LIC Policy Surrender Before 3 Years : Easy Guide is one of the most searched topics among policyholders who are considering closing their insurance policy early. Many people purchase a policy with long-term goals in mind, but circumstances can change. Financial emergencies, changing priorities, or a better understanding of insurance products may lead someone to think about surrendering a policy before completing three years.

However, before making this decision, it is important to understand how LIC policy surrender works, how much money you may receive, what losses you might face, and whether better alternatives are available. I have seen many policyholders make quick decisions without understanding the financial impact, only to regret it later. This guide explains everything in simple language so you can make an informed choice.

Table of Contents

What Is LIC Policy Surrender Before 3 Years?

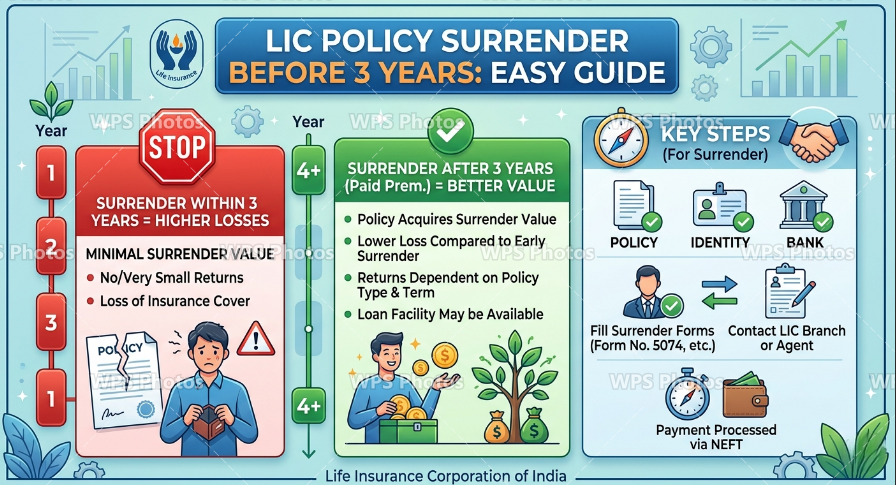

LIC Policy Surrender Before 3 Years refers to closing your Life Insurance Corporation policy before completing three policy years. When a policy is surrendered, the policyholder voluntarily terminates the contract and receives a surrender value if eligible.

Many traditional LIC plans require a minimum number of premiums to be paid before any surrender value becomes available. If the policy is surrendered too early, the amount received may be significantly lower than the total premiums paid.

This is why understanding the surrender rules is essential before taking any action. Insurance policies are generally designed for long-term financial protection and wealth creation rather than short-term returns.

LIC Policy Surrender Before 3 Years Rules

The rules for LIC Policy Surrender Before 3 Years vary depending on the type of policy.

Most traditional LIC policies require at least two or three full years of premium payments before they acquire a surrender value. If this condition is not met, the policyholder may receive little or no refund.

Important factors affecting surrender eligibility include:

- Type of LIC policy

- Number of premiums paid

- Policy term

- Sum assured

- Bonus eligibility

- Special policy conditions

Before surrendering any policy, always check the policy bond and official LIC guidelines.

Why Do People Consider LIC Policy Surrender Before 3 Years?

Many policyholders decide to surrender their policies due to personal financial situations.

Financial Emergencies

Unexpected expenses such as medical bills, business losses, or family obligations can create an urgent need for funds.

Wrong Policy Selection

Some individuals purchase policies without fully understanding their benefits and later realize that the plan does not match their financial goals.

Better Investment Options

Investors sometimes discover alternatives that offer higher flexibility or returns and consider switching.

Premium Affordability Issues

A change in income or employment status can make it difficult to continue premium payments.

How Much Money Will You Get?

One of the most common questions regarding LIC Policy Surrender Before 3 Years is how much money will be refunded.

The answer depends on several factors:

- Total premiums paid

- Policy type

- Duration completed

- Bonus accumulated

- Guaranteed surrender value rules

In many cases, surrendering early leads to a financial loss because the policy has not accumulated sufficient value.

Many insurance experts recommend checking the exact surrender value from LIC before making a final decision.

Understanding Surrender Value

The surrender value is the amount payable by LIC when a policy is voluntarily terminated before maturity.

There are generally two types of surrender values:

Guaranteed Surrender Value

This is calculated according to LIC’s predefined rules and policy terms.

Special Surrender Value

This may be higher than the guaranteed surrender value and depends on factors such as policy duration and bonus accumulation.

For LIC Policy Surrender Before 3 Years, the surrender value is often quite limited because the policy has not been active long enough to build substantial value.

Disadvantages of LIC Policy Surrender Before 3 Years

Before surrendering your policy, consider the following disadvantages.

Loss of Insurance Protection

The life insurance coverage ends immediately after surrender.

Financial Loss

You may receive less than the amount you have paid in premiums.

Loss of Future Bonuses

Any future bonus benefits associated with the policy will no longer apply.

Loss of Long-Term Benefits

Many LIC plans offer benefits that become more valuable over time.

Restarting Insurance Can Cost More

If you need insurance later, purchasing a new policy may involve higher premiums due to age or health conditions.

LIC Policy Surrender Before 3 Years-Alternatives to LIC Policy Surrender Before 3 Years

Instead of surrendering, you may want to explore other options.

Convert to Paid-Up Policy

A paid-up policy allows you to stop paying premiums while retaining a reduced insurance benefit.

Policy Loan

Some policies allow borrowing against the policy value instead of surrendering it.

Premium Adjustment

Depending on the policy, there may be options to adjust premium obligations.

Financial Planning Review

A professional financial advisor can help evaluate whether surrendering is truly the best choice.

Real-Life Example

I have seen a policyholder who purchased an LIC endowment plan and decided to surrender it after two years due to temporary financial stress.

After checking the surrender value, he realized the amount payable was much lower than expected. Instead of surrendering the policy, he chose an alternative arrangement and continued the policy. A few years later, he was happy that he had avoided an unnecessary loss.

This example highlights why understanding the details before surrendering is important.

When Does LIC Policy Surrender Before 3 Years Make Sense?

Although early surrender is often discouraged, there are situations where it may be reasonable.

Severe Financial Hardship

If immediate cash is essential for survival or emergencies.

Unsuitable Policy

If the policy was purchased without understanding its structure and clearly does not fit your needs.

Better Financial Strategy

If a well-researched alternative aligns more effectively with your financial objectives.

Even in these cases, comparing all available options is important before proceeding.

Documents Required for Policy Surrender

The surrender process usually requires:

- Original policy document

- Identity proof

- Address proof

- Bank account details

- Cancelled cheque

- Surrender request form

Requirements can vary depending on the specific policy and LIC branch.

LIC Policy Surrender Before 3 Years: Easy Guide-Step-by-Step LIC Policy Surrender Process

Visit Your LIC Branch

Contact the branch where your policy is serviced.

Request a Surrender Form

Fill out the required application accurately.

Submit Documents

Attach all supporting documents.

Verification Process

LIC verifies the information and eligibility.

Receive Payment

Once approved, the surrender value is credited to your registered bank account.

Expert Tips Before Surrendering

Calculate the Actual Loss

Understand exactly how much money you will receive and how much you may lose.

Compare Alternatives

Explore policy loans and paid-up options before surrendering.

Review Long-Term Goals

Consider whether the policy still supports your future financial plans.

Consult a Professional

A qualified financial advisor can help evaluate the consequences.

Read Policy Terms Carefully

Always review the policy bond and surrender conditions before making a decision.

Common Mistakes to Avoid

Acting Emotionally

Never surrender a policy solely because of temporary financial pressure.

Ignoring Alternatives

Many people overlook better options that may preserve policy benefits.

Not Checking Surrender Value

Always obtain the exact surrender value from LIC before making a decision.

Forgetting Insurance Needs

Life insurance protection remains important even if financial priorities change.

LIC Policy Surrender Before 3 Years vs Policy Continuation

Many policyholders face a difficult choice when they realize they may not want to continue their LIC policy. The question is whether to surrender the policy or keep paying premiums. The answer depends on your financial goals, cash flow, and insurance needs.

When you surrender a policy early, you may recover only a portion of the money paid. In contrast, continuing the policy allows it to build value over time and keeps your insurance protection active. I have often seen policyholders focus only on the immediate cash they can receive without calculating the long-term benefits they might lose.

For example, a policy that has been active for only two years may provide very little surrender value. However, if the same policy is maintained for several more years, it may accumulate bonuses and become eligible for higher benefits. Therefore, before choosing LIC Policy Surrender Before 3 Years, compare the surrender value with the expected future benefits.

How LIC Calculates Surrender Value

Understanding how LIC calculates surrender value helps policyholders make better decisions. Although formulas vary across plans, the surrender value generally depends on the following factors:

Number of Premiums Paid

The more premiums you have paid, the greater the chance of receiving a meaningful surrender value.

Policy Duration

Longer policy duration usually results in a higher surrender value.

Sum Assured

Policies with larger sum assured amounts may generate a different surrender value structure.

Bonus Accumulation

Some traditional LIC plans accumulate bonuses that may contribute to the final surrender value.

Policy Type

Endowment plans, money-back plans, whole-life plans, and ULIPs have different surrender value calculations.

Because every plan is different, it is always advisable to request an official surrender value statement from LIC before making a final decision.

LIC Policy Surrender Before 3 Years: Easy Guide-Common Reasons People Regret Surrendering Early

Many policyholders later realize they made a mistake by surrendering their policy too quickly.

They Needed Insurance Later

After surrendering a policy, some people discover that obtaining new insurance is more expensive because they are older.

They Lost Long-Term Benefits

Many LIC plans become more valuable over time due to bonuses and maturity benefits.

They Underestimated Their Loss

Some policyholders focus only on the refund amount and overlook the value of lost future benefits.

Their Financial Situation Improved

Temporary financial difficulties often improve, but a surrendered policy cannot always be restored easily.

These examples demonstrate why LIC Policy Surrender Before 3 Years should be considered carefully rather than emotionally.

Best Alternatives to LIC Policy Surrender Before 3 Years

Before surrendering your policy, explore the alternatives available.

Reduce Financial Burden

Review your monthly budget to see whether premium payments can still be managed.

Convert to Paid-Up Status

Many traditional policies can be converted into paid-up policies after meeting eligibility requirements.

Use Emergency Savings

If the financial challenge is temporary, using emergency funds may prevent unnecessary losses.

Seek Professional Advice

Financial planners often identify solutions that policyholders may not consider on their own.

A small amount of professional guidance can sometimes save thousands of rupees over the long term.

LIC Policy Surrender Before 3 Years and Tax Implications

Tax consequences are another important factor.

Depending on the policy and applicable tax regulations, surrendering a policy early may affect tax benefits previously claimed. If tax deductions were claimed under applicable sections of the Income Tax Act, certain situations may require reassessment of those benefits.

Tax rules can change over time, so it is wise to consult a qualified tax professional before surrendering your policy.

Ignoring tax implications can lead to unexpected liabilities later.

Pro Tips Most Policyholders Don’t Know

Many people are unaware of the following practical tips:

Request an Exact Surrender Value

Never rely on estimates. Ask LIC for the exact amount payable.

Compare Multiple Options

Review surrender, paid-up, loan, and continuation options side by side.

Review Financial Goals

Your decision should align with your overall financial plan rather than a short-term concern.

Avoid Peer Pressure

Many people surrender policies because friends or relatives recommend it. Always evaluate your personal situation first.

Think Long Term

Insurance products are generally designed for long-term financial planning, not short-term gains.

Case Study: A Realistic Scenario

Imagine a policyholder named Raj purchased an LIC endowment plan and paid premiums for two years. After facing temporary financial difficulties, he considered LIC Policy Surrender Before 3 Years.

Before proceeding, he contacted LIC and learned that the surrender value was much lower than the total premiums paid. Instead of surrendering, he adjusted his monthly expenses and continued paying premiums.

A few years later, his financial condition improved significantly. The policy continued earning benefits, and he retained life insurance protection throughout the period.

This example illustrates why understanding all available options before surrendering is important.

Final Expert Recommendation

In most situations, LIC Policy Surrender Before 3 Years should be considered only after exploring every alternative. Early surrender often results in financial loss, reduced insurance protection, and missed long-term benefits.

Before making your final decision:

- Calculate the exact surrender value.

- Compare all available alternatives.

- Review your long-term financial goals.

- Consider future insurance needs.

- Seek professional financial advice if necessary.

A well-informed decision today can prevent unnecessary losses and help secure your financial future more effectively.

LIC Policy Surrender Before 3 Years for Different LIC Plans

One important fact that many policyholders do not know is that surrender rules can vary significantly from one LIC plan to another. Therefore, when researching LIC Policy Surrender Before 3 Years, it is essential to understand your specific policy type rather than relying on general information.

Endowment Plans

Endowment plans are among the most popular LIC products. These plans combine insurance coverage with savings benefits. If surrendered early, policyholders often receive less than expected because the policy has not accumulated sufficient value.

Money Back Plans

Money Back Plans provide periodic payouts during the policy term. However, surrendering before three years may result in losing future payouts and bonus benefits.

Whole Life Plans

Whole Life Plans are designed to provide coverage for an extended period. Early surrender can significantly reduce the financial benefits that would otherwise accumulate over decades.

ULIPs

Unit Linked Insurance Plans have different surrender rules compared to traditional plans. Charges, lock-in periods, and fund performance can affect the final surrender value.

Understanding your policy category is the first step before considering LIC Policy Surrender Before 3 Years.

Warning Signs That You Should Review Your Policy

Not every policy should be surrendered. However, some situations indicate that a detailed review may be necessary.

Premiums Are Becoming Difficult to Pay

If premium payments consistently create financial stress, it may be time to evaluate alternatives.

Financial Goals Have Changed

People’s financial priorities evolve over time. A policy purchased years ago may no longer fit current objectives.

Duplicate Insurance Coverage

Some individuals accidentally purchase multiple policies that provide overlapping benefits.

Better Risk Protection Is Available

In certain situations, a separate term insurance policy may provide higher coverage at a lower cost.

These situations do not automatically mean you should surrender the policy. Instead, they suggest that a careful review is needed.

Mistakes to Avoid During LIC Policy Surrender Before 3 Years

Many policyholders make avoidable mistakes that increase their financial losses.

Not Understanding Policy Terms

Every LIC policy contains specific surrender conditions. Ignoring these details can lead to unrealistic expectations.

Following Advice Without Verification

Friends, relatives, and social media users may provide suggestions without understanding your financial situation.

Ignoring Tax Effects

Tax implications can influence the actual benefit of surrendering a policy.

Not Comparing Alternatives

Many people surrender first and evaluate alternatives later. The smarter approach is to compare all available options before taking action.

Making Decisions During Financial Stress

Stress often leads to short-term thinking. Whenever possible, make financial decisions calmly and after gathering complete information.

Long-Term Financial Impact of Early Surrender

When evaluating LIC Policy Surrender Before 3 Years, it is important to look beyond immediate cash requirements.

A policy often serves multiple purposes:

- Life insurance protection

- Long-term savings

- Financial discipline

- Wealth accumulation

- Family security

When a policy is surrendered, all of these benefits may disappear simultaneously.

For example, a person who surrenders a policy at age 30 may later need new insurance at age 40. Because age increases and health conditions may change, obtaining equivalent coverage could become significantly more expensive.

This is one reason financial planners usually recommend exploring every alternative before surrendering a policy.

How to Check LIC Surrender Value

Before taking any action, obtain an accurate surrender value estimate.

Through LIC Branch

Visit your nearest LIC office and request surrender value details.

Through LIC Agent

Your LIC advisor may help obtain current surrender value information.

Through Customer Support

LIC customer support channels can provide guidance regarding policy status and eligibility.

Through Online Services

Depending on policy availability, some details may be accessible through LIC’s digital services.

Never base your decision on assumptions. Always obtain official figures.

Financial Planning Lessons from LIC Policy Surrender Before 3 Years

There are valuable financial lessons that can be learned from this topic.

Understand Before You Buy

Many policyholders purchase products without fully understanding their benefits and limitations.

Review Policies Regularly

Annual reviews help ensure that insurance plans still align with financial goals.

Build an Emergency Fund

A strong emergency fund can reduce the likelihood of needing to surrender investments or insurance products during financial difficulties.

Separate Insurance and Investment Decisions

Many financial experts recommend evaluating insurance protection and investment objectives independently.

These lessons can improve overall financial management beyond insurance planning.

Frequently Asked Questions

Can I surrender my LIC policy before 3 years?

Yes, but eligibility and surrender value depend on the policy type and number of premiums paid.

Will I get all my money back?

No. Early surrender usually results in receiving less than the total premiums paid.

Is there any penalty for surrendering?

There may not be a direct penalty, but the surrender value can be significantly lower than your total investment.

Is a policy loan better than surrendering?

In many situations, a policy loan may be a better option because it allows you to retain insurance coverage.

How long does the surrender process take?

The processing time varies depending on documentation and verification requirements.

Conclusion

LIC Policy Surrender Before 3 Years is a major financial decision that should not be taken lightly. While surrendering may provide immediate liquidity, it often results in reduced returns, loss of insurance coverage, and missed long-term benefits. Before making a final decision, carefully evaluate your surrender value, compare alternative options, and consider your future financial needs. A thoughtful approach can help you avoid unnecessary losses and make the best choice for your financial future.