consistent saving and investing should begin as early as possible.

What is the best financial habit to develop?

Paying yourself first by saving and investing before spending is one of the most effective habits.

Conclusion

Why 1 Bad Financial Decision At 25 Can Cost You 40 Lakh Later is ultimately a lesson about time, discipline, and awareness. Financial success rarely depends on luck. Instead, it depends on the choices made consistently over many years.

A small decision today can either create future wealth or future regret. The good news is that financial mistakes are often preventable. By investing early, controlling spending, avoiding unnecessary debt, building an emergency fund, and continuously improving financial knowledge, you can dramatically improve your long-term financial future.

The best time to make smart financial decisions was yesterday. The second-best time is today.

2 thoughts on “Bad Financial Decision At 25”