Save ₹75000 Tax Using 80D And 80C – Save ₹75000 Tax Using 80D And 80C is one of the most searched tax-saving strategies among salaried employees and self-employed individuals in India. Every year, millions of taxpayers pay more tax than necessary simply because they do not understand how Section 80C and Section 80D work together. The good news is that the Income Tax Act provides completely legal ways to reduce your taxable income and potentially save a significant amount of money.

Many people focus only on investments like PPF or ELSS and forget that health insurance can also provide valuable tax deductions. When both sections are used strategically, the total deduction becomes much larger than what most taxpayers expect. I have seen many taxpayers realize this only at the end of the financial year, when they start collecting documents and suddenly discover that they missed several opportunities to reduce their tax liability.

The biggest mistake people make is waiting until March for tax planning. Smart taxpayers start planning from the beginning of the financial year. This approach not only helps them save taxes but also improves their financial discipline. Whether you are a salaried employee, freelancer, consultant, or business owner, understanding how to Save ₹75000 Tax Using 80D And 80C can help you keep more of your hard-earned money.

In this guide, we will break down everything in simple language so that even a beginner can understand how these deductions work and how to maximize them legally.

What Is Section 80C And Why Is It Important?

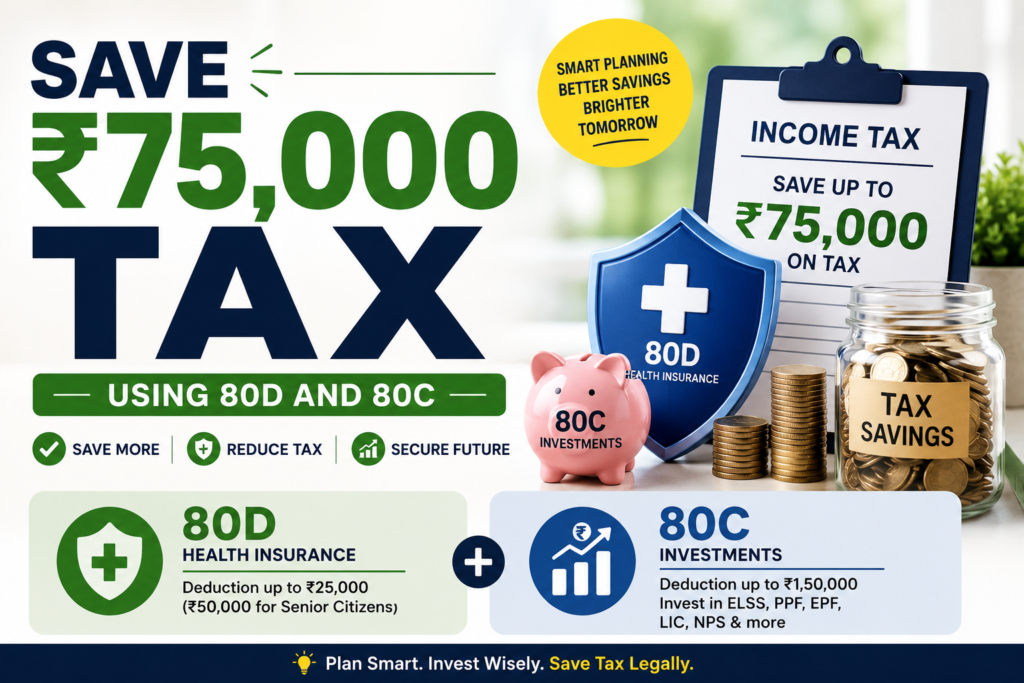

Section 80C is one of the most popular tax-saving provisions available under the old tax regime. It allows taxpayers to claim deductions on specific investments and expenses. The maximum deduction available under this section is ₹1.5 lakh per financial year.

Many financial experts recommend utilizing the full 80C limit because it not only reduces tax liability but also encourages long-term wealth creation. Over the years, I have noticed that people who consistently use 80C options often build stronger financial foundations than those who ignore them.

Popular investments and expenses covered under Section 80C include:

- Public Provident Fund (PPF)

- Employee Provident Fund (EPF)

- Equity Linked Savings Scheme (ELSS)

- National Savings Certificate (NSC)

- Tax Saving Fixed Deposits

- Sukanya Samriddhi Yojana

- Life Insurance Premiums

- Principal Repayment of Home Loan

- Children’s Tuition Fees

The benefit of Section 80C goes beyond tax savings. For example, PPF offers long-term wealth accumulation, ELSS provides market-linked growth potential, and EPF helps create retirement security. Therefore, using Section 80C wisely can improve both your current tax situation and your future financial health.

When planning to Save ₹75000 Tax Using 80D And 80C, Section 80C usually forms the foundation of your strategy because it offers the highest deduction limit available to most taxpayers

Table of Contents

Best Investments To Save ₹75000 Tax Using 80D And 80C

Choosing the right investment under Section 80C is important because not all tax-saving products provide the same benefits. Some offer guaranteed returns while others focus on long-term wealth creation.

PPF is often considered one of the safest options. It is backed by the government and offers tax-free maturity benefits. Investors looking for stability frequently choose PPF because it combines safety with tax savings.

ELSS funds are popular among investors seeking higher returns. These mutual funds invest primarily in equities and have the shortest lock-in period among tax-saving investments. While returns are not guaranteed, many investors have achieved substantial long-term growth through disciplined ELSS investing.

EPF is another powerful option, especially for salaried employees. Since contributions are automatically deducted from salary, employees often accumulate significant retirement savings without requiring additional effort.

Life insurance premiums also qualify for deduction under Section 80C. However, experts often recommend buying insurance primarily for protection rather than solely for tax benefits. A suitable term insurance plan can provide financial security for family members while contributing toward tax deductions.

For parents, children’s tuition fees can also contribute toward the Section 80C limit. Similarly, homeowners can claim principal repayment of eligible home loans.

A diversified approach generally works best. Instead of putting all money into one product, many taxpayers combine EPF, ELSS, PPF, and insurance premiums to fully utilize their 80C deduction limit.

Understanding Section 80D Tax Benefits

While most taxpayers know about Section 80C, fewer people fully understand the power of Section 80D. This section provides deductions for health insurance premiums and certain medical expenses.

Healthcare costs continue to rise every year. Therefore, health insurance is no longer optional for most families. Fortunately, the government encourages health insurance adoption through tax incentives under Section 80D.

The deduction limits generally include:

- Self, spouse, and dependent children

- Additional deduction for parents

- Higher deduction limits for senior citizens

A taxpayer can claim deductions for health insurance premiums paid for themselves and their family. If they also pay premiums for their parents, they may qualify for additional deductions.

One important point is that premiums should generally be paid through banking channels such as net banking, debit cards, credit cards, or UPI to qualify for deductions. Cash payments are usually not eligible except in specific circumstances related to preventive health check-ups.

I have often seen people delay purchasing health insurance because they view it as an unnecessary expense. However, one hospitalization can create a financial burden far greater than the annual premium amount. Therefore, Section 80D provides both financial protection and tax benefits simultaneously.

When combined correctly, Section 80D becomes a key component of the strategy to Save ₹75000 Tax Using 80D And 80C.

How Section 80C And Section 80D Work Together

Many taxpayers assume that Section 80C and Section 80D are connected under the same deduction limit. This is not correct. These sections operate independently.

This means you can claim deductions under Section 80C and then claim additional deductions under Section 80D separately. This creates a powerful opportunity to reduce taxable income significantly.

For example, suppose a taxpayer fully utilizes the ₹1.5 lakh deduction available under Section 80C. If the same taxpayer also purchases eligible health insurance policies for themselves and their parents, they may qualify for additional deductions under Section 80D.

This combined approach can substantially reduce taxable income and lead to meaningful tax savings. Depending on income level and tax slab, the actual tax saved can be considerable.

The key idea is simple. Instead of viewing tax-saving investments and health insurance separately, treat them as part of one integrated financial planning strategy. This mindset helps maximize benefits while improving overall financial security.

Most successful taxpayers who consistently Save ₹75000 Tax Using 80D And 80C follow this exact approach. They build a yearly plan, allocate money toward eligible investments, maintain adequate insurance coverage, and ensure all documentation remains organized for tax filing.

Common Mistakes That Reduce Tax Savings

One common mistake is investing at the last moment. Rushed decisions often lead to poor investment choices.

Another mistake is buying unsuitable insurance products solely for tax benefits. Tax savings should never be the only reason for purchasing a financial product.

Many taxpayers also forget to keep payment receipts and policy documents. Missing documentation can create problems while claiming deductions.

Some individuals fail to review deduction limits every year. Tax rules may change, and staying informed helps maximize available benefits.

Ignoring parents’ health insurance deductions is another costly mistake. Many taxpayers overlook this opportunity even when they are paying premiums for their parents.

Finally, some people choose the new tax regime without carefully comparing it against the old regime. Depending on your deductions, the old regime may sometimes provide better overall tax savings.

Detailed Example To Save ₹75000 Tax Using 80D And 80C

Understanding theory is helpful, but real numbers make everything easier. Let us see how a taxpayer can Save ₹75000 Tax Using 80D And 80C using a practical example.

Assume Rahul is a salaried employee with an annual taxable income of ₹12 lakh under the old tax regime. Like many employees, Rahul wants to reduce his tax burden legally while also strengthening his financial future.

During the financial year, Rahul contributes ₹80,000 to EPF through his salary. He additionally invests ₹70,000 in an ELSS mutual fund. This brings his total Section 80C deduction to ₹1.5 lakh.

Rahul also purchases a family health insurance policy and pays a premium for his parents’ health insurance. These premiums qualify under Section 80D.

Because Rahul utilizes both sections effectively, his taxable income reduces significantly. Since he falls in a higher tax slab, every deduction helps lower the tax payable on his income.

The important lesson from this example is that tax savings are often the result of planning rather than luck. Rahul did not buy unnecessary products. He simply used the provisions already available under the law.

I have seen many employees earning similar salaries pay substantially different amounts of tax. The difference usually comes from awareness and planning. Those who understand deductions often retain more of their income without doing anything illegal or complicated.

The goal should never be to chase tax-saving products blindly. Instead, choose products that match your financial goals and then enjoy the tax benefits that come with them. That is the smartest way to Save ₹75000 Tax Using 80D And 80C.

Save ₹75000 Tax Using 80D And 80C Through Smart Financial Planning

Tax planning works best when it becomes part of your overall financial strategy. Many people treat tax saving as a separate activity. However, the most successful taxpayers combine wealth creation, insurance protection, retirement planning, and tax optimization into one system.

Start by calculating your expected income at the beginning of the financial year. Next, determine how much of the Section 80C limit is already covered through EPF contributions. This step gives you clarity about the remaining amount you need to invest.

After that, evaluate your insurance needs. Health insurance should be chosen based on adequate coverage rather than tax deductions alone. A policy with insufficient coverage may save a small premium today but create major financial stress during a medical emergency.

Once these foundations are in place, you can select suitable investments. Younger investors often prefer ELSS because of its growth potential. Conservative investors may choose PPF due to its safety and government backing.

One approach I frequently hear from financial planners is to automate investments. Monthly SIPs in ELSS funds and systematic contributions to PPF help avoid last-minute decisions. This method also spreads investments throughout the year instead of creating pressure near the financial year-end.

The taxpayers who consistently Save ₹75000 Tax Using 80D And 80C usually follow a disciplined process. They invest regularly, maintain proper insurance coverage, preserve documentation, and review their strategy annually.

Best 80C Options For Different Types Of Taxpayers

Every taxpayer has different goals, risk tolerance, and financial responsibilities. Therefore, the best 80C option depends on individual circumstances.

For Salaried Employees

Salaried employees already contribute to EPF. This automatically utilizes part of their Section 80C limit. They can complement EPF with ELSS, PPF, or tax-saving fixed deposits.

Many salaried professionals prefer ELSS because it offers equity exposure and has a relatively short lock-in period. Long-term investors often find ELSS attractive due to its potential for wealth creation.

For Self-Employed Professionals

Self-employed individuals do not receive EPF benefits. Therefore, they often rely on PPF, ELSS, life insurance premiums, and NPS contributions to maximize deductions.

Self-employed taxpayers should focus on maintaining consistent investment habits because there are no automatic salary deductions to help them save.

For Parents

Parents can benefit from claiming deductions on children’s tuition fees. This provision can contribute significantly toward the Section 80C limit.

Many families also combine tuition fee deductions with life insurance premiums and PPF investments to achieve maximum utilization.

For Conservative Investors

Conservative investors typically prioritize safety over returns. For them, PPF, NSC, and tax-saving fixed deposits remain popular choices.

Although returns may be lower than equity-based investments, these options provide stability and predictability.

For Aggressive Investors

Aggressive investors often prefer ELSS funds because they offer market-linked growth opportunities. Over long periods, equities have historically outperformed many traditional investment products.

The right mix depends on your personal financial objectives. Regardless of the chosen products, proper planning can help Save ₹75000 Tax Using 80D And 80C while supporting broader wealth-building goals.

Best Health Insurance Strategy Under Section 80D

Health insurance is one of the most valuable financial tools available today. Medical inflation continues to increase, and treatment costs can become substantial even for common procedures.

A good strategy starts with ensuring adequate coverage for yourself, your spouse, and dependent children. After securing family coverage, evaluate whether your parents also need insurance protection.

Many taxpayers focus only on their own policies and ignore the additional deduction opportunities available for parents’ premiums. This can reduce the overall tax benefit they could otherwise claim.

When selecting a policy, compare factors such as:

- Coverage amount

- Network hospitals

- Claim settlement record

- Waiting periods

- Room rent limits

- Policy exclusions

Do not purchase a policy solely because it qualifies for a deduction. The primary purpose of health insurance is financial protection. Tax benefits should be viewed as an additional advantage.

I have personally observed cases where individuals purchased the cheapest available policy for tax purposes but later discovered that the coverage was inadequate during a medical emergency. Proper planning requires balancing affordability with meaningful protection.

A strong health insurance strategy contributes directly to the objective of Save ₹75000 Tax Using 80D And 80C while also safeguarding long-term financial stability.

Save ₹75000 Tax Using 80D And 80C: Step-By-Step Action Plan

Many readers understand the concepts but want a practical roadmap. Here is a straightforward process you can follow.

Step 1: Estimate Annual Income

Calculate your expected taxable income for the current financial year. This helps determine your likely tax liability.

Step 2: Review Existing Deductions

Check how much of your Section 80C limit is already utilized through EPF, life insurance premiums, or other eligible investments.

Step 3: Identify Remaining 80C Capacity

If you have not reached the deduction limit, decide whether ELSS, PPF, NSC, or another eligible product suits your needs.

Step 4: Evaluate Health Insurance Coverage

Review existing health insurance policies for yourself and your family. Ensure coverage remains adequate.

Step 5: Consider Parents’ Insurance

If appropriate, explore health insurance coverage for parents. This may provide additional deductions while improving family financial security.

Step 6: Maintain Documentation

Keep premium receipts, investment statements, and supporting records organized throughout the year.

Step 7: Review Before Filing

Before filing your return, verify all deduction claims and ensure documentation is complete.

Following these steps can make the process of Save ₹75000 Tax Using 80D And 80C far easier and more effective.

Tax Planning Mistakes That Cost Thousands Of Rupees

One major mistake is waiting until March to invest. Last-minute decisions often result in unsuitable products and missed opportunities.

Another common error is focusing only on tax savings while ignoring investment quality. Tax benefits are temporary, but investment performance affects wealth creation for years.

Some taxpayers buy multiple insurance products without understanding their features. This can lead to unnecessary expenses and inefficient coverage.

Others fail to compare tax regimes before making decisions. Depending on income, deductions, and financial goals, one regime may be more beneficial than the other.

Documentation issues also create problems. Missing receipts, incorrect records, and incomplete paperwork can delay or complicate tax filing.

A surprising number of taxpayers overlook deductions available through parents’ health insurance. This omission can reduce overall tax efficiency.

Finally, many people never review their strategy. Financial circumstances change over time. A tax plan that worked three years ago may not be optimal today.

Avoiding these mistakes can significantly improve your ability to Save ₹75000 Tax Using 80D And 80C while maintaining a stronger overall financial position.

Real-Life Scenario: Two Employees, Different Outcomes

Consider two employees earning the same salary.

The first employee ignores tax planning throughout the year. Near the end of the financial year, he rushes into random investments and purchases products he barely understands.

The second employee plans from April. She contributes regularly to eligible investments, maintains proper health insurance, and keeps all documents organized.

By the time tax filing season arrives, both employees have similar incomes. However, the second employee enjoys lower tax liability, better financial protection, stronger investment discipline, and less stress.

This example highlights an important truth. Tax savings are rarely about finding secret loopholes. Instead, they result from consistent planning and informed decision-making.

The taxpayers who successfully Save ₹75000 Tax Using 80D And 80C are often the same individuals who manage other aspects of their finances effectively.

Advanced Strategies To Save ₹75000 Tax Using 80D And 80C

Once you understand the basics, you can move to more advanced tax-planning techniques. These strategies are not complicated, but they require consistency and awareness throughout the financial year.

One effective strategy is to start tax planning in April rather than waiting until January or February. This gives you the entire year to spread investments gradually. Instead of investing a large amount at once, you can invest monthly. This approach reduces financial pressure and helps build discipline.

Another strategy is combining wealth creation and tax saving. For example, many investors choose ELSS because it offers both tax benefits and long-term growth potential. While returns are not guaranteed, ELSS has historically attracted investors looking for higher growth opportunities.

Similarly, PPF remains valuable for conservative investors seeking stability. By balancing growth-oriented and safety-oriented options, taxpayers can create a diversified financial plan.

Health insurance should also be reviewed annually. As income increases and family responsibilities change, coverage requirements may increase. Updating policies when necessary ensures adequate protection while continuing to enjoy tax benefits.

Many financial planners recommend treating tax planning as a by-product of financial planning. When your investments, insurance, and savings align with your goals, tax savings naturally follow. This mindset helps avoid poor decisions driven solely by tax considerations.

The most successful taxpayers who Save ₹75000 Tax Using 80D And 80C generally focus on long-term financial security rather than short-term tax reduction alone.

Save ₹75000 Tax Using 80D And 80C With Year-Round Planning

Year-round planning offers several advantages over last-minute tax saving. It allows you to evaluate options carefully, compare products, and avoid emotional decisions.

For example, if you decide in April to invest a specific amount every month, you can automate contributions through SIPs or standing instructions. This reduces the risk of forgetting investments and helps maintain consistency.

Health insurance premiums can also be scheduled in advance. By planning early, you can compare policies thoroughly instead of rushing to purchase a plan near the end of the financial year.

I have noticed that taxpayers who plan throughout the year generally experience less stress during tax season. Their documents are organized, deductions are already tracked, and investment goals remain on schedule.

Year-round planning also creates better financial habits. Instead of viewing tax saving as an annual task, it becomes part of an ongoing financial management process.

When combined with disciplined investing and adequate insurance coverage, this approach makes it easier to Save ₹75000 Tax Using 80D And 80C while simultaneously improving overall financial health.

Expert Tips To Maximize Tax Savings Legally

Start Early

Early planning provides flexibility and prevents rushed decisions. The earlier you begin, the easier it becomes to manage deductions effectively.

Review Existing Investments

Many taxpayers already have eligible investments but fail to account for them properly. Reviewing existing investments helps avoid duplication.

Avoid Product Mis-Selling

Never purchase a product solely because someone claims it will save tax. Understand the features, costs, benefits, and risks before investing.

Maintain Records

Organized records simplify tax filing and reduce the chances of missing deductions.

Reassess Every Year

Income levels, family situations, and financial goals change over time. Annual reviews ensure your strategy remains relevant.

Focus On Financial Goals

Tax savings are important, but long-term financial objectives should always remain the priority.

These simple habits can significantly improve your ability to Save ₹75000 Tax Using 80D And 80C while reducing unnecessary financial mistakes.

Frequently Asked Questions

Can I Claim Both Section 80C And Section 80D Together?

Yes. Section 80C and Section 80D operate independently. Eligible taxpayers can claim deductions under both sections if they satisfy the applicable requirements.

Is Health Insurance Mandatory To Claim Section 80D Benefits?

To claim deductions for health insurance premiums, you must purchase an eligible health insurance policy. Certain preventive health check-up benefits may also be available subject to applicable rules.

Which Is Better For Tax Saving: ELSS Or PPF?

There is no universal answer. ELSS offers market-linked growth potential, while PPF focuses on stability and government-backed security. The best choice depends on your goals and risk tolerance.

Can Salaried Employees Save ₹75000 Tax Using 80D And 80C?

Many salaried employees can significantly reduce tax liability by properly utilizing deductions available under these sections. Actual savings depend on income level, tax slab, and eligible deductions.

Does Section 80C Include Home Loan Benefits?

The principal repayment component of an eligible home loan may qualify under Section 80C, subject to applicable conditions.

Can I Claim Deductions For Parents’ Health Insurance?

Yes. Eligible premiums paid for parents may qualify for additional deductions under Section 80D.

Is Tax Planning Legal?

Absolutely. Tax planning uses deductions and benefits specifically provided by law. It is completely different from tax evasion, which is illegal.

Should I Invest Only For Tax Savings?

No. Investments should align with financial goals, risk tolerance, and time horizon. Tax benefits should be considered an additional advantage.

Common Myths About Tax Saving

Many myths continue to confuse taxpayers.

One myth is that tax planning is only for high-income earners. In reality, taxpayers across income levels can benefit from understanding deductions.

Another myth is that health insurance is purchased only for tax benefits. The primary purpose of health insurance is financial protection against medical expenses.

Some people believe tax-saving investments automatically generate high returns. This is not always true. Different products have different risk and return profiles.

A common misconception is that tax planning can be completed in one day. Effective tax planning is usually an ongoing process that spans the entire financial year.

Another myth is that only experts can understand tax deductions. While tax laws can appear complex, basic deductions such as Section 80C and Section 80D are relatively straightforward once explained clearly.

Understanding these realities helps taxpayers make informed decisions and improve their ability to Save ₹75000 Tax Using 80D And 80C.

Final Thoughts On Save ₹75000 Tax Using 80D And 80C

Save ₹75000 Tax Using 80D And 80C is not about finding shortcuts or exploiting loopholes. It is about understanding the benefits already available under the Income Tax Act and using them intelligently.

Section 80C encourages long-term savings and investment. Section 80D promotes health insurance coverage and financial protection. Together, these provisions can help reduce taxable income while strengthening overall financial security.

The most important step is to begin early. Waiting until the final weeks of the financial year often leads to rushed decisions and missed opportunities. Instead, create a simple annual plan, invest consistently, review insurance coverage regularly, and maintain proper records.

Over time, these habits not only improve tax efficiency but also contribute to better wealth creation, stronger financial discipline, and greater peace of mind.

Many taxpayers focus exclusively on how much tax they can save this year. A better question is how today’s financial decisions can improve both tax savings and future financial stability. When viewed from that perspective, Section 80C and Section 80D become more than tax-saving tools—they become part of a broader financial success strategy.

If you have not yet reviewed your investments and insurance coverage for the current financial year, now is a good time to start. A few well-planned decisions today could help you Save ₹75000 Tax Using 80D And 80C while building a stronger financial future for yourself and your family.

Conclusion

Save ₹75000 Tax Using 80D And 80C remains one of the most practical and legal tax-saving strategies available under the old tax regime. By combining eligible investments under Section 80C with health insurance deductions under Section 80D, taxpayers can significantly reduce taxable income while improving financial security.

The key is not complexity but consistency. Start early, choose suitable investments, maintain adequate health insurance, keep documentation organized, and review your strategy every year. These simple actions can create meaningful tax savings and support long-term wealth creation.

Take action today rather than waiting until the end of the financial year. Your future self will thank you for the financial discipline, protection, and tax efficiency that come from smart planning