New Vs Old Tax Regime Calculator For 15 LPA Salary is one of the most searched financial topics among salaried employees in India right now because many taxpayers feel confused while selecting the right tax regime every financial year. Most people earning around 15 lakh salary think the new tax regime automatically saves more tax because of lower slab rates. However, the reality is very different. Your final tax liability depends on deductions, exemptions, HRA benefits, home loan interest, investments under Section 80C, insurance premiums, and several other factors. This is why blindly choosing one regime can cost you thousands of rupees every year. If you are a salaried employee trying to understand which tax regime is better for 15 LPA salary in 2026, then this detailed guide will help you calculate everything in the simplest way possible. You will learn practical examples, tax calculations, smart strategies, hidden mistakes people make, and expert-level tax-saving tips that most blogs never explain properly.

Table of Contents

What Is New Vs Old Tax Regime Calculator For 15 LPA Salary

The New Vs Old Tax Regime Calculator For 15 LPA Salary is a financial comparison method that helps salaried employees understand which tax regime reduces their overall tax burden. The Indian government introduced the new tax regime to simplify taxation with lower slab rates and fewer deductions. On the other hand, the old tax regime continues to offer traditional tax-saving benefits through deductions and exemptions. Because of this, taxpayers earning 15 lakh annually often struggle to decide which option works best for them.

A simple tax calculator compares taxable income after considering all eligible deductions like HRA, Section 80C investments, NPS contributions, health insurance premiums, standard deduction, and home loan interest. The result shows how much tax you pay under each regime. This comparison becomes extremely important because even a small difference in deductions can completely change the final outcome. Many salaried employees switch to the new regime assuming it is simpler, but later realize they lost valuable tax-saving opportunities. Therefore, using a proper comparison calculator before filing income tax returns is one of the smartest financial decisions you can make in 2026.

Why Salaried Employees With 15 LPA Salary Must Compare Both Tax Regimes

A salary of 15 lakh per annum places many professionals in the higher tax brackets. This means poor tax planning can significantly increase tax liability. Most IT professionals, corporate employees, engineers, banking professionals, and managers fall into this income category. Because their income is moderately high, the difference between the new and old tax regime can become very large depending on investment habits and deductions.

For example, suppose one employee invests heavily in ELSS mutual funds, pays home loan EMI, contributes to NPS, and claims HRA. In that case, the old regime may save more money. However, another employee living with parents, having no home loan, and not making investments may benefit more from the new regime. This is why there is no universal answer. The right choice depends completely on personal financial structure.

Many taxpayers also ignore future financial goals while selecting tax regimes. They choose the new regime for short-term convenience but stop investing regularly because deductions no longer motivate them. Over time, this affects long-term wealth creation. Therefore, comparing both tax regimes is not just about saving tax this year. It is also about building disciplined financial habits that help create wealth in the future.

Understanding The New Tax Regime In 2026

The new tax regime was introduced to simplify the income tax structure and reduce dependency on exemptions. It offers lower tax slab rates compared to the old regime. However, most deductions and exemptions are not available under this system. The government designed it mainly for individuals who prefer simple taxation without investment-related paperwork.

Under the new regime, salaried employees cannot claim benefits like HRA exemption, LTA, Section 80C deductions, home loan interest for self-occupied property, and several other traditional deductions. However, taxpayers still get the standard deduction benefit and some limited allowances depending on updated rules.

Many young professionals prefer the new regime because they do not want to lock money in tax-saving instruments. They enjoy higher in-hand salary and simplified filing. However, this approach may not always maximize wealth creation. Financial discipline becomes extremely important because you no longer invest merely for tax savings.

The biggest advantage of the new regime is simplicity. You avoid maintaining multiple investment proofs and complicated calculations. Moreover, if you have fewer deductions, the lower slab rates can reduce your tax burden considerably. Therefore, professionals with minimal investments often find this regime more beneficial.

Understanding The Old Tax Regime In 2026

The old tax regime follows the traditional taxation structure where taxpayers can claim multiple deductions and exemptions to reduce taxable income. This regime remains highly beneficial for salaried employees who actively invest and plan finances strategically. People earning 15 lakh salary often save substantial tax under the old regime if they fully utilize deductions.

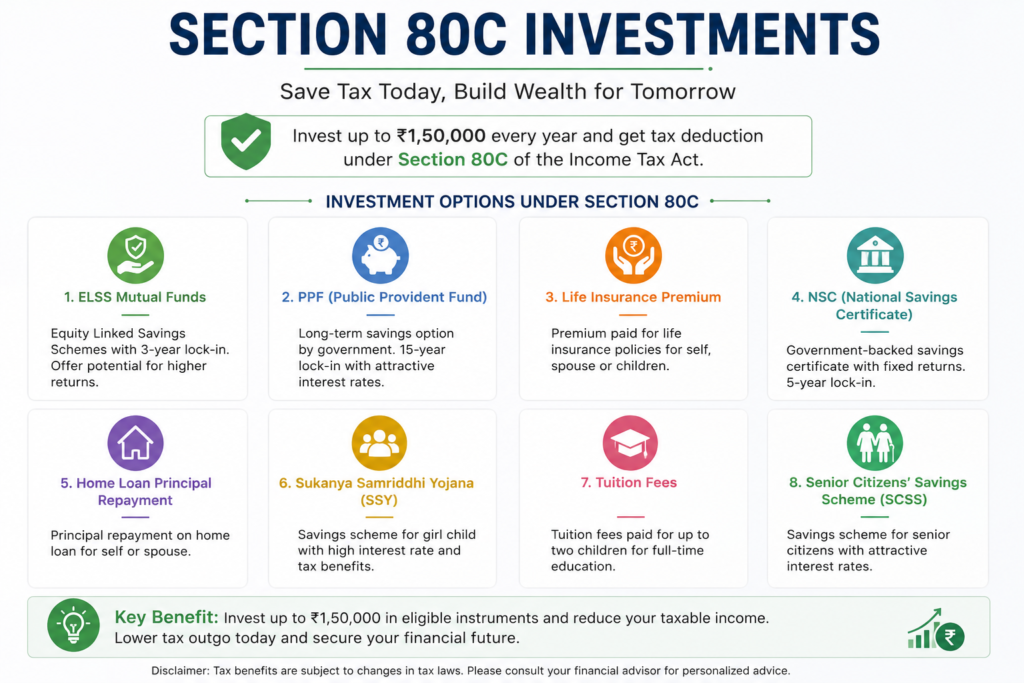

Some major deductions available include Section 80C investments up to ₹1.5 lakh, NPS deduction under Section 80CCD(1B), health insurance premium under Section 80D, home loan interest deduction, HRA exemption, LTA, education loan interest, and donations under Section 80G. These deductions collectively reduce taxable income significantly.

The old regime encourages disciplined investing habits. Taxpayers invest in PPF, ELSS funds, EPF, life insurance, Sukanya Samriddhi Yojana, and NPS to reduce taxes while building future wealth. Therefore, many financial advisors still recommend the old regime for long-term financial planning.

However, the biggest challenge is complexity. Taxpayers must maintain investment proofs, rent receipts, insurance documents, and other paperwork carefully. Additionally, if you fail to invest properly, the higher slab rates can increase tax liability substantially. Therefore, the old regime works best for financially disciplined individuals who actively manage investments and deductions.

New Vs Old Tax Regime Calculator For 15 LPA Salary With Real Example

Let us understand this with a realistic salary breakup example. Assume Rahul is a salaried employee earning 15 lakh annually in India.

Annual Salary: ₹15,00,000

Under the old tax regime, Rahul claims:

- Standard deduction: ₹50,000

- Section 80C investments: ₹1,50,000

- NPS contribution: ₹50,000

- Health insurance premium: ₹25,000

- Home loan interest: ₹2,00,000

- HRA exemption: ₹1,20,000

After deductions, Rahul’s taxable income reduces significantly. As a result, his total tax liability becomes much lower compared to the new regime.

Under the new regime, most deductions disappear. Even though slab rates are lower, the taxable income remains much higher because deductions are unavailable. Consequently, Rahul may end up paying more tax overall.

This example clearly shows why salary structure and investment pattern matter more than slab rates alone. A proper New Vs Old Tax Regime Calculator For 15 LPA Salary helps taxpayers identify the exact regime that minimizes tax legally and efficiently.

Key Deductions That Can Make Old Regime Better

One of the biggest reasons why many salaried employees still prefer the old regime is the power of deductions. These deductions directly reduce taxable income, which lowers overall tax burden substantially. Understanding these deductions properly can help taxpayers save thousands of rupees every year.

Section 80C Investments

Section 80C remains the most popular tax-saving provision in India. It allows deductions up to ₹1.5 lakh through investments like ELSS mutual funds, PPF, EPF, life insurance premiums, tax-saving fixed deposits, and Sukanya Samriddhi Yojana. Most salaried employees already contribute to EPF through their employer, which automatically helps utilize a portion of this deduction.

NPS Contribution Benefits

National Pension System contributions provide additional deduction benefits under Section 80CCD(1B). Taxpayers can claim an extra ₹50,000 deduction beyond the 80C limit. This makes NPS one of the most powerful long-term tax-saving investments for salaried professionals.

Home Loan Interest Deduction

Employees paying home loan EMIs can claim deductions on interest payments up to ₹2 lakh for self-occupied properties. This single deduction alone can make the old regime far more beneficial than the new regime.

HRA Exemption

House Rent Allowance exemption helps salaried employees living in rented accommodation reduce taxable income considerably. Professionals living in metro cities often save substantial tax through HRA benefits because rental expenses are usually high.

When New Tax Regime Is Better For 15 LPA Salary

Although many people assume the old regime always wins, there are several situations where the new tax regime becomes more beneficial. Understanding these cases helps avoid unnecessary tax-saving investments that may not align with financial goals.

The new regime works best for salaried employees who have very limited deductions. For instance, if someone lives with parents, has no home loan, makes minimal investments, and prefers higher monthly cash flow, then the lower slab rates under the new regime can reduce overall tax liability.

Young professionals entering high-paying jobs often choose this regime because they want flexibility instead of locking money into tax-saving products. Freelancers and startup employees who frequently change jobs may also prefer simplified taxation.

Additionally, many employees fail to maximize available deductions every year. They invest randomly at the last minute without proper financial planning. In such situations, the old regime may actually increase tax burden because incomplete deductions cannot compensate for higher slab rates. Therefore, disciplined investing remains essential if you want the old regime to outperform the new regime.

Biggest Mistakes People Make While Choosing Tax Regime

Selecting the wrong tax regime is one of the most common financial mistakes salaried employees make every year. Unfortunately, many people decide based on social media opinions instead of actual calculations.

Blindly Following Friends Or Colleagues

Every individual has different salary structures, deductions, and financial goals. What works for one person may not work for another. Therefore, copying someone else’s tax regime choice is risky.

Ignoring Long-Term Wealth Creation

Many taxpayers select the new regime only for immediate tax savings but stop investing altogether. Over time, this affects retirement planning and wealth accumulation.

Not Calculating HRA Properly

HRA calculations are often misunderstood. Employees either underclaim or overclaim exemptions because they do not understand eligibility rules correctly.

Forgetting Additional Deductions

Several taxpayers forget deductions like NPS, health insurance premiums, and education loan interest while comparing tax regimes. Missing these deductions can lead to inaccurate calculations.

Choosing Convenience Over Savings

Some employees choose the new regime simply because it feels easier. However, a few hours of tax planning can sometimes save tens of thousands of rupees annually.

Smart Tax Saving Strategies For 15 LPA Salary Employees

Tax planning should never happen at the last moment. Smart salaried employees plan throughout the financial year to maximize deductions and improve wealth creation simultaneously.

One effective strategy is combining ELSS mutual funds with NPS contributions. ELSS offers market-linked returns with shorter lock-in periods compared to traditional tax-saving products. Meanwhile, NPS helps create retirement wealth while providing extra deductions.

Another powerful strategy involves optimizing salary structure. Employees can request tax-efficient salary components like meal coupons, fuel reimbursements, internet reimbursements, and telephone allowances where applicable.

Home loan planning can also dramatically improve tax efficiency. If purchasing property aligns with long-term goals, the interest deduction under the old regime becomes extremely valuable.

Additionally, maintaining proper investment documentation throughout the year avoids last-minute confusion. Many salaried employees lose deductions simply because they fail to submit proofs on time.

Finally, reviewing tax calculations every year is important because income levels, deductions, and government rules change regularly. A tax regime that works today may not remain optimal next year

Real Life Case Study Of A 15 LPA Employee Choosing The Right Tax Regime

Let us understand the practical impact of the New Vs Old Tax Regime Calculator For 15 LPA Salary through a real-world style example that mirrors what thousands of salaried employees face every financial year. Imagine Priya, a 32-year-old IT professional working in Bengaluru with an annual CTC of ₹15 lakh. Initially, she selected the new tax regime because several colleagues claimed it was “simpler and cheaper.” During the first year, she enjoyed slightly higher monthly in-hand salary because fewer deductions were involved. However, after reviewing her finances with a CA, she realized she had ignored several valuable tax-saving opportunities. Priya was paying rent in a metro city, contributing to EPF, investing in ELSS mutual funds, paying health insurance premiums for parents, and also repaying a home loan. Under the old regime, all these deductions significantly reduced her taxable income. After switching regimes and restructuring her investments properly, she reduced her annual tax liability by more than ₹70,000. More importantly, she also built a disciplined investment portfolio that supported her long-term wealth goals. This example highlights a crucial lesson. Tax planning is not just about reducing taxes today. It is also about creating future financial security. Many salaried professionals earning around 15 lakh miss this bigger picture because they focus only on immediate salary credits instead of long-term financial growth.

Step By Step Method To Calculate Tax On 15 LPA Salary

Many salaried employees feel overwhelmed when they hear terms like taxable income, exemptions, deductions, cess, and slab rates. However, calculating taxes becomes much easier when you follow a structured approach. The first step is identifying your total annual income including basic salary, HRA, special allowance, bonus, and any additional income sources. Once the gross salary is calculated, subtract the standard deduction available to salaried employees. After this, you need to calculate deductions under the old regime if applicable. These include Section 80C investments, NPS contributions, health insurance premiums, home loan interest, and HRA exemption. Once deductions are subtracted, the remaining amount becomes taxable income. Now apply the applicable slab rates according to the chosen regime. Finally, add health and education cess to determine the total tax payable. Under the new regime, calculations become simpler because most deductions are unavailable. However, simplicity does not automatically mean lower taxes. Therefore, the smartest approach is calculating taxes under both regimes side by side. This comparison instantly reveals which option saves more money. Today, many online tax calculators can automate this process, but understanding the logic behind calculations helps you make smarter financial decisions instead of blindly trusting automated tools.

How Salary Structure Impacts Tax Regime Selection

Most people think only total salary matters while comparing tax regimes, but the truth is your salary structure plays an equally important role. Two employees earning the same 15 lakh salary can end up paying completely different tax amounts depending on how their compensation is structured. For example, an employee receiving high HRA benefits while living in a rented metro city can save substantial tax under the old regime. Similarly, employees receiving employer NPS contributions or reimbursements for internet, travel, or telephone expenses may benefit more from traditional taxation. On the other hand, professionals receiving mostly fixed salary without exemptions often prefer the new regime. Many companies today also provide flexible benefit plans that allow employees to optimize taxes legally. Understanding these salary components becomes extremely important because even small adjustments can create major tax savings over time. Unfortunately, many salaried employees ignore their salary structure and focus only on slab rates. This leads to poor decisions. Therefore, before choosing a regime, carefully analyze all salary components including allowances, reimbursements, retirement benefits, and employer contributions. Sometimes a properly optimized salary structure can save more tax than changing the regime itself. This is why experienced financial planners always review salary breakup first before recommending a tax strategy.

Best Investments To Save Tax Under Old Tax Regime

The old tax regime becomes highly rewarding when taxpayers use deductions strategically instead of investing randomly in March every year. One of the best tax-saving options remains ELSS mutual funds because they combine wealth creation with tax deductions under Section 80C. Unlike traditional insurance plans, ELSS funds offer higher long-term growth potential with only a three-year lock-in period. Public Provident Fund is another excellent choice for conservative investors seeking guaranteed returns and tax-free maturity benefits. Meanwhile, National Pension System has become increasingly popular among salaried professionals because it offers an additional ₹50,000 deduction beyond the 80C limit. Health insurance also plays a major role in tax planning because premiums paid for self and parents qualify for deductions under Section 80D. Additionally, employees should never ignore EPF contributions because they automatically reduce taxable income while building retirement savings. Many financial experts recommend combining multiple investment options instead of depending entirely on one product. This approach improves diversification while maximizing deductions. However, the biggest mistake people make is choosing poor financial products solely for tax savings. Every investment should align with personal financial goals, risk tolerance, and liquidity needs. Smart tax planning always balances tax efficiency with wealth creation and future security.

Why The New Tax Regime Appeals To Young Professionals

The new tax regime has become increasingly popular among younger salaried employees, especially those in metro cities and fast-growing industries like technology and startups. One major reason is flexibility. Unlike the old regime, the new system does not force taxpayers to invest in specific products merely for deductions. Young professionals often prefer liquidity because they want freedom to invest in startups, equities, travel, higher education, or business opportunities instead of locking funds into long-term tax-saving instruments. Another reason is convenience. The new regime simplifies filing because employees do not need to maintain extensive documentation for deductions and exemptions. This becomes particularly attractive for people who frequently switch jobs or work in dynamic industries. Additionally, many younger professionals live with parents and do not pay significant rent or home loan EMIs. Therefore, traditional deductions offer limited value to them. However, there is also a hidden risk. Many people selecting the new regime stop investing consistently because tax incentives disappear. Over time, this affects wealth creation and retirement planning. Therefore, even if someone chooses the new regime, disciplined investing remains essential. Financial freedom comes from consistent wealth-building habits, not merely from lower tax slabs. Young professionals must understand this difference clearly before prioritizing short-term convenience over long-term financial security.

Hidden Benefits Of The Old Tax Regime Most People Ignore

When people compare tax regimes, they usually focus only on immediate tax calculations. However, the old regime provides several indirect financial advantages that many taxpayers completely overlook. One major hidden benefit is forced financial discipline. Because deductions encourage investments, salaried employees automatically build savings habits through PPF, ELSS, EPF, and NPS contributions. Over a decade, these investments can create substantial wealth. Another underrated advantage is insurance coverage. Tax-saving life insurance and health insurance plans often provide important financial protection for families while simultaneously reducing taxes. Additionally, home loan deductions encourage asset creation through real estate ownership. While buying property should never happen solely for tax benefits, deductions certainly improve affordability for long-term homeowners. The old regime also supports retirement planning because products like EPF and NPS build retirement corpus gradually over time. Furthermore, disciplined investors often achieve better overall financial management because they review expenses, savings, and investments regularly for tax planning purposes. Therefore, the old regime does much more than merely reducing taxes. It indirectly promotes wealth creation, insurance protection, retirement security, and long-term financial stability. Unfortunately, many salaried employees ignore these broader financial advantages while comparing only short-term tax outflows.

Common Myths About New Vs Old Tax Regime Calculator For 15 LPA Salary

There are countless misconceptions surrounding the New Vs Old Tax Regime Calculator For 15 LPA Salary, and these myths often lead to poor financial decisions. One common myth is that the new regime is always better because slab rates are lower. In reality, lower slab rates do not guarantee lower taxes if significant deductions are available under the old regime. Another widespread misconception is that the old regime is too complicated. While documentation requirements are higher, modern tax software and salary portals have made tax filing much easier than before. Some people also believe tax-saving investments provide poor returns. However, instruments like ELSS mutual funds historically delivered strong long-term growth alongside tax benefits. Another myth is that only high-income individuals benefit from tax planning. In truth, proper tax management matters even more for middle-income salaried employees because every saved rupee improves financial flexibility. Many taxpayers also think they cannot switch regimes later. Salaried employees actually have flexibility to choose the regime every year depending on changing financial circumstances. Therefore, tax planning should remain dynamic rather than fixed permanently. Breaking these myths is essential because misinformation often prevents people from making financially intelligent decisions that could save substantial money annually.

Advanced Tax Planning Tips For Salaried Employees

Most tax-saving advice available online focuses only on basic deductions. However, advanced tax planning strategies can further optimize taxes for salaried professionals earning 15 lakh annually. One powerful technique involves maximizing employer-provided benefits like meal coupons, fuel reimbursements, and telephone reimbursements where company policies permit. Another smart approach is increasing employer NPS contributions because these contributions provide additional tax benefits without affecting the regular 80C limit. Married couples can also strategically distribute investments and assets to improve overall family tax efficiency. For example, certain investments or rental incomes can be structured intelligently depending on income levels. Additionally, reviewing HRA declarations carefully can unlock higher exemptions, especially in metro cities with expensive rent. Some employees also benefit from professional tax planning around bonuses and variable pay structures. Timing investment redemptions and capital gains realization can further improve overall tax efficiency. Furthermore, maintaining a separate emergency fund prevents premature withdrawal from tax-saving investments during financial emergencies. Advanced tax planning is not about exploiting loopholes illegally. Instead, it focuses on understanding rules deeply and using every legitimate opportunity available under the law. Employees who proactively plan finances throughout the year usually save significantly more tax than those rushing during the final months before filing returns.

Best Online Tools To Compare New Vs Old Tax Regime

Technology has made tax comparison easier than ever before. Today, several reliable online platforms provide advanced calculators specifically designed for comparing the New Vs Old Tax Regime Calculator For 15 LPA Salary. These tools automatically calculate tax liability based on salary breakup, deductions, investments, HRA benefits, and home loan details. Many salaried employees prefer using calculators because they instantly generate side-by-side comparisons without manual calculations. Platforms like SEMrush, Ahrefs, Surfer SEO, and Rank Math are widely used for SEO optimization research, while financial calculators available on tax portals help improve personal finance planning accuracy. However, taxpayers should always cross-check calculator results because tax rules occasionally change. Additionally, automated tools may not fully account for unique salary structures or complex financial situations. Therefore, individuals with significant investments or multiple income sources should consider consulting qualified tax professionals for personalized advice. Online calculators work best as preliminary comparison tools rather than final decision-makers. Combining technology with human financial understanding creates the most accurate and beneficial tax planning outcomes.

New Vs Old Tax Regime Calculator For 15 LPA Salary Explained With Complete Tax Breakdown

The biggest reason why people search for New Vs Old Tax Regime Calculator For 15 LPA Salary is simple. Nobody wants to pay extra tax when legal tax-saving opportunities already exist. However, many salaried employees still make rushed decisions without understanding how income tax actually works. Some people choose the new regime because social media influencers call it “modern and simple.” Others stick to the old regime because they have always used it. Unfortunately, neither approach guarantees maximum tax savings. The correct decision depends on salary structure, deductions, financial discipline, investment habits, and future goals. This is exactly why using a proper New Vs Old Tax Regime Calculator For 15 LPA Salary becomes extremely important before filing your income tax return. A detailed comparison helps you identify which regime gives the lowest tax liability while supporting your financial future. Employees earning 15 lakh annually often fall into the category where even small tax-planning mistakes can lead to major financial losses over time. Therefore, understanding both tax systems deeply is no longer optional. It is an essential part of smart personal finance management in India.

How New Vs Old Tax Regime Calculator For 15 LPA Salary Helps You Save Money

A reliable New Vs Old Tax Regime Calculator For 15 LPA Salary does much more than simple tax calculation. It gives clarity. Most salaried employees struggle because they only look at tax slab percentages while ignoring deductions and exemptions that can dramatically reduce taxable income. The calculator compares both regimes side by side using your exact salary details. It includes deductions like Section 80C investments, HRA exemption, home loan interest, NPS contributions, and health insurance premiums. Once these deductions are entered, the calculator instantly reveals which tax regime produces lower tax liability. This process prevents emotional decision-making and replaces it with data-driven financial planning. Another major benefit of using a New Vs Old Tax Regime Calculator For 15 LPA Salary is long-term wealth awareness. When people see how deductions reduce taxes, they also realize how disciplined investments build future financial security. Many salaried employees ignore investing because they only focus on monthly salary credits. However, once tax calculations clearly show the financial benefits of smart investing, they become more serious about wealth creation. Therefore, this calculator acts as both a tax-planning tool and a financial awareness tool for salaried professionals.

Why New Vs Old Tax Regime Calculator For 15 LPA Salary Is Trending In 2026

Searches related to New Vs Old Tax Regime Calculator For 15 LPA Salary have increased rapidly because tax rules continue evolving and salaried employees want clarity before making financial decisions. Inflation, rising salaries, increasing rental costs, and changing investment habits have made tax planning more important than ever. Employees earning around 15 lakh salary often belong to urban middle-class families trying to balance expenses, EMIs, savings, and future goals simultaneously. Therefore, choosing the wrong regime directly impacts disposable income and investment capacity. Another reason for this trend is the growing popularity of digital finance platforms. Today, employees actively compare taxes online before selecting salary structures or making investments. YouTube finance creators, tax experts, and personal finance bloggers frequently discuss New Vs Old Tax Regime Calculator For 15 LPA Salary because millions of salaried individuals want simplified explanations. Additionally, younger professionals entering higher salary brackets for the first time often feel confused by tax terminology. They want practical examples instead of complicated legal language. This growing demand has turned tax-regime comparison content into one of the most searched finance topics in India. Therefore, understanding this subject properly provides both immediate tax benefits and long-term financial confidence.

New Vs Old Tax Regime Calculator For 15 LPA Salary For Salaried Employees Living In Metro Cities

Metro-city employees often receive the highest benefit from using a New Vs Old Tax Regime Calculator For 15 LPA Salary because their expenses and deductions are usually larger than those living in smaller cities. Rent itself becomes a major tax-saving factor through HRA exemptions. In cities like Bengaluru, Mumbai, Delhi, Hyderabad, and Pune, rental expenses consume a large portion of monthly salary. Under the old regime, HRA exemptions can significantly reduce taxable income. Additionally, metro-city professionals often invest heavily in SIPs, ELSS mutual funds, NPS accounts, and insurance products because financial awareness is generally higher in urban corporate environments. Many employees also pay home loan EMIs due to expensive property markets. These factors make the old regime extremely attractive for salaried professionals in metro cities. However, employees without investments or property ownership may still benefit from the new regime. This is why a New Vs Old Tax Regime Calculator For 15 LPA Salary becomes essential instead of relying on assumptions. Every financial detail matters. A salaried employee paying high rent and home loan interest may save far more under the old regime compared to someone with similar salary but fewer deductions. Therefore, metro-city professionals should never select a regime without detailed calculation.

Best Financial Habits To Improve Results From New Vs Old Tax Regime Calculator For 15 LPA Salary

Using a New Vs Old Tax Regime Calculator For 15 LPA Salary gives better results when combined with strong financial habits. Tax planning alone cannot create financial freedom unless supported by disciplined money management. The first important habit is investing consistently throughout the year instead of rushing during March. Last-minute tax-saving investments often lead to poor decisions and unsuitable financial products. Systematic monthly investing improves both wealth creation and tax efficiency. Another important habit is maintaining proper financial records. Salaried employees frequently lose deductions because they misplace rent receipts, insurance documents, or investment proofs. Organized documentation simplifies tax filing and prevents unnecessary stress. Emergency fund creation is another crucial habit because financial emergencies often force people to break long-term investments prematurely. Additionally, regular financial reviews help employees adjust strategies based on salary increases and changing goals. People earning 15 lakh annually usually experience career growth over time, which means tax planning should also evolve continuously. Most importantly, taxpayers should focus on overall wealth creation instead of chasing tax savings blindly. A good New Vs Old Tax Regime Calculator For 15 LPA Salary supports better financial decisions, but long-term financial discipline ultimately determines real success.

Which Employees Benefit Most From New Vs Old Tax Regime Calculator For 15 LPA Salary

The New Vs Old Tax Regime Calculator For 15 LPA Salary is especially useful for salaried employees who want maximum tax savings without making financial mistakes. Professionals working in IT companies, banks, MNCs, startups, government jobs, consulting firms, and private corporate sectors usually fall into this salary category. Most of these employees receive multiple salary components such as HRA, special allowance, performance bonus, employer PF contribution, gratuity benefits, and reimbursements. Because of this, the New Vs Old Tax Regime Calculator For 15 LPA Salary becomes extremely important for identifying the most tax-efficient option. Employees who pay rent, invest in SIPs, contribute to NPS, purchase health insurance, or pay home loan EMIs generally see a major difference in tax calculations between both regimes. On the other hand, salaried employees with very limited deductions may prefer the new regime because of lower slab rates and simpler compliance. However, the only accurate way to identify the better option is by using a detailed New Vs Old Tax Regime Calculator For 15 LPA Salary with proper deduction entries. Many taxpayers make the mistake of selecting the regime based on assumptions instead of calculations. This leads to unnecessary tax payments every year. Therefore, comparing both systems properly is one of the smartest financial habits for salaried professionals earning 15 lakh annually.

New Vs Old Tax Regime Calculator For 15 LPA Salary And Long Term Wealth Creation

One important factor people ignore while using a New Vs Old Tax Regime Calculator For 15 LPA Salary is long-term wealth creation. Most salaried employees focus only on current-year tax savings without understanding how tax planning affects future financial stability. The old regime indirectly encourages disciplined investing because deductions motivate people to invest regularly in PPF, EPF, ELSS mutual funds, NPS, and insurance plans. Over 10 to 20 years, these investments can build a significant retirement corpus and improve financial security. Meanwhile, many employees selecting the new regime enjoy slightly higher monthly in-hand salary but fail to invest systematically. As a result, they may save tax today but compromise long-term wealth creation. This is why financial experts often recommend using the New Vs Old Tax Regime Calculator For 15 LPA Salary not only for tax comparison but also for evaluating financial habits. If the old regime helps you maintain investment discipline and build assets consistently, then slightly lower in-hand salary may actually improve long-term wealth outcomes. Therefore, tax planning should never happen in isolation. It should always align with retirement goals, family security, emergency planning, and future financial independence. Employees who understand this relationship usually make smarter regime decisions compared to those focusing only on immediate tax calculations.

Why New Vs Old Tax Regime Calculator For 15 LPA Salary Is Important Before Salary Increment

Many salaried employees receive annual increments but fail to recalculate taxes properly afterward. This creates unexpected tax liabilities later in the financial year. A New Vs Old Tax Regime Calculator For 15 LPA Salary becomes extremely useful immediately after salary revision because increments often push employees into different tax situations. For example, an employee earning 12 lakh annually may initially benefit from the new regime due to fewer deductions. However, after promotion and salary increase to 15 lakh, the same employee may suddenly benefit more from the old regime because tax liability increases substantially at higher income levels. Additionally, increments often come with larger bonuses, revised HRA structures, stock options, and employer contributions. All these changes affect tax calculations significantly. Therefore, every salaried employee should use a New Vs Old Tax Regime Calculator For 15 LPA Salary after annual appraisal discussions instead of waiting until tax-filing season. Early tax planning helps employees restructure investments properly throughout the year. It also prevents last-minute panic investing in unsuitable tax-saving products. Financially smart professionals treat salary increments as opportunities to improve overall tax efficiency and wealth creation simultaneously. This proactive mindset separates financially stable individuals from those constantly struggling with tax confusion and cash-flow problems.

New Vs Old Tax Regime Calculator For 15 LPA Salary For Employees With Home Loan

Employees paying home loan EMIs often receive the highest benefit from using a New Vs Old Tax Regime Calculator For 15 LPA Salary because home loan deductions can dramatically reduce taxable income under the old regime. Interest paid on self-occupied home loans qualifies for deductions up to ₹2 lakh annually. Additionally, principal repayment contributes toward Section 80C deductions. Combined together, these benefits significantly lower taxable income for salaried professionals earning around 15 lakh annually. Many taxpayers ignore this advantage while comparing slab rates superficially. Under the new regime, these valuable deductions disappear, which can increase total tax liability despite lower slab percentages. Therefore, employees with ongoing home loans should always use a detailed New Vs Old Tax Regime Calculator For 15 LPA Salary before selecting the new regime. Another important point is that property ownership also supports long-term asset creation. While home purchase decisions should never happen solely for tax savings, the deductions certainly improve affordability and financial efficiency. Employees living in expensive metro cities particularly benefit because property EMIs are usually substantial. Therefore, combining home loan benefits with HRA planning, NPS contributions, and Section 80C investments can make the old regime far more rewarding for salaried homeowners compared to the new regime.

Mistakes To Avoid While Using New Vs Old Tax Regime Calculator For 15 LPA Salary

Although a New Vs Old Tax Regime Calculator For 15 LPA Salary simplifies tax comparison, many salaried employees still make serious mistakes while using these tools. One common mistake is entering incomplete salary details. Many employees ignore bonuses, special allowances, or variable pay components, which leads to inaccurate tax calculations. Another major mistake is forgetting employer PF contributions and NPS benefits. These factors significantly impact final taxable income under the old regime. Some people also underestimate HRA exemptions by entering incorrect rental information. As a result, the calculator produces misleading comparisons. Another frequent error is ignoring future investments. Employees sometimes compare regimes based only on current deductions instead of planned investments for the financial year. This creates inaccurate long-term decisions. Additionally, many taxpayers blindly trust online calculators without understanding the logic behind results. While digital tools are helpful, users should still understand basic tax concepts to avoid confusion. A New Vs Old Tax Regime Calculator For 15 LPA Salary works best when salary details, deductions, and investment plans are entered carefully and honestly. Finally, one of the biggest mistakes is selecting a regime based purely on convenience instead of financial benefit. Even if the old regime requires slightly more paperwork, substantial tax savings may justify the extra effort completely.

Future Of New Vs Old Tax Regime Calculator For 15 LPA Salary In India

The importance of the New Vs Old Tax Regime Calculator For 15 LPA Salary will continue increasing in the coming years because India’s salaried workforce is growing rapidly and financial awareness is improving. More professionals now actively compare taxes, investments, insurance, and retirement planning instead of depending entirely on employers or tax consultants. Additionally, digital finance platforms, AI-based tax tools, and online calculators are making tax planning easier for ordinary salaried employees. The government may also continue modifying tax slabs and deduction structures over time, which means regular tax comparison will become even more important. Employees earning around 15 lakh annually represent a large portion of India’s urban middle class, and this group constantly seeks ways to improve disposable income while building future wealth. Therefore, the New Vs Old Tax Regime Calculator For 15 LPA Salary will remain one of the most searched finance topics in India for years ahead. Another important trend is personalized tax planning. Future tax tools may provide customized recommendations based on salary structure, city, investment goals, family responsibilities, and risk appetite. However, regardless of technological improvements, one principle will always remain true. Smart taxpayers compare both regimes carefully before making decisions. Those who actively manage taxes usually build stronger financial foundations compared to people who ignore planning completely.

FAQ – New Vs Old Tax Regime Calculator For 15 LPA Salary

Which regime is better according to New Vs Old Tax Regime Calculator For 15 LPA Salary?

The better regime depends on deductions and investments. Employees claiming HRA, home loan interest, Section 80C deductions, and NPS benefits often save more under the old regime. Those with minimal deductions may benefit from the new regime.

Can I switch every year using New Vs Old Tax Regime Calculator For 15 LPA Salary?

Yes, salaried employees can usually choose between the new and old regime every financial year while filing income tax returns. This flexibility helps taxpayers adjust according to changing financial situations.

Does home loan affect New Vs Old Tax Regime Calculator For 15 LPA Salary results?

Yes, home loan interest deductions significantly impact tax calculations under the old regime. Employees with large home loan EMIs often find the old regime more beneficial.

Is New Vs Old Tax Regime Calculator For 15 LPA Salary accurate?

Most reputed calculators provide accurate estimates if all salary details and deductions are entered correctly. However, taxpayers should still review results carefully or consult professionals for complex financial situations.

Why is New Vs Old Tax Regime Calculator For 15 LPA Salary important?

This calculator helps salaried employees compare both tax systems properly, reduce unnecessary taxes legally, improve investment planning, and make smarter long-term financial decisions

New Vs Old Tax Regime Calculator For 15 LPA Salary For IT Employees In India

The New Vs Old Tax Regime Calculator For 15 LPA Salary has become extremely important for IT employees because most professionals in the technology sector receive complex salary structures with multiple allowances and bonuses. Software engineers, developers, data analysts, cybersecurity experts, and project managers often earn around 15 lakh annually in metro cities like Bengaluru, Hyderabad, Pune, Chennai, and Gurugram. These professionals usually receive HRA benefits, EPF contributions, joining bonuses, performance incentives, and stock-related compensation. Because of this, the New Vs Old Tax Regime Calculator For 15 LPA Salary helps IT employees compare taxes more accurately instead of depending on assumptions. Employees paying high rent in metro cities often save substantial tax under the old regime through HRA exemptions. Similarly, IT professionals investing aggressively in ELSS mutual funds, NPS accounts, and health insurance may also benefit more from traditional taxation. However, younger tech employees without major deductions sometimes prefer the new regime because it increases monthly in-hand salary and simplifies compliance. Therefore, every IT employee should use a proper New Vs Old Tax Regime Calculator For 15 LPA Salary before submitting investment declarations to employers. Even small changes in deductions can create massive differences in annual tax liability. Smart IT professionals understand that tax planning is not only about reducing taxes but also about maximizing long-term financial growth and maintaining better cash flow management.

How New Vs Old Tax Regime Calculator For 15 LPA Salary Impacts Monthly In-Hand Salary

One major reason why employees search for New Vs Old Tax Regime Calculator For 15 LPA Salary is to understand the impact on monthly take-home salary. Many salaried professionals focus heavily on in-hand income because it directly affects lifestyle, EMI management, travel expenses, family budgeting, and investment capacity. Under the new regime, lower slab rates usually increase monthly in-hand salary because deductions and investment commitments are lower. Employees often feel financially comfortable because they receive more cash immediately. However, under the old regime, a portion of salary may go toward tax-saving investments like EPF, PPF, ELSS funds, NPS, and insurance premiums. Although monthly take-home salary appears slightly lower, long-term wealth creation becomes stronger. This is why the New Vs Old Tax Regime Calculator For 15 LPA Salary should never be used only for short-term comparison. Employees must also analyze how investment-linked deductions improve future financial security. Another important factor is employer tax deduction at source. Companies calculate TDS based on the selected regime, which directly impacts monthly salary credits. Therefore, selecting the wrong regime may lead to unnecessary tax deductions throughout the year. Using a detailed New Vs Old Tax Regime Calculator For 15 LPA Salary helps employees balance present cash flow with future financial goals more effectively.

Why Financial Experts Recommend New Vs Old Tax Regime Calculator For 15 LPA Salary Every Year

Financial experts consistently recommend using a New Vs Old Tax Regime Calculator For 15 LPA Salary every financial year because tax situations change regularly. Salary increments, bonuses, changing rent amounts, marriage, home loans, insurance purchases, and investment decisions all affect tax liability significantly. A regime that saved more tax last year may not remain beneficial this year. For example, an employee without investments may initially prefer the new regime. However, after purchasing a home, starting NPS contributions, or increasing ELSS investments, the old regime may suddenly become more advantageous. This is why financial advisors never recommend permanent assumptions regarding taxation. Instead, they encourage annual comparison through a reliable New Vs Old Tax Regime Calculator For 15 LPA Salary. Another important reason is government policy changes. Tax slabs, deduction limits, rebate rules, and standard deduction benefits may evolve over time. Employees who ignore yearly comparison often continue paying higher taxes unnecessarily. Additionally, annual tax review improves overall financial awareness. It encourages salaried professionals to analyze investments, spending patterns, retirement planning, and wealth creation strategies systematically. Therefore, using a New Vs Old Tax Regime Calculator For 15 LPA Salary annually is not just a tax-saving exercise. It is a critical financial planning habit that supports long-term stability and smarter money management.

New Vs Old Tax Regime Calculator For 15 LPA Salary And Retirement Planning

Retirement planning is another important area connected closely with the New Vs Old Tax Regime Calculator For 15 LPA Salary. Many salaried employees focus heavily on present expenses while ignoring future financial security. However, tax-saving investments under the old regime often double as retirement-building tools. EPF contributions, PPF accounts, NPS investments, and ELSS mutual funds help create long-term wealth gradually. Employees choosing the old regime frequently build larger retirement corpus because deductions motivate disciplined investing. On the other hand, employees selecting the new regime sometimes enjoy higher in-hand salary but fail to invest consistently for retirement. Over time, this can create financial insecurity during later stages of life. Therefore, the New Vs Old Tax Regime Calculator For 15 LPA Salary should always be viewed through a retirement-planning perspective as well. If tax-saving investments help you remain financially disciplined and create future wealth, then the old regime may provide benefits beyond immediate tax reduction. Financial independence requires systematic investing for decades, not just temporary tax savings. This is why experienced financial planners often combine tax planning with retirement planning instead of treating them separately. Employees earning 15 lakh annually have strong earning potential, which means disciplined investment strategies implemented early can create significant wealth before retirement age.

New Vs Old Tax Regime Calculator For 15 LPA Salary For Beginners

Beginners entering higher salary brackets often feel overwhelmed by taxation concepts, making the New Vs Old Tax Regime Calculator For 15 LPA Salary extremely useful for simplifying decisions. Fresh professionals receiving their first high-paying corporate salary frequently struggle with deductions, exemptions, TDS calculations, and investment declarations. Many simply follow HR suggestions without understanding actual financial impact. However, early tax awareness creates stronger financial habits for life. A New Vs Old Tax Regime Calculator For 15 LPA Salary helps beginners understand how salary structure affects taxation and why investments matter beyond tax savings. It teaches concepts like HRA exemption, Section 80C deductions, NPS contributions, and home loan benefits in practical terms. Beginners also learn the difference between taxable income and gross salary, which removes common confusion. Another important advantage is financial confidence. Employees who understand taxation early usually make better career and investment decisions later. They avoid panic during tax-filing season and maintain better control over monthly finances. Therefore, every young professional entering the 15 lakh salary range should spend time understanding how a New Vs Old Tax Regime Calculator For 15 LPA Salary works instead of ignoring tax planning completely. Financial literacy developed early creates massive long-term advantages in wealth creation and money management.

New Vs Old Tax Regime Calculator For 15 LPA Salary And Smart Wealth Building

The New Vs Old Tax Regime Calculator For 15 LPA Salary is not only about saving taxes legally. It also supports smarter wealth-building strategies when used correctly. Most financially successful individuals understand that tax efficiency and wealth creation work together. Money saved through intelligent tax planning can be redirected toward investments, emergency funds, retirement planning, and asset creation. Employees using the old regime often build wealth through disciplined contributions toward ELSS mutual funds, PPF accounts, NPS investments, and home ownership. Meanwhile, employees choosing the new regime can still build wealth if they consciously invest extra in-hand salary instead of increasing lifestyle expenses unnecessarily. This is why the New Vs Old Tax Regime Calculator For 15 LPA Salary should always connect with broader financial goals. Tax planning becomes powerful only when it supports long-term financial growth. Another important aspect is behavioral finance. Tax-saving investments create structured investing habits because employees contribute regularly throughout the year. Over decades, consistency becomes more important than occasional large investments. Therefore, employees should never evaluate the New Vs Old Tax Regime Calculator For 15 LPA Salary purely from a short-term perspective. The smartest taxpayers focus on total financial growth, future security, retirement readiness, and asset accumulation alongside annual tax reduction.

New Vs Old Tax Regime Calculator For 15 LPA Salary For Maximum Tax Savings In 2026

The New Vs Old Tax Regime Calculator For 15 LPA Salary is one of the most powerful tools for salaried employees who want maximum tax savings in 2026 without making financial mistakes. Employees earning around 15 lakh annually often fall into a critical income bracket where tax planning decisions create a major difference in overall wealth creation. Many people assume the new regime automatically reduces taxes because slab rates appear lower. However, the New Vs Old Tax Regime Calculator For 15 LPA Salary clearly shows that deductions, exemptions, and investment habits often make the old regime more rewarding for many salaried professionals. Employees paying rent, investing under Section 80C, contributing to NPS, purchasing health insurance, and repaying home loans usually discover substantial tax savings under the old regime after proper comparison. Meanwhile, employees without major deductions may benefit more from the new regime. Therefore, the New Vs Old Tax Regime Calculator For 15 LPA Salary should always be used before submitting investment declarations or filing income tax returns. Smart taxpayers compare both systems carefully every year instead of blindly following social media advice or office discussions. This comparison helps reduce unnecessary tax payments while improving long-term financial planning and wealth-building discipline simultaneously.

Benefits Of Using New Vs Old Tax Regime Calculator For 15 LPA Salary Before Filing ITR

Using a New Vs Old Tax Regime Calculator For 15 LPA Salary before filing income tax returns helps salaried employees avoid costly errors and maximize legal tax savings efficiently. Many taxpayers wait until the final weeks before ITR filing and then make rushed financial decisions without proper calculation. This often leads to incorrect regime selection and higher tax liability. A detailed New Vs Old Tax Regime Calculator For 15 LPA Salary removes confusion by comparing both regimes side by side using exact salary details, deductions, investments, HRA benefits, insurance premiums, and loan repayments. Another major benefit is better financial clarity. Employees understand how different investments affect taxable income and future wealth creation. The New Vs Old Tax Regime Calculator For 15 LPA Salary also helps improve budgeting because employees can estimate tax deductions throughout the year instead of facing sudden surprises later. Many salaried professionals underestimate how much tax they can legally save through proper planning. Once they use a detailed comparison calculator, they often realize that strategic investments dramatically reduce overall tax burden. Therefore, tax comparison should never happen casually. A proper New Vs Old Tax Regime Calculator For 15 LPA Salary transforms taxation from a stressful obligation into a structured financial-planning process that supports long-term financial stability and better money management.

Why New Vs Old Tax Regime Calculator For 15 LPA Salary Is Important For Family Financial Planning

The New Vs Old Tax Regime Calculator For 15 LPA Salary becomes even more important when family responsibilities increase. Salaried employees supporting spouses, children, parents, or home loans must carefully optimize taxes because every saved rupee improves household financial stability. Employees with families usually invest more aggressively in insurance, retirement plans, education funds, and medical coverage. These investments create valuable deductions under the old regime, making the New Vs Old Tax Regime Calculator For 15 LPA Salary essential for accurate tax comparison. Health insurance premiums for parents, tuition fee deductions for children, and home loan benefits significantly impact taxable income. Therefore, employees with family responsibilities often discover that the old regime provides stronger overall financial advantages despite slightly higher slab rates. Another important factor is long-term security. Family-oriented financial planning requires disciplined savings and asset creation. Tax-saving investments encouraged by the old regime support this goal naturally. However, even employees choosing the new regime should maintain disciplined investing habits independently. The New Vs Old Tax Regime Calculator For 15 LPA Salary helps families identify the balance between current cash flow and future financial security. Smart family financial planning always integrates taxation, insurance, investments, emergency funds, and retirement preparation together instead of treating them separately.

Conclusion

Choosing between both tax systems without using a proper New Vs Old Tax Regime Calculator For 15 LPA Salary can lead to major financial mistakes. Salaried employees earning 15 lakh annually often fall into a category where deductions, investments, HRA exemptions, home loans, and retirement contributions significantly impact tax liability. Therefore, blindly choosing a regime based on social media advice or office discussions is risky. A detailed New Vs Old Tax Regime Calculator For 15 LPA Salary helps identify the most beneficial option based on actual numbers instead of assumptions. More importantly, tax planning should always support long-term wealth creation, financial discipline, and retirement security. Employees who actively compare taxes every year usually save more money and build stronger financial habits over time. Whether you choose the new regime or old regime, the smartest approach is understanding your salary structure, investment goals, and future financial responsibilities clearly. Start planning early, review deductions carefully, and use a reliable New Vs Old Tax Regime Calculator For 15 LPA Salary before filing your taxes in 2026.