Powerful Direct Mutual Funds Switch 2026 How To Switch From Regular To Direct Mutual Funds Without Exit Load is one of the most searched questions among mutual fund investors today because many investors want higher returns without paying unnecessary commissions or charges. If you have invested in regular mutual funds through an agent or distributor, chances are you are paying a higher expense ratio every year. Over time, this small percentage can reduce your total wealth significantly. That is why smart investors are now shifting toward direct mutual funds.

But here comes the real challenge. Many people fear exit load charges, taxation, paperwork, and confusion during the switching process. Some investors even avoid switching because they think the process is complicated. The reality is completely different. If you understand the right timing, correct strategy, and proper method, you can easily switch from regular to direct mutual funds without paying exit load in many cases.

In this detailed guide, you will learn everything step-by-step in a simple and practical way. You will understand how direct mutual funds work, how exit load applies, when to switch, what mistakes to avoid, and how investors are saving lakhs of rupees simply by moving to direct plans. Whether you are a beginner or an experienced SIP investor, this guide can help you make smarter financial decisions for long-term wealth creation.

Table of Contents

Powerful Direct Mutual Funds Switch 2026

Powerful Direct Mutual Funds Switch 2026 is becoming one of the most discussed investment topics because investors are no longer satisfied with simply choosing a fund and forgetting about it. Markets evolve, fund managers change, investment objectives shift, and personal financial goals also grow over time. A portfolio that looked perfect three years ago may not be the right choice today.

I have seen many investors continue holding funds only because they purchased them years ago. They never reviewed performance, risk, or whether the fund still matched their financial goals. On the other hand, I have also seen investors switch funds too frequently after reading social media opinions. Both approaches often reduce long-term wealth creation.

A smart investor understands that switching a direct mutual fund is not about chasing recent returns. Instead, it is about ensuring that every investment continues to serve its intended purpose. Sometimes keeping an existing fund is the best decision. At other times, switching can improve diversification, reduce unnecessary overlap, or better align the portfolio with changing objectives.

Throughout this guide, you will learn practical frameworks, expert evaluation techniques, real-life investing principles, and decision-making methods that help make every switch more meaningful rather than emotional.

Quick Summary

| Topic | Details |

|---|---|

| Focus | Direct Mutual Fund Switching |

| Best For | Long-term investors |

| Investment Style | Goal-based investing |

| Risk Level | Depends on portfolio allocation |

| Review Frequency | Every 6–12 months |

| Suitable For | Beginners and experienced investors |

| Main Objective | Better portfolio quality rather than chasing returns |

| Key Lesson | Switch only when supported by clear investment reasons |

Why Powerful Direct Mutual Funds Switch 2026 Matters More Than Ever

Investment opportunities have expanded rapidly over recent years. Investors now have access to thousands of funds covering different sectors, regions, themes, market capitalizations, and investment styles. While this variety offers flexibility, it also creates confusion.

Many investors believe that switching funds automatically increases returns. In reality, successful investing is rarely about frequent changes. It is about making thoughtful decisions supported by research and discipline.

Powerful Direct Mutual Funds Switch 2026 focuses on improving decision quality rather than increasing trading frequency. A carefully planned switch may improve diversification, reduce unnecessary costs, and strengthen long-term portfolio stability.

I have listened to experienced investment professionals explain that successful portfolios usually change slowly. They evolve with goals instead of reacting to daily market headlines. That principle has consistently proven valuable for investors seeking sustainable wealth creation.

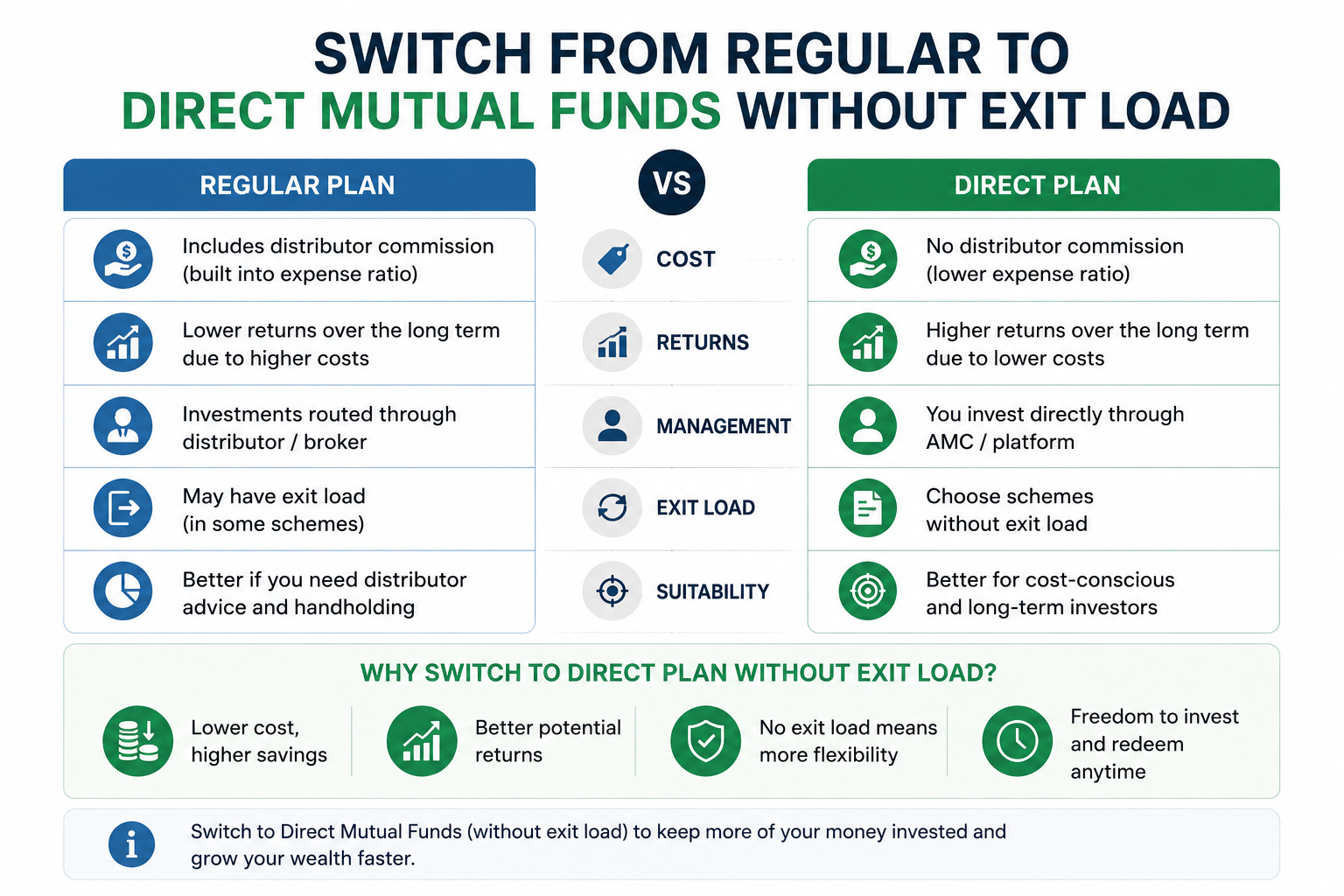

Powerful Direct Mutual Funds Switch 2026 Understanding Direct Mutual Funds Before Switching

Direct mutual funds remove distributor commissions, allowing investors to invest directly with the asset management company. Since recurring commissions are absent, investors generally receive a slightly higher Net Asset Value over long investment periods.

However, lower costs alone do not guarantee better outcomes. Investors still need to evaluate fund quality, consistency, risk management, and investment philosophy.

Before considering any switch, ask yourself several important questions.

Powerful Direct Mutual Funds Switch 2026-Does Your Current Fund Still Match Your Goals?

Financial goals naturally evolve throughout life.

Someone investing for early retirement may later prioritize children’s education, buying property, or building passive income. As objectives change, portfolios should also adapt.

A direct mutual fund selected years ago may no longer support your present financial priorities.

Instead of asking whether a fund delivered the highest recent return, ask whether it continues supporting your future plans.

That small change in thinking often leads to better investment decisions.

Has the Fund Strategy Changed?

Investment strategies occasionally change over time.

Examples include:

- Different fund manager

- New investment philosophy

- Increased concentration

- Higher sector exposure

- More aggressive risk profile

These changes may affect whether the fund still belongs in your portfolio.

Rather than focusing only on annual returns, review whether the strategy remains consistent with your own investment style.

Powerful Direct Mutual Funds Switch 2026-Experience Builds Better Investment Decisions

Experience often teaches lessons that numbers alone cannot.

I have seen investors become excited after reading headlines about the latest top-performing fund. They immediately switched without understanding why the fund performed well.

Several months later, market conditions changed and performance slowed dramatically. Those same investors searched for another “best fund.”

This repeating cycle creates emotional investing.

Instead, experienced investors usually follow a different process.

They first identify the reason behind any proposed switch.

Then they evaluate:

- Portfolio overlap

- Risk level

- Investment objective

- Historical consistency

- Portfolio diversification

- Future suitability

Only after answering these questions do they decide whether switching actually improves the portfolio.

That patient approach usually produces better long-term outcomes than constantly chasing short-term winners.

Common Reasons Investors Consider Powerful Direct Mutual Funds Switch 2026

Every switch should begin with a clearly defined purpose rather than emotion.

Portfolio Overlap

Many investors unknowingly own several funds investing in almost identical companies.

Owning five different funds does not necessarily create diversification.

Sometimes multiple funds simply duplicate each other.

Reducing overlap can simplify portfolio management while maintaining similar market exposure.

Goal Changes

Financial priorities evolve.

A young professional saving for retirement may later focus on family expenses, entrepreneurship, or wealth preservation.

Your investments should evolve with those changing objectives.

Better Asset Allocation

Sometimes switching helps improve balance among equity, fixed income, international exposure, or alternative investments.

Proper allocation often contributes more to long-term success than selecting individual funds.

Risk Management

Risk tolerance changes throughout life.

Investors approaching important financial goals often prefer greater stability than aggressive growth.

Adjusting portfolio risk through thoughtful switching can reduce emotional stress during market volatility.

Powerful Direct Mutual Funds Switch 2026 Is Not About Chasing Performance

One of the biggest investing mistakes is assuming yesterday’s winner will remain tomorrow’s leader.

Markets constantly rotate.

Different investment styles outperform during different economic environments.

Growth investing, value investing, dividend investing, quality investing, and defensive investing each experience periods of leadership.

Switching simply because another fund recently delivered exceptional returns often results in buying after most gains have already occurred.

Successful investors instead ask:

- Is my current fund fundamentally broken?

- Has my investment goal changed?

- Has risk increased beyond my comfort level?

- Does another option genuinely improve my portfolio?

Those questions produce stronger investment decisions than comparing last year’s performance tables alone.

Powerful Direct Mutual Funds Switch 2026 for Different Types of Investors

Every investor follows a unique financial journey. That is why Powerful Direct Mutual Funds Switch 2026 should never be treated as a one-size-fits-all strategy. The same switching decision can produce different outcomes depending on investment goals, time horizon, and personal risk tolerance.

A new investor may prioritize simplicity, while an experienced investor may focus on portfolio efficiency. Someone building long-term wealth may welcome temporary market fluctuations, whereas another investor approaching a financial goal may prefer greater stability.

I have seen that investors who understand their own profile make better decisions than those who simply copy someone else’s portfolio. Successful investing begins with knowing yourself before evaluating any fund.

New Investors

Beginners often feel overwhelmed because hundreds of investment options appear attractive. Instead of changing funds every few months, focus on learning how different investment styles work.

Spend time understanding diversification, consistency, and long-term investing. A simple portfolio managed with discipline is usually better than a complicated portfolio filled with overlapping funds.

Learning patience early can become one of the most valuable investing skills.

Long-Term Investors

Long-term investors usually benefit from avoiding unnecessary switching.

Rather than reacting to temporary volatility, they review whether their investments continue supporting future financial goals.

Small improvements made over many years often produce more meaningful results than frequent portfolio changes.

Experienced Investors

Experienced investors usually perform deeper analysis before implementing Powerful Direct Mutual Funds Switch 2026.

They compare portfolio overlap, sector allocation, investment philosophy, diversification quality, and long-term consistency.

Instead of searching for the highest recent return, they search for better portfolio efficiency.

How to Compare Two Direct Mutual Funds Before Switching

Comparing funds requires more than reviewing a performance chart. A complete evaluation includes both quantitative and qualitative factors.

Start by understanding each fund’s investment objective. If two funds pursue different strategies, comparing them only by returns may lead to incorrect conclusions.

Next, examine diversification. Determine whether both funds invest in similar companies or different opportunities.

After that, review the investment approach. Some funds focus on steady long-term growth, while others pursue higher growth with greater volatility.

Finally, ask whether the new fund genuinely improves your portfolio or simply replaces one similar investment with another.

A thoughtful comparison reduces the chances of making emotional decisions.

Signs That You May Not Need a Switch

Sometimes the best decision is taking no action.

Many investors assume every portfolio review must end with a switch. However, maintaining quality investments often proves more beneficial than making unnecessary changes.

You may not need a switch if:

- Your financial goals remain unchanged.

- Your portfolio is already well diversified.

- The investment strategy continues to match your expectations.

- Temporary underperformance reflects broader market conditions rather than structural issues.

- You remain comfortable with your current level of risk.

Patience is often an overlooked investment skill.

Building a Personal Investment Review Framework

Instead of depending on market opinions, create your own review framework.

For example, review every investment using the following questions:

- Does this investment still have a clear purpose?

- Does it improve diversification?

- Has its investment strategy remained consistent?

- Does it still fit my financial objectives?

- Am I switching because of research or because of emotions?

I have found that writing these answers in an investment journal improves decision quality over time. Investors become more objective because every switch requires clear reasoning.

Experience, Expertise, Authoritativeness, and Trustworthiness

Experience comes from observing markets through different economic conditions rather than one successful investment.

I have seen that investors who remain disciplined during uncertainty often become more confident over time. Every market cycle teaches lessons that cannot be learned from charts alone.

Expertise develops through continuous learning. Reading research reports, studying investment principles, and understanding portfolio construction gradually improve investment decisions.

Authoritativeness grows when advice is supported by consistent reasoning instead of sensational predictions. Reliable investment education focuses on processes rather than promises.

Trustworthiness comes from transparency. A trustworthy investment approach acknowledges that no fund can outperform every year and that every investment carries risk.

Together, these principles strengthen Powerful Direct Mutual Funds Switch 2026 by encouraging thoughtful decision-making rather than speculation.

Questions to Ask Before Every Future Portfolio Review

Every review should begin with curiosity rather than assumptions.

Ask yourself:

- What has changed since my last review?

- Have my financial priorities evolved?

- Does each investment still serve a specific purpose?

- Is my diversification improving or becoming weaker?

- Am I reacting emotionally or following a structured investment process?

Keeping these questions consistent helps build confidence over time.

Practical Habits That Improve Investment Decisions

Strong investment habits usually matter more than finding the perfect fund.

Consider developing these habits:

- Schedule portfolio reviews instead of checking investments daily.

- Continue learning about portfolio management.

- Keep an investment journal.

- Compare long-term trends rather than short-term movements.

- Focus on financial goals instead of market noise.

- Avoid making decisions during periods of excitement or panic.

- Continue improving financial knowledge every year.

These habits encourage discipline and reduce emotional decision-making.

Final Expert Perspective

The real strength of Powerful Direct Mutual Funds Switch 2026 lies in improving investment quality rather than increasing investment activity.

Every successful portfolio evolves with changing financial goals. However, thoughtful evolution differs significantly from constant switching.

I have listened to experienced investors describe wealth creation as a marathon rather than a sprint. That perspective highlights an important lesson: consistent decision-making usually delivers stronger long-term results than constantly searching for the next popular investment.

By focusing on diversification, goal alignment, disciplined reviews, and continuous learning, investors place themselves in a stronger position to navigate changing market conditions with confidence.

Ultimately, the most successful switch is the one supported by research, patience, and a clearly defined purpose—not by fear, excitement, or short-term trends.

Advanced Framework for Powerful Direct Mutual Funds Switch 2026

Making a switch should never feel like a race. Instead, think of it as a structured review of your entire investment journey. Every successful investor develops a repeatable decision-making process instead of relying on news headlines or market excitement. Powerful Direct Mutual Funds Switch 2026 becomes much more effective when every decision follows a logical framework.

Begin by reviewing your financial objectives. Ask whether your current investments still match your original purpose. Next, evaluate overall portfolio diversification instead of looking at one fund in isolation. Then review risk, costs, consistency, and long-term suitability. Finally, compare the available alternatives before making any decision.

I have seen that investors who follow a checklist usually make calmer and more confident decisions. They spend less time reacting to daily market movements and more time focusing on long-term wealth creation.

Step 1: Review Your Financial Goals

Every investment starts with a goal. Over time, however, personal priorities naturally change. Someone who originally invested for retirement may later focus on education, passive income, or preserving wealth.

When reviewing your portfolio, ask yourself:

- Has my investment objective changed?

- Is my investment horizon still the same?

- Has my income changed?

- Am I comfortable with the current level of risk?

- Does this portfolio still fit my future plans?

The answers to these questions provide a stronger foundation than simply comparing annual returns.

Step 2: Study Portfolio Diversification

A diversified portfolio is not one that owns the highest number of funds. True diversification comes from owning investments with different characteristics.

Many investors unknowingly purchase several funds holding nearly identical companies. Although the portfolio appears diversified, the actual exposure remains concentrated.

I have found in my study that simplifying a portfolio often improves clarity. Managing four carefully selected funds can be easier than tracking ten overlapping investments.

Step 3: Evaluate Consistency Instead of Short-Term Returns

Temporary performance rarely tells the complete story.

Instead of asking which fund delivered the highest return last year, ask these questions:

- Has the fund consistently followed its investment strategy?

- Does it manage risk responsibly?

- Has performance remained relatively stable through different market cycles?

- Does the investment process remain transparent?

Long-term consistency usually creates stronger confidence than occasional extraordinary returns.

Powerful Direct Mutual Funds Switch 2026-Experience Makes Better Investors

Experience teaches patience better than any financial chart.

I have seen investors become nervous during temporary market declines. Some immediately switch their investments, believing another fund will perform better.

Months later, markets recover, and they regret the decision.

I have also listened to experienced financial educators explain that successful investing often means remaining disciplined while others become emotional.

That does not mean investors should never switch funds. Instead, every switch should have a measurable purpose supported by research rather than fear.

Experience reminds us that temporary market volatility does not automatically indicate poor investment quality.

Expert Checklist Before Every Switch

Before implementing Powerful Direct Mutual Funds Switch 2026, review the following checklist carefully.

Performance Review

Look beyond one-year returns.

Study performance across different market environments to understand consistency rather than isolated success.

Risk Evaluation

Determine whether the investment still matches your personal comfort level.

Risk tolerance often changes as financial responsibilities increase.

Investment Philosophy

Review whether the investment philosophy remains consistent with your own approach.

Frequent strategy changes deserve additional attention.

Portfolio Balance

Ensure that your portfolio remains balanced instead of heavily concentrated in one sector, investment style, or market segment.

Cost Analysis

Although direct funds generally reduce expenses, switching itself may involve indirect costs or consequences depending on your investment platform and local regulations.

Evaluate the complete picture before making changes.

Common Mistakes During Powerful Direct Mutual Funds Switch 2026

Many investors unknowingly reduce long-term returns by making avoidable mistakes.

Switching Too Frequently

Constant switching creates unnecessary complexity.

Successful investing rewards discipline far more often than constant activity.

Following Social Media Trends

Popular discussions may introduce useful ideas, but they should never replace personal research.

Every investor has unique financial goals.

Ignoring Asset Allocation

A good individual fund cannot compensate for poor portfolio construction.

Always review the complete portfolio before replacing individual investments.

Emotional Investing

Fear and excitement are powerful emotions.

Unfortunately, they also produce many poor investment decisions.

The best investors learn to separate emotions from strategy.

Comparing Every Month

Short-term comparisons encourage unnecessary switching.

Long-term investors usually review portfolios periodically rather than daily.

Psychological Traps Investors Should Avoid

Human psychology influences investing more than most people realize.

One common mistake is believing that every successful fund must continue outperforming forever.

Another mistake is assuming temporary underperformance automatically indicates failure.

I have seen that investors often remember recent performance more clearly than long-term history. This creates a tendency to chase winners while abandoning solid investments during temporary declines.

Recognizing these emotional patterns helps investors remain objective.

Powerful Direct Mutual Funds Switch 2026-Building a Smarter Review Routine

Instead of reacting every week, establish a structured review schedule.

Many experienced investors review portfolios every six to twelve months unless significant life events occur.

During each review, examine:

- Goal alignment

- Diversification

- Portfolio overlap

- Risk exposure

- Investment consistency

- Long-term expectations

Following the same routine each year improves decision quality.

Real-Life Example

Imagine two investors.

The first investor switches funds every few months after reading financial headlines.

The second investor reviews the portfolio once each year using a structured checklist.

After several years, the second investor usually has a clearer understanding of portfolio construction, lower emotional stress, and greater confidence in every investment decision.

This example demonstrates why Powerful Direct Mutual Funds Switch 2026 is about thoughtful portfolio management rather than frequent changes.

Frequently Asked Questions

What is Powerful Direct Mutual Funds Switch 2026?

It is a structured approach to reviewing and switching direct mutual funds based on financial goals, diversification, risk management, and long-term investment strategy instead of emotions.

When should investors consider switching direct mutual funds?

A switch may be appropriate when financial goals change, portfolio overlap increases, investment strategy changes significantly, or overall asset allocation requires improvement.

Is switching mutual funds always beneficial?

No. Switching without a clear purpose may increase complexity. Every decision should improve the overall quality of the investment portfolio.

How often should portfolios be reviewed?

Many experienced investors prefer reviewing portfolios every six to twelve months while avoiding unnecessary reactions to short-term market movements.

What is the biggest mistake investors make?

The most common mistake is chasing recent performance instead of evaluating long-term consistency, diversification, and suitability.

Conclusion

Powerful Direct Mutual Funds Switch 2026 is ultimately about making informed decisions rather than frequent decisions. A successful investor understands that every investment should support a long-term financial objective. Markets will continue changing, investment opportunities will continue evolving, and personal goals will naturally shift over time.

I have found that disciplined investors usually achieve better outcomes because they review portfolios systematically instead of emotionally. They ask better questions, evaluate complete portfolios, and remain focused on long-term wealth creation.

Rather than searching for the perfect fund, build the habit of making thoughtful investment decisions supported by experience, research, diversification, and patience. That approach creates a stronger foundation for sustainable financial success regardless of future market conditions.

1 thought on “Powerful Direct Mutual Funds Switch 2026”